Videos

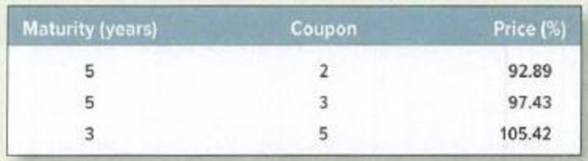

Prices and spot interest rates What spot interest rates are implied by the following Treasury bonds? Assume for simplicity that the bonds pay annual coupons. The price of a one-year strip is 97.56%, and the price of a four-year strip is 87.48%.

To determine: The spot interest rates implied by treasury bonds.

Explanation of Solution

Determine

Hence,

Determine

Hence,

Determine

Determine

Solve equation 1 and 2

Determine

Hence, the spot rates are 2.50%, 3.22%, 3.09%, 3.40% and 3.60 for years 1 to 5.

Want to see more full solutions like this?

Chapter 3 Solutions

PRIN.OF CORPORATE FINANCE

- Forecasting interest rates Assume the current interest rate on a one-year treasury bond(1R1) is 4.50 percent, the current rate on a two-year treasury bond (1R2) is 5.25 percent, and the current rate on a three-year treasury bond (1R3) is 6.50 percent. If the unbiased expectations theory of the term structure of interest rates is correct, what is the one-year forward rate expected on treasury bills during year 3, 3f1?arrow_forwardInterest premium. Estimate the default premium and the maturity premium given the following three investment opportunities: a Treasury bill with a current interest rate of 3.25%; a Treasury bond with a twenty-year maturity and a current interest rate of 4.5%; and a AAA, corporate bond with a twenty-year maturity and an interest rate of 9%. What is the default premium? % (Round to two decimal places.)arrow_forwardEstimate the default premium and the maturity premium given the following three investment opportunities: a Treasury bill with a current interest rate of 3.5%; a Treasury bond with a twenty-year maturity and a current interest rate of 5.25%; and a AAA, corporate bond with a twenty-year maturity and an interest rate of 7.5%. What is the default premium? nothing% (Round to two decimal places.)arrow_forward

- If the interest rates on 1-, 5-, 20-, and 30-year bonds are (respectively)4%, 5%, 6%, and 7%, then how would you describe the yield curve?How would you describe it if the rates were reversed?arrow_forwardThe outstanding bonds of Winter Tires Inc. provide a real rate of return of 3.2 percent. If the current rate of inflation is 2.1 percent, what is the actual nominal rate of return on these bonds?arrow_forwardConsider information on the following bonds (with face value 100): Bond Maturity (years) Coupon rate Yield-to-maturity А 1 0% 5.0% В 2 5% 5.5% C 3 6% 6.0% Coupons are paid annually. What is the three-year spot interest rate?arrow_forward

- Suppose you can observe that 1-year bond interest rate is 4%, 2-year bond interest rate is 8%, and 3-year bond interest rate is 10% at time t. It is also known that the term premium on a 2-year bond is 1% and the term premium on a 3-year bond is 1.5%. a) What are the market's expected 1-year bond interest rates for the next two years from time t? b) How to interpret those expected short-term interest rates? (what would be the "possible" economic meanings in the expected short- term interest rates?) Discuss as least two "candidates" to explain them.arrow_forwardSuppose that the current one-year rate (one-year spot rate) and expected one-year government bonds over years 2, 3 and 4 are as follows: 1R1 = 4.80%, E(2r1) = 5.45%, E(3r1) = 5.95%, E(4r1) = 6.10% Assume that there are no liquidity premiums. To the nearest basis point, what is the current rate for the four-year-maturity government bond? 5.57% 5.62% 5.83% 6.10%arrow_forwardSuppose that the prices of zero-coupon bonds with various maturities are given in the following table. The face value of each bond is $1,000. Maturity (Years) Price 1 $ 998.78 2 880.89 3 815.92 4 752.40 5 685.70 a. Calculate the forward rate of interest for each year. (Round your answers to 2 decimal places.) b. How could you construct a 1-year forward loan beginning in year 3? (Round your Rate of synthetic loan answer to 2 decimal places.) c. How could you construct a 1-year forward loan beginning in year 4? (Round your answers to 2 decimal places.)arrow_forward

- Suppose that the market interest rate rises overnight from 3.5% to 8%. Calculate the present values of the 5.5%, 3-year bond and of the 5.5%, 30-year bond both before and after this change in interest rates. Which bond price fluctuates more to interest rate change? Why?arrow_forwardThe following information is about the spot rates on Treasury securities and BBB corporate bond: Spot 1 Year Spot 2 Year Spot 3 Year Treasury 3% 4.75% 5.5% BBB Corporate Debt 7.5% 9.15% 10.5% Question: Using the implied forward rates, estimate the annual marginal default probability for the one-year BBB corporate debt in year 3?arrow_forwardSuppose that the prices of zero-coupon bonds with various maturities are given in the following table. The face value of each bond is $1,000. Maturity (Years) 1 2 3 4 5 Required: a. Calculate the forward rate of interest for each year. b. How could you construct a 1-year forward loan beginning in year 3? c. How could you construct a 1-year forward loan beginning in year 4? Required A Price $940.93 Complete this question by entering your answers in the tabs below. 868.39 800.92 735.40 670.48 Required B Maturity (years) 2 3 Calculate the forward rate of interest for each year. Note: Round your answers to 2 decimal places. Required C Forward Rate % % Prov 12 of 12 Nextarrow_forward

Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education