Concept explainers

Videos

Optima Company is a high-technology organization that produces a mass-storage system. The design of Optima’s system is unique and represents a breakthrough in the industry. The units Optima produces combine positive features of both compact and hard disks. The company is completing its fifth year of operations and is preparing to build its

- a. Fourth-quarter sales for 20X0 are 55,000 units.

- b. Unit sales by quarter (for 20X1) are projected as follows:

The selling price is $400 per unit. All sales are credit sales. Optima collects 85% of all sales within the quarter in which they are realized; the other 15% is collected in the following quarter. There are no

- c. There is no beginning inventory of finished goods. Optima is planning the following ending finished goods inventories for each quarter:

- d. Each mass-storage unit uses 5 hours of direct labor and three units of direct materials. Laborers are paid $10 per hour, and one unit of direct materials costs $80.

- e. There are 65,700 units of direct materials in beginning inventory as of January 1, 20X1. At the end of each quarter, Optima plans to have 30% of the direct materials needed for next quarter’s unit sales. Optima will end the year with the same amount of direct materials found in this year’s beginning inventory.

- f. Optima buys direct materials on account. Half of the purchases are paid for in the quarter of acquisition, and the remaining half are paid for in the following quarter. Wages and salaries are paid on the 15th and 30th of each month.

- g. Fixed overhead totals $1 million each quarter. Of this total, $350,000 represents depreciation. All other fixed expenses are paid for in cash in the quarter incurred. The fixed overhead rate is computed by dividing the year’s total fixed overhead by the year’s budgeted production in units.

- h. Variable overhead is budgeted at $6 per direct labor hour. All variable overhead expenses are paid for in the quarter incurred.

- i. Fixed selling and administrative expenses total $250,000 per quarter, including $50,000 depreciation.

- j. Variable selling and administrative expenses are budgeted at $10 per unit sold. All selling and administrative expenses are paid for in the quarter incurred.

- k. The balance sheet as of December 31, 20X0, is as follows:

- l. Optima will pay quarterly dividends of $300,000. At the end of the fourth quarter, $2 million of equipment will be purchased.

Required:

Prepare a master budget for Optima Company for each quarter of 20X1 and for the year in total. The following component budgets must be included:

- 1. Sales budget

- 2. Production budget

- 3. Direct materials purchases budget

- 4. Direct labor budget

- 5. Overhead budget

- 6. Selling and administrative expenses budget

- 7. Ending finished goods inventory budget

- 8. Cost of goods sold budget (Note: Assume that there is no change in work-in-process inventories.)

- 9.

Cash budget - 10. Pro forma income statement (using absorption costing) (Note: Ignore income taxes.)

- 11. Pro forma balance sheet (Note: Ignore income taxes.)

1.

Construct sales budget.

Explanation of Solution

Budgets:

Budgets are prepared for the planning and controlling purposes. Budgets facilitate planning and making decisions to achieve the desired objectives and are prepared to enable comparison between actual and expected outcomes.

Sales budget:

| Particulars |

Q1 ($) |

Q2 ($) |

Q3 ($) |

Q4 ($) |

Total ($) |

| Sales units (A) | 65,000 | 70,000 | 75,000 | 90,000 | 300,000 |

| Selling price (B) | 400 | 400 | 400 | 400 | |

| Sales | 26,000,000 | 28,000,000 | 30,000,000 | 36,000,000 | 120,000,000 |

Table (1)

2.

Construct production budget.

Explanation of Solution

Production budget:

| Particulars |

Q1 ($) |

Q2 ($) |

Q3 ($) |

Q4 ($) |

Total ($) |

| Expected sales | 65,000 | 70,000 | 75,000 | 90,000 | 300,000 |

| Add: Closing units. | 13,000 | 15,000 | 20,000 | 10,000 | 58,000 |

| Less: Opening units. | 0 | 13,000 | 15,000 | 20,000 | 48,000 |

| Production units | 78,000 | 72,000 | 80,000 | 80,000 | 310,000 |

Table (2)

Working Notes:

- Opening units are closing units of previous quarter.

- Production units are computed by adding closing units and subtracting opening units from the expected sales.

3.

Construct direct material purchases budget.

Explanation of Solution

Materials purchases budget:

| Particulars |

Q1 ($) |

Q2 ($) |

Q3 ($) |

Q4 ($) |

Total ($) |

| Expected material required for production | 234,000 | 216,000 | 240,000 | 240,000 | 930,000 |

| Add: Closing units. 30% of sales units of next month | 63,000 | 67,500 | 81,000 | 65,700 | 65,700 |

| Less: Opening units. | 65,700 | 63,000 | 67,500 | 81,000 | 65,700 |

| Material units expected to be purchased (A) | 231,300 | 220,500 | 253,500 | 224,700 | 930,000 |

|

Material cost: $80 per unit | 18,504,000 | 17,640,000 | 20,280,000 | 17,976,000 | 74,400,000 |

Table (3)

4.

Construct direct labor budget.

Explanation of Solution

Direct labor budget:

| Particulars |

Q1 ($) |

Q2 ($) |

Q3 ($) |

Q4 ($) |

Total ($) |

| Expected production (A) | 78,000 | 72,000 | 80,000 | 80,000 | 310,000 |

| Hours per unit (B) | 5 | 5 | 5 | 5 | 5 |

|

Number of hours | 390,000 | 360,000 | 400,000 | 400,000 | 1,550,000 |

| Rate per hour | 10 | 10 | 10 | 10 | 10 |

| Labor cost | 3,900,000 | 3,600,000 | 4,000,000 | 4,000,000 | 15,500,000 |

Table (4)

5.

Construct overhead budget.

Explanation of Solution

Overhead budget:

| Particulars |

Q1 ($) |

Q2 ($) |

Q3 ($) |

Q4 ($) |

Total ($) |

| Number of hours (sub-part 4) (A) | 390,000 | 360,000 | 400,000 | 400,000 | 1,550,000 |

| Variable overhead | 2,340,000 | 2,160,000 | 2,400,000 | 2,400,000 | 9,300,000 |

| Fixed overhead (C) | 1,000,000 | 1,000,000 | 1,000,000 | 1,000,000 | 4,000,000 |

|

Total overhead | 3,340,000 | 3,160,000 | 3,400,000 | 3,400,000 | 13,300,000 |

Table (5)

6.

Construct selling and administrative expenses budget.

Explanation of Solution

Selling and administrative expenses budget:

| Particulars |

Q1 ($) |

Q2 ($) |

Q3 ($) |

Q4 ($) |

Total ($) |

| Number of sales units (A) | 65,000 | 70,000 | 75,000 | 90,000 | 300,000 |

| Variable expense | 650,000 | 700,000 | 750,000 | 900,000 | 3,000,000 |

| Fixed expense(C) | 250,000 | 250,000 | 250,000 | 250,000 | 1,000,000 |

|

Total overhead | 900,000 | 950,000 | 1,000,000 | 1,150,000 | 4,000,000 |

Table (6)

7.

Construct ending finished goods inventory budget.

Explanation of Solution

Ending goods inventory budget:

| Particulars |

Amount ($) |

| Material cost | 240 |

| Add: Labor cost | 50 |

| Add: Variable overheads | 30 |

| Add: Fixed overheads | 12.90 |

| Unit cost | 332.90 |

| Cost of ending goods | 3,329,000 |

Table (7)

8.

Construct COGS budget.

Explanation of Solution

Cost of goods sold budget:

| Particulars |

Amount ($) |

| Material cost | 74,400,000 |

| Add: Labor cost | 15,500,000 |

| Add: Variable overheads | 9,300,000 |

| Add: Fixed overheads | 4,000,000 |

| Manufacturing cost (A) | 103,200,000 |

| Add: Beginning finished goods | 0 |

| Cost of goods available for sale (A) | 103,200,000 |

| Less: Ending goods (sub-part 7) (B) | 3,329,000 |

| COGS | 99,871,000 |

Table (8)

9.

Construct cash budget.

Explanation of Solution

Cash Budget:

| Particulars |

Q1 ($) |

Q2 ($) |

Q3 ($) |

Q4 ($) |

Total ($) |

| Opening balance | 250,000 | 1,110,000 | 3,128,000 | 5,568,000 | 250,000 |

| Receipt from sales of current quarter |

22,100,000 |

25,500,000 | 102,000,000 | ||

| Receipts from sales of previous quarter | 3,300,000 |

3,900,000 |

4,200,000 |

4,500,000 | 15,900,000 |

| Less: Payment for material purchased in preceding quarter1 | 7,248,000 | 9,252,000 | 8,820,000 | 10,140,000 | 35,460,000 |

| Less: Payment for material purchased in current quarter |

9,252,000 |

8,820,000 |

10,140,000 |

8,988,000 | 37,200,000 |

| Less: labor cost | 3,900,000 | 3,600,000 | 4,000,000 | 4,000,000 | 15,500,000 |

| Less: Variable manufacturing Overhead cost | 2,340,000 | 2,160,000 | 2,400,000 | 2,400,000 | 9,300,000 |

| Less: Fixed manufacturing Overhead cost | 650,000 | 650,000 | 650,000 | 650,000 | 2,600,000 |

| Less: Variable Selling and administrative expense | 650,000 | 700,000 | 750,000 | 900,000 | 3,000,000 |

| Less: Fixed Selling and administrative expense | 200,000 | 200,000 | 200,000 | 200,000 | 800,000 |

| Less: Dividends | 300,000 | 300,000 | 300,000 | 300,000 | 1,200,000 |

| Less: acquisition of equipment | 2,000,000 | 2,000,000 | |||

| Closing balance | 1,110,000 | 3,128,000 | 5,568,000 | 11,090,000 | 11,090,000 |

Table (9)

Working Notes:

1. Computation of payment for material purchased in quarter 4 of the last year:

10.

Construct pro forma income statement.

Explanation of Solution

Budgeted income statement:

| Particulars |

Amount ($) |

| Sales | 120,000,000 |

| Less: COGS (sub-part 8) | 99,871,000 |

| Operating profit | 20,129,000 |

| Less: Selling and administrative expenses | 4,000,000 |

| Income | 16,129,000 |

Table (10)

11.

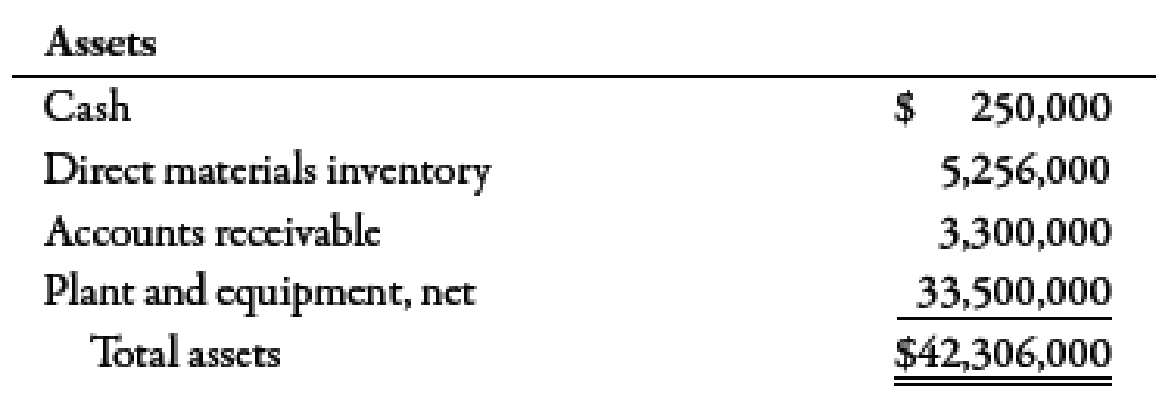

Construct pro forma balance sheet.

Explanation of Solution

Budgeted Balance Sheet:

| Particulars |

Amount ($) |

| Assets: | |

| Cash | 11,090,000 |

| Direct material inventory | 5,256,000 |

| Accounts receivable | 5,400,000 |

| Finished goods inventory | 3,329,000 |

| Plant and equipment | 33,900,000 |

| Total Assets | 58,975,000 |

| Liabilities and Equity: | |

| Accounts payable | 8,988,000 |

| Capital stock | 27,000,000 |

| Retained Earnings | 22,987,000 |

| Total liabilities and equity | 58,975,000 |

Table (11)

Working Notes:

1.

Computation of opening retained earnings:

Capital stock of $27,000,000 has been assumed.

Want to see more full solutions like this?

Chapter 9 Solutions

Managerial Accounting: The Cornerstone of Business Decision-Making

- Optima Company is a high-technology organization that produces a mass-storage system. The design of Optima’s system is unique and represents a breakthrough in the industry. The units Optima produces combine positive features of both compact and hard disks. The company is completing its fifth year of operations and is preparing to build its master budget for the coming year (2019). The budget will detail each quarter’s activity and the activity for the year in total. The master budget will be based on the following information: a. Fourth-quarter sales for 2018 are 55,000 units. b. Unit sales by quarter (for 2018) are projected as follows: First quarter 65,000 Second quarter 70,000 Third quarter 75,000 Fourth quarter 90,000 The selling price is $400 per unit. All sales are credit sales. Optima collects 85 percent of all sales within the quarter in which they are realized; the other 15 percent is collected in the following quarter. There are no bad debts. c. There is no beginning…arrow_forwardOptima Company is a high-technology organization that produces a mass-storage system. The design of Optima’s system is unique and represents a breakthrough in the industry. The units Optima produces combine positive features of both compact and hard disks. The company is completing its fifth year of operations and is preparing to build its masterbudget for the coming year (20X1). The budget will detail each quarter’s activity and the activity for the year in total. The master budget will be based on the following information:a. Fourth-quarter sales for 20X0 are 55,000 units.b. Unit sales by quarter (for 20X1) are projected as follows: First quarter 65,000 Second quarter 70,000 Third quarter 75,000 Fourth quarter 90,000 The selling price is $400 per unit. All sales are credit sales. Optima collects 85% of all sales within the quarter in which they are realized; the other 15% is collected in the following quarter. There are no bad debts. C .There is no beginning inventory of…arrow_forwardOptima Company is a high-technology organization that produces a mass-storage system. The design of Optima’s system is unique and represents a breakthrough in the industry. The units Optima produces combine positive features of both compact and hard disks. The company is completing its fifth year of operations and is preparing to build its master budget for the coming year (2019). The budget will detail each quarter’s activity and the activity for the year in total. The master budget will be based on the following information: a. Fourth-quarter sales for 2018 are 55,000 units. b. Unit sales by quarter (for 2018) are projected as follows: First quarter 65,000 Second quarter 70,000 Third quarter 75,000 Fourth quarter 90,000 The selling price is $400 per unit. All sales are credit sales. Optima collects 85 percent of all sales within the quarter in which they are realized; the other 15 percent is collected in the following quarter. There are no bad debts. c. There is no beginning…arrow_forward

- Optima Company is a high-technology organization that produces a mass-storage system. Thedesign of Optima’s system is unique and represents a breakthrough in the industry. The unitsOptima produces combine positive features of both compact and hard disks. The company iscompleting its fifth year of operations and is preparing to build its master budget for the comingyear (20X1). The budget will detail each quarter’s activity and the activity for the year in total.The master budget will be based on the following information:a. Fourth-quarter sales for 20X0 are 55,000 units.b. Unit sales by quarter (for 20X1) are projected as follows:First quarter 65,000Second quarter 70,000Third quarter 75,000Fourth quarter 90,000The selling price is $400 per unit. All sales are credit sales. Optima collects 85% of all saleswithin the quarter in which they are realized; the other 15% is collected in the followingquarter. There are no bad debts.c. There is no beginning inventory of finished goods. Optima…arrow_forwardCreate a budget for the following project: Blazer Company plans on purchasing new equipment to retool its manufacturing process. The project will involve the acquisition of equipment, installation of the new equipment, selling off the old equipment and training the workforce on the new equipment and processes. Blazer expects this project to take two years from beginning to end. Costs and expected income for the project are as shown below. Your task is to create a two-year cash budget for the project and compute a return on investment (ROI) for the project. You may ignore the time value of money in your calculation. You may make reasonable assumptions to complete this problem so long as you document them. Facts: a. The equipment to be purchased will cost $455,000. The equipment will be purchased and paid for at the beginning of Year 1. b. Installation cost will be $55,000. c. Blazer will purchase a maintenance contract for the equipment. The first year of maintenance is included in the…arrow_forwardIona Company, a large printing company, is in its fourth year of a five-year, quality improvement program. The program began in 20x0 with an internal study that revealed the quality costs being incurred. In that year, a five-year plan was developed to lower quality costs to 10 percent of sales by the end of 20x5. Sales and quality costs for each year are as follows: Budgeted figures. Quality costs by category are expressed as a percentage of sales as follows: The detail of the 20x5 budget for quality costs is also provided. All prevention costs are fixed; all other quality costs are variable. During 20x5, the company had 12 million in sales. Actual quality costs for 20x4 and 20x5 are as follows: Required: 1. Prepare an interim quality cost performance report for 20x5 that compares actual quality costs with budgeted quality costs. Comment on the firms ability to achieve its quality goals for the year. 2. Prepare a one-period quality performance report for 20x5 that compares the actual quality costs of 20x4 with the actual costs of 20x5. How much did profits change because of improved quality? 3. Prepare a graph that shows the trend in total quality costs as a percentage of sales since the inception of the quality improvement program. 4. Prepare a graph that shows the trend for all four quality cost categories for 20x1 through 20x5. How does this graph help management know that the reduction in total quality costs is attributable to quality improvements? 5. Assume that the company is preparing a second five-year plan to reduce quality costs to 2.5 percent of sales. Prepare a long-range quality cost performance report assuming sales of 15 million at the end of five years. Assume that the final planned relative distribution of quality costs is as follows: proofreading, 50 percent; other inspection, 13 percent; quality training, 30 percent; and quality reporting, 7 percent.arrow_forward

- Jay Rexford, president of Photo Artistry Company, was just concluding a budget meeting with his senior staff. It was November of 20x1, and the group was discussing preparation of the firm’s master budget for 20x2. “I've decided to go ahead and purchase the industrial robot we’ve been talking about. We’ll make the acquisition on January 2 of next year, and I expect it will take most of the year to train the personnel and reorganize the production process to take full advantage of the new equipment.” In response to a question about financing the acquisition, Rexford replied as follows: “The robot will cost $950,000. There will also be an additional $50,000 in ancillary equipment to be purchased. We’ll finance these purchases with a one‑year $1,000,000 loan from Shark Bank and Trust Company. I’ve negotiated a repayment schedule of four equal installments on the last day of each quarter. The interest rate will be 10 percent, and interest payments will be quarterly as well.” With…arrow_forwardSandhill's Recording Studio rents studio time to musicians in two-hour blocks. Each session includes the use of the studio facilities, a digital recording of the performance, and a professional music producer/mixer. Anticipated annual volume is 1.400 sessions. The company has invested $2,073,750 in the studio and expects a return on investment of 20%. Budgeted costs for the coming year are as -follows: Direct materials (tapes, CDs, etc.) Direct labour Variable overhead Fixed overhead Variable selling and administrative expenses Fixed selling and administrative expenses (a) Determine the total cost per session. Total cost per session Per Session $25 380 60 35 Total $1,358,000 707,000arrow_forwardWildhorse's Recording Studio rents studio time to musicians in two-hour blocks. Each session includes the use of the studio facilities, a digital recording of the performance, and a professional music producer/mixer. Anticipated annual volume is 1,400 sessions. The company has invested $2,212,000 in the studio and expects a return on investment of 20%. Budgeted costs for the coming year are as follows: (a) Per Session Total Direct materials (tapes, CDs, etc.) $20 Direct labour 400 Variable overhead 45 Fixed overhead $1,330,000 Variable selling and administrative expenses 40 Fixed selling and administrative expenses 728,000 Your answer is correct. Determine the total cost per session. Total cost per session $ 1975 SUPPORarrow_forward

- Blossom's Recording Studio rents studio time to musicians in two-hour blocks. Each session includes the use of the studio facilities, a digital recording of the performance, and a professional music producer/mixer. Anticipated annual volume is 1,000 sessions. The company has invested $1,963,500 in the studio and expects a return on investment of 20%. Budgeted costs for the coming year are as follows: Per Session Total Direct materials (tapes, CDs, etc.) $20 Direct labour. 380 Variable overhead 40 Fixed overhead $925,000 Variable selling and administrative expenses 30 Fixed selling and administrative expenses 475,000arrow_forwardGrouper's Recording Studio rents studio time to musicians in 2-hour blocks. Each session includes the use of the studio facilities, a digital recording of the performance, and a professional music producer/mixer. Anticipated annual volume is 1,020 sessions. The company has invested $2,299,080 in the studio and expects a return on investment (ROI) of 20%. Budgeted costs for the coming year are as follows. Direct materials (CDs, etc.) Direct labor Variable overhead Fixed overhead Variable selling and administrative expenses $40 Fixed selling and administrative expenses (a) Per Session $20 $395 $45 Your Answer Correct Answer Total $974,100 $515,100arrow_forwardYou have just been hired as a management trainee by Benjamin’s Fashions, a nationwide distributor of a designer's silk ties. The company has an exclusive franchise on the distribution of the ties, and sales have grown so rapidly over the last few years that it has become necessary to add new members to the management team. You have been given responsibility for all planning and budgeting. Your first assignment is to prepare a master budget for the next 12 months starting January 1, 2022. You are anxious to make a favorable impression on the president and have assembled the information below. The company desires a minimum ending cash balance each month of $10,000. The ties are sold to retailers for $8.00 each (75% of total sales, all on account) and $10.00 each to the individual customers in the mall stores (25% of total sales, all in cash). Recent and forecasted sales in units are as follows: Months Units Months…arrow_forward

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning