1.

Prepare the journal entries for the formation of the

1.

Explanation of Solution

Partnership:

A partnership is an unincorporated form of business which is formed by an agreement, owned and managed mutually by two or more individuals, who invest their assets in the business and share the liabilities and profits among themselves.

Journal entry is a set of economic events which can be measured in monetary terms. These are recorded chronologically and systematically.

Accounting rules for Journal entries:

- To record increase balance of account: Debit assets, expenses, losses and credit liabilities, capital, revenue and gains.

- To record decrease balance of account: Credit assets, expenses, losses and debit liabilities, capital, revenue and gains.

Record the journal entry:

| Date | Account titles and Explanation | Debit | Credit |

| January 1 | Cash | $13,544 | |

| Accounts Receivable | $15,280 | ||

| Merchandise Inventory | $89,692 | ||

| Supplies | $1,286 | ||

| Office Equipment | $18,000 | ||

| Store Equipment | $8,000 | ||

| Allowance for | $1,720 | ||

| Notes payable | $36,000 | ||

| Accounts payable | $18,082 | ||

| Partner F, Capital | $90,000 | ||

| (To record investment of Partner F in partnership) |

Table (1)

- Cash is an asset and it is increased. Therefore, debit cash by $13,544.

- Accounts receivable is an asset and it is increased. Therefore, debit accounts receivable account by $15,280.

- Merchandise inventory is an asset and it is increased. Therefore, debit merchandise inventory account by $89,692.

- Supplies are asset and it is increased. Therefore, debit supplies account by $1,286.

- Office equipment is an asset and it is increased. Therefore, debit office equipment account by $18,000.

- Store equipment is an asset and it is increased. Therefore, debit store equipment account by $8,000.

- Allowance for bad debts is a component of partners’ equity and it is increased which decreases the value of partners’ equity. Therefore, credit allowance for bad debts account by $1,720.

- Notes payable is a liability and it is increased. Therefore, credit notes payable account by $36,000.

- Accounts payable is a liability and it is increased. Therefore, credit accounts payable account by $18,082.

- Partner F, Capital is a component of partners’ equity and it is increases the value of partners’ equity. Therefore, credit Partner F, capital account by $90,000.

Record the investment made by Partner B:

| Date | Account titles and Explanation | Debit | Credit |

| January 1 | Cash | $50,000 | |

| Partner B, Capital | $50,000 | ||

| ( To record investment of Partner B in partnership) |

Table (2)

- Cash is an asset and it is increased. Therefore, debit cash account by $50,000

- Partner B, Capital is a component of

stockholders’ equity and it is increases the value of partners’ equity. Therefore, credit Partner B, capital account by $50,000.

2.

Prepare the lower portion of the income statement reporting the allocation of the profits to each partner.

2.

Explanation of Solution

Income statement: The financial statement which reports revenues and expenses from business operations and the result of those operations as net income or net loss for a particular time period is referred to as income statement. In partnership, the division is often recorded in the lower portion of the income statement.

Prepare the lower portion of the income statement reporting the allocation of the profits to each partner.

| Partnership F and B Plumbing supplies | |||

| Income Statement (Partial) | |||

| For Year Ended December 31 | |||

| Net income | $150,000 | ||

| Allocation of net income: | Partner F | partner B | Total |

| Salary allowances | $50,000 | $30,000 | $80,000 |

| Interest allowances | $9,000 | $5,000 | $14,000 |

| Remaining income | $33,600 | $22,400 | $56,000 |

| Allocation of net income | $92,600 | $57,400 | $150,000 |

Table (3)

3.

Prepare journal entry for the investment of Partner P.

3.

Explanation of Solution

| Date | Account titles and Explanation | Debit | Credit |

| January 1 | Cash | $30,000 | |

| Partner F, Capital | $30,000 | ||

| ( To record investment of Partner F in partnership) |

Table (4)

- Cash is an asset and it is increased. Therefore, debit cash account by $30,000

- Partner B, Capital is a component of stockholders’ equity and it is increases the partners’ equity. Therefore, credit Partner B, capital account by $30,000.

4.

Prepare a statement of partnership liquidation and related journal entries.

4.

Explanation of Solution

Liquidation of partnership:

Liquidation is the process where assets are sold, gains and losses are allocated to the partners, liabilities are paid out and the cash that is remaining cash or other assets are distributed to partners.

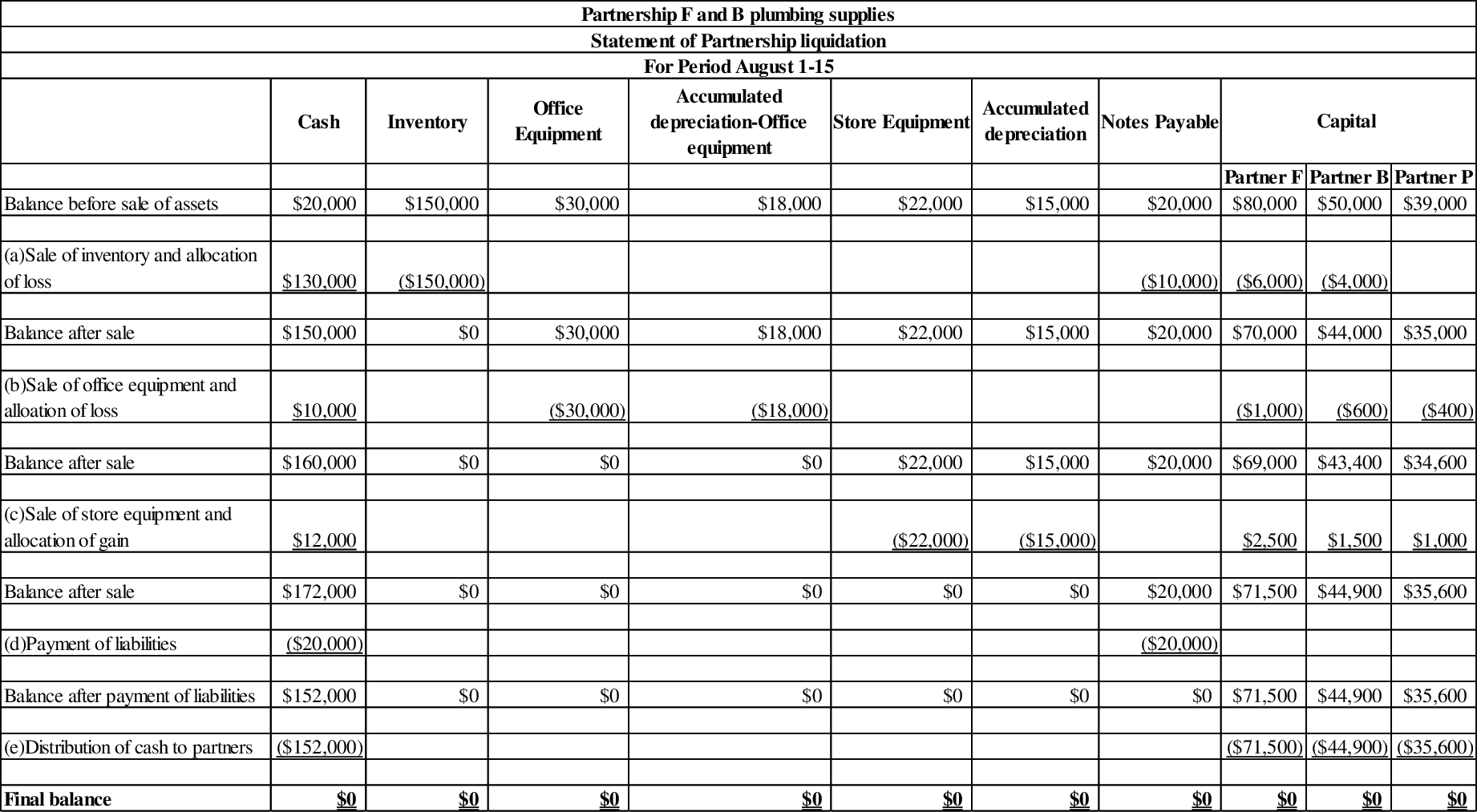

The statement of partnership liquidation statement is prepared as follows:

Figure (1)

Record the journal entry:

| Date | Account titles and Explanation | Debit | Credit |

| August 1 | Cash | $130,000 | |

| Loss on sale of assets | $20,000 | ||

| Inventory | $150,000 | ||

| (To record sale of assets) |

Table (5)

- Cash is an asset and it is increased. Therefore, debit cash account by $130,000.

- Loss on sale of assets is a component of partners’ equity and it is decreased which increases the value of partners’ equity. Therefore, debit loss on sale of assets account, by $20,000.

- Inventory is an asset and it is decreased. Therefore, credit inventory account by $150,000.

| Date | Account titles and Explanation | Debit | Credit |

| August 1 | Partner F, Capital | $10,000 | |

| Partner B, Capital | $6,000 | ||

| Partner P, Capital | $4,000 | ||

| Loss on sale of assets | $20,000 | ||

| ( To record allocation of loss) |

Table (6)

- Partner F, Capital is a component of partners’ equity and it is decreased which increases the value of partners’ equity. Therefore, debit Partner F, capital account by $10,000.

- Partner B, Capital is a component of partners’ equity and it is decreased which increases the value of partners’ equity. Therefore, debit Partner B, capital account by $6,000.

- Partner P, Capital is a component of partners’ equity and it is decreased which increases the value of partners’ equity. Therefore, debit Partner P, capital account by $4,000.

- Loss on sale of assets is a component of partners’ equity and it is increased which decreases the value of partners’ equity. Therefore, credit loss on sale of assets account, by $20,000.

| Date | Account titles and Explanation | Debit | Credit |

| August 3 | Cash | $10,000 | |

| $18,000 | |||

| Loss on sale of inventory | $2,000 | ||

| Office equipment | $30,000 | ||

| ( To record Sale of office equipment) |

Table (7)

- Cash is an asset and it is increased. Therefore, debit cash account by $10,000.

- Accumulated depreciation is a contra asset and it is decreased. Therefore, debit accumulated depreciation account by $18,000.

- Loss on sale of assets is a component of partners’ equity and it is decreased which increases the value of partners’ equity. Therefore, debit loss on sale of assets account, by $2,000.

- Office equipment is an asset and it is decreased. Therefore, credit office equipment account by $30,000.

| Date | Account titles and Explanation | Debit | Credit |

| August 3 | Partner F, Capital | $10,000 | |

| Partner B, Capital | $6,000 | ||

| Partner P, Capital | $4,000 | ||

| Loss on sale of office furniture | $20,000 | ||

| ( To record distribution of cash to partners) |

Table (8)

- Partner F, Capital is a component of partners’ equity and it is decreased which increases the value of partners’ equity. Therefore, debit Partner F, capital account by $10,000.

- Partner B, Capital is a component of partners’ equity and it is decreased which increases the value of partners’ equity. Therefore, debit Partner B, capital account by $6,000.

- Partner P, Capital is a component of partners’ equity and it is decreased which increases the value of partners’ equity. Therefore, debit Partner P, capital account by $4,000.

- Loss on sale of assets is a component of partners’ equity and it is increased which decreases the value of partners’ equity. Therefore, credit loss on sale of assets account, by $20,000.

| Date | Account titles and Explanation | Debit | Credit |

| August 5 | Cash | $120,000 | |

| Accumulated Depreciation-Store equipment | $150,000 | ||

| Store equipment | $22,000 | ||

| Gain on sale of store equipment | $5,000 | ||

| (To record sale of store equipment) |

Table (9)

- Cash is an asset and it is increased. Therefore, debit cash account by $120,000.

- Accumulated depreciation is a contra asset and it is decreased. Therefore, debit accumulated depreciation account by $150,000.

- Office equipment is an asset and it is decreased. Therefore, credit office equipment account by $22,000.

- Gain on sale of asset is a component of partners’ equity and it is increased which decreases the value of partners’ equity. Therefore, credit gain on sale of assets account, by $5,000.

| Date | Account titles and Explanation | Debit | Credit |

| August 5 | Gain on sale of assets | $5,000 | |

| Partner F, Capital | $2,500 | ||

| Partner B, Capital | $1,500 | ||

| Partner P, Capital | $1,000 | ||

| ( To record allocation of gain) |

Table (10)

- Gain on sale of assets is a component of partners’ equity and it is decreased which increases the value of partners’ equity. Therefore, debit gain on sale of assets account, by $5,000.

- Partner F, Capital is a component of partners’ equity and it is increased which decreases the value of partners’ equity. Therefore, credit Partner F, capital account by $2,500.

- Partner B, Capital is a component of partners’ equity and it is increased which decreases the value of partners’ equity. Therefore, credit Partner B, capital account by $1,500.

- Partner P, Capital is a component of partners’ equity and it is increased which decreases the value of partners’ equity. Therefore, credit Partner P, capital account by $1,000.

| Date | Account titles and Explanation | Debit | Credit |

| August 10 | Notes payable | $20,000 | |

| Cash | $20,000 | ||

| ( To record payment of notes payable) |

Table (11)

- Notes payable is a liability and it is decreased. Therefore, debit notes payable account by $20,000.

- Cash is an asset and it decreased. Therefore, debit cash account by $20,000.

| Date | Account titles and Explanation | Debit | Credit |

| August 15 | Partner F, Capital | $71,500 | |

| Partner B, Capital | $ 44,900 | ||

| Partner P Capital | $35,600 | ||

| Cash | $152,000 | ||

| ( To record distribution of cash) |

Table (12)

- Partner F, Capital is a component of partners’ equity and it is decreased which increases the value of partners’ equity. Therefore, debit Partner F, capital account by $71,500.

- Partner B, Capital is a component of partners’ equity and it is decreased which increases the value of partners’ equity. Therefore, debit Partner B, capital account by $44,900.

- Partner P, Capital is a component of partners’ equity and it is decreased which increases the value of partners’ equity. Therefore, debit Partner P, capital account by $35,600.

- Cash is an asset and it is decreased. Therefore, credit cash account by $152,000.

Want to see more full solutions like this?

Chapter 19 Solutions

College Accounting, Chapters 1-27 (New in Accounting from Heintz and Parry)

- Edward Seymour is a financial consultant to Cornish Inc., a real estate syndicate. Cornish Inc. finances and develops commercial real estate (office buildings). The completed projects are then sold as limited partnership interest to individual investors. The syndicate makes a profit on the sale of these partnership interests. Edward provides financial information for the offering projects, which is a document that provides the financial and legal details of the limited partnership offerings. In one of the projects, the bank has financed the construction of a commercial office building at a rate of 10% for the first four years, after which time the rate jumps to 15% of the mortgage. The interest costs are one of the major ongoing costs of a real estate project. Edward has reported prominently in the prospectus that the break-even occupancy for the first four years is 65%. This is the amount of office space that must be leased to cover and general upkeep costs over the first four…arrow_forwardMeyers is considering investing in one of several existing partnerships and is attempting to consider the price to be paid for a partnership interest. In addition to investing cash, Meyers would be contributing a piece of land that has a fair market value of $50,000. The existing partnerships are characterized as follows:(attached)1. Determine the amount of consideration that Meyers should have to convey in order to acquire an interest in each of the partnerships.2. Assume that in addition to the land Meyers was asked to convey cash of $4,000, $60,000, and $15,000 to partnerships A through C, respectively. Determine the amount of goodwill to be recorded assuming that all assets are adjusted to fair value. Indicate to whom the goodwill is traceable.arrow_forwardSteve Reese is a well-known interior designer in Fort Worth, Texas. He wants to start his own business and convinces Rob O’Donnell, a local merchant, to contribute the capital to form a partnership. On January 1, 2022, O’Donnell invests a building worth $54,000 and equipment valued at $20,000 as well as $16,000 in cash. Although Reese makes no tangible contribution to the partnership, he will operate the business and be an equal partner in the beginning capital balances. To entice O’Donnell to join this partnership, Reese draws up the following profit and loss agreement: O’Donnell will be credited annually with interest equal to 10 percent of the beginning capital balance for the year. O’Donnell will also have added to his capital account 10 percent of partnership income each year (without regard for the preceding interest figure) or $5,000, whichever is larger. All remaining income is credited to Reese. Neither partner is allowed to withdraw funds from the partnership during 2022.…arrow_forward

- Barbara Ripley and Fred Nichols decide to organize the ALL-Star partnership. Ripley invests $15,000 cash, and Nichols contributes $10,000 cash and equipment having a book value of $3,500.Prepare the entry to record Nichols’s investment in the partnership, assuming the equipment has a fair value of $4,000. What is the account title and explanation? what is debit? what is credit?arrow_forwardSteve Reese is a well-known interior designer in Fort Worth, Texas. He wants to start his own business and convinces Rob O’Donnell, a local merchant, to contribute the capital to form a partnership. On January 1, 2019, O’Donnell invests a building worth $74,000 and equipment valued at $44,000 as well as $32,000 in cash. Although Reese makes no tangible contribution to the partnership, he will operate the business and be an equal partner in the beginning capital balances. To entice O’Donnell to join this partnership, Reese draws up the following profit and loss agreement: O’Donnell will be credited annually with interest equal to 10 percent of the beginning capital balance for the year.O’Donnell will also have added to his capital account 10 percent of partnership income each year (without regard for the preceding interest figure) or $6,000, whichever is larger. All remaining income is credited to Reese.Neither partner is allowed to withdraw funds from the partnership during 2019.…arrow_forwardSteve Reese is a well-known Interior designer in Fort Worth, Texas. He wants to start his own business and convinces Rob O'Donnell, a local merchant, to contribute the capital to form a partnership On January 1, 2022, O'Donnell Invests a building worth $102,000 and equipment valued at $40,000 as well as $38,000 in cash. Although Reese makes no tangible contribution to the partnership, he will operate the business and be an equal partner In the beginning capital balances. To entice O'Donnell to join this partnership. Reese draws up the following profit and loss agreement: ⚫ O'Donnell will be credited annually with interest equal to 20 percent of the beginning capital balance for the year. ⚫ O'Donnell will also have added to his capital account 10 percent of partnership Income each year (without regard for the preceding Interest figure) cr $4,000, whichever is larger. All remaining Income is credited to Reese. Neither partner is allowed to withdraw funds from the partnership during 2022.…arrow_forward

- Steve Reese is a well-known interior designer in Fort Worth, Texas. He wants to start his own business and convinces Rob O’Donnell, a local merchant, to contribute the capital to form a partnership. On January 1, 2019, O’Donnell invests a building worth $126,000 and equipment valued at $132,000 as well as $52,000 in cash. Although Reese makes no tangible contribution to the partnership, he will operate the business and be an equal partner in the beginning capital balances. To entice O’Donnell to join this partnership, Reese draws up the following profit and loss agreement: O’Donnell will be credited annually with interest equal to 10 percent of the beginning capital balance for the year. O’Donnell will also have added to his capital account 20 percent of partnership income each year (without regard for the preceding interest figure) or $7,000, whichever is larger. All remaining income is credited to Reese. Neither partner is allowed to withdraw funds from the partnership during…arrow_forwardJerry and Chan have formed a partnership. Jerry contributed cash of 630,000 and computer equipment that cost 225,000. The fair value of the computer is 180,000. Jerry has notes payable on the computer worth 60,000 to be assumed by the partnership. Jerry is to have 60% capital interest in the partnership. Gray contributed only 450,000. The partners agreed to share profits and losses equally. Jerry should make an additional investment or withdrawal at what amount?arrow_forwardThomas Richey operates a small shop that sells fishing equipment. His postclosing trial balance on December 31, 20X1, is shown below. Richey plans to enter into a partnership with Kathryn Price, effective January 1, 20X2. Profits and losses will be shared equally. Richey is to transfer all assets and liabilities of his store to the partnership after revaluation as agreed. Price will invest cash equal to Richey’s investment after revaluation. The agreed values are Accounts Receivable (net), $58,000; Merchandise Inventory, $199,600; and Furniture and Equipment, $49,200. The partnership will operate as Richey and Price Angler’s Outpost. Richey's Tackle Center Postclosing Trial Balance December 31, 20X1 Account Name Debit Credit Cash $19,000 Accounts Receivable 65,600 Allowance for Doubtful Accounts $10,000 Merchandise Inventory 180,000 Furniture and Equipment 116,400 Accumulated Depreciation 92,000 Accounts Payable…arrow_forward

- Bobby Robinson and Nicholas White decide to organize the R&W partnership. Robinson invests $15,000 cash, and White contributes $10,000 cash and equipment having a book value of $4,500. Prepare the entry to record White’s investment in the partnership, assuming the equipment has a fair value of $4,000.arrow_forwardAna, Bea and Carol decided to form a partnership contributing the following items. Ana is to invest her existing business in the partnership consisting of the following accounts; cash of P20,000; accounts receivable of P50,000; inventory P30,000; fixtures of P40,000; payables of P12,000. Bea on the other hand is to invest cash of P15,000 and a delivery truck costing P30,000 but is mortgaged with the bank for P20,000. The partners agree that the receivables will re have a 90% realizable value. The inventory would be valued at P20,000. P5,000 of the payables would be paid prior to the formation of the partnership. The delivery truck would have a 20% increase in its market value. The partnership will shoulder only 80% of the mortgage and Carol is to invest cash to be able to have a 40% interest in the partnership.How much cash should Carol invest in the newly formed partnership?A. 61,200 B. 138,000 C. 60,800 D. 102,000arrow_forwardBatman and Robin agree to form a partnership. Batman is to contribute 135,600 cash and equipment that has a carrying value of 135,000 and a fair value of 115,000. The equipment however, has a mortgage attached to it and it is agreed by the partners that they will assume it. Robin, on the other hand contributed 240,000 cash. They share profits and losses in the ratio of 4:5. Furthermore, part of their agreement is to bring their initial capital in conformity with their profit and loss ratio.How much is the mortgage of the equipment? Pls provide solutionA. 58,600 B. 10,600 C. 78,600 D. 34,600arrow_forward

College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning

College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning