Concept explainers

Videos

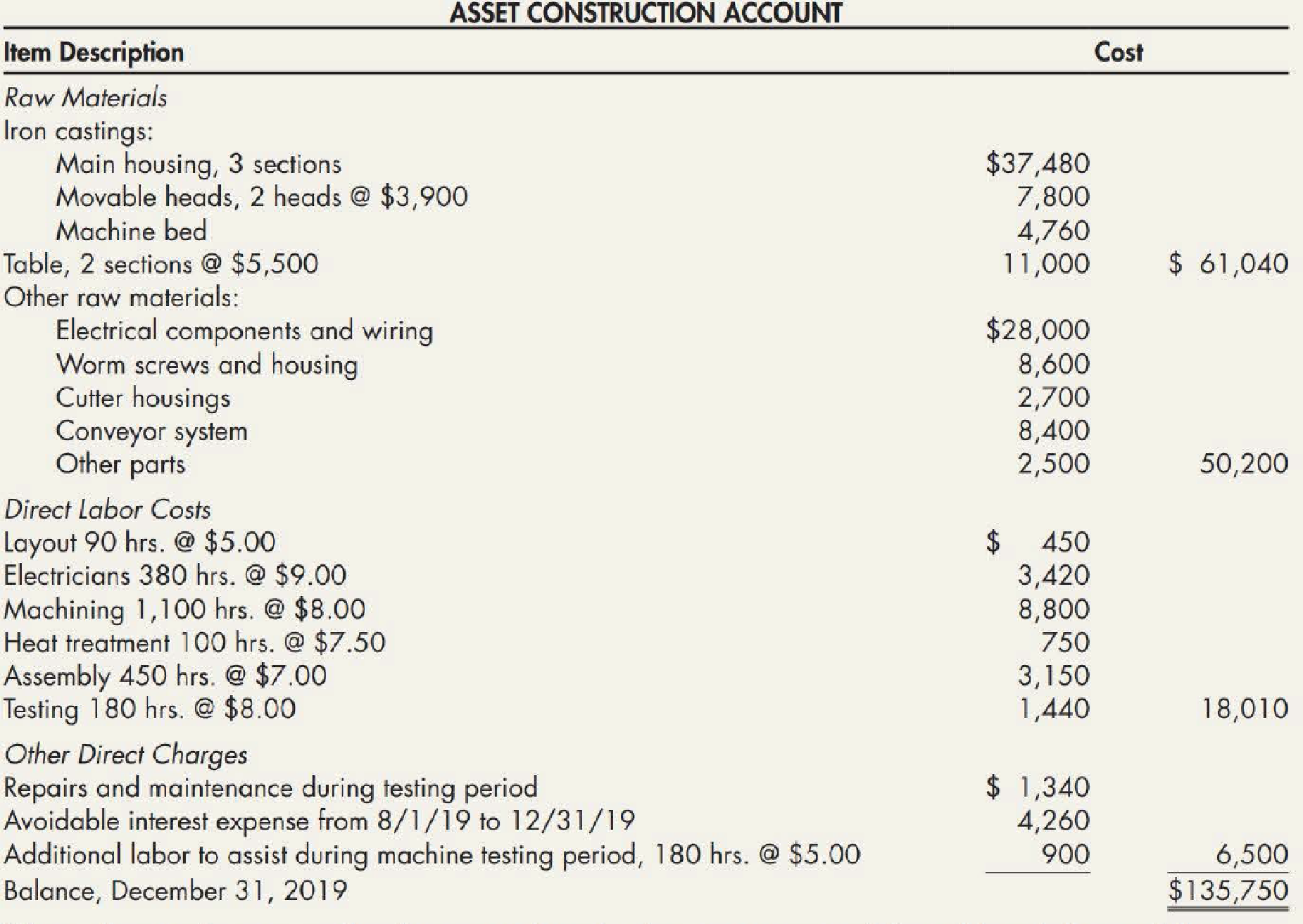

Self-Construction Olson Machine Company manufactures small and large milling machines. Selling prices of these machines range from $35,000 to $200,000. During the 5-month period from August 1, 2019, through December 31, 2019, Olson manufactured a milling machine for its own use. This machine was built as part of the regular production activities. The project required a large amount of time front planning and supervisory personnel, as well as that of some of the company’s officers, because it was a more sophisticated type of machine than the regular production models.

Throughout the 5-month period, Olson charged all costs directly associated with the construction of the machine to a special account entitled “Asset Construction Account.” An analysis of the charges to this account as of December 31, 2019, follows:

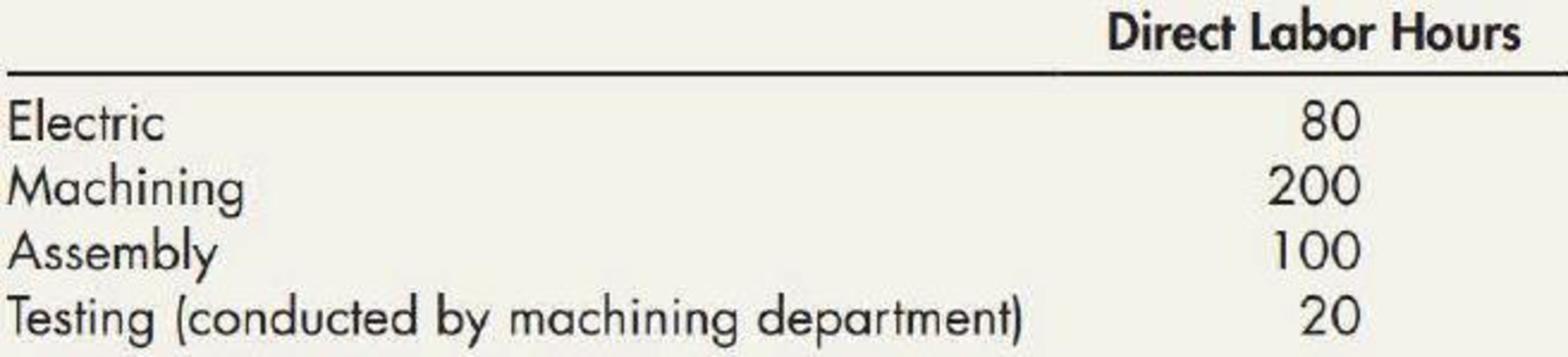

Olson allocates factory

Olson uses a flat rate of 40% of direct labor dollars to allocate general and administrative overhead.

During the machine testing period, a cutter head malfunctioned and did extensive damage to the machine table and one cutter housing. This damage was not anticipated and was the result of an error in the assembly operation. Although no additional raw materials were needed to make the machine operational after the accident, the following labor for rework was required:

Olson has included all these labor charges in the asset construction account. In addition, it included in the account the repairs and maintenance charges of $1,340 that it incurred as a result of the malfunction.

Required:

- 1. Compute, consistent with GAAP and common practice, the amount that Olson should capitalize for the milling machine as of December 31, 2019, when it declares the machine operational.

- 2. Next Level Identify the costs you included in Requirement 1 for which there are acceptable alternative procedures. Describe the alternative procedure(s) in each case.

1.

Calculate the amount that Company O must capitalize for the milling machine as of December 31, 2019.

Explanation of Solution

Cost of self-constructed assets:

Company sometimes constructs an item of “property, plant and equipment” which is used in the business operations and these are known as self-constructed assets. The cost of self-constructed assets comprises of expenses that are required to build an asset and put it in operating condition.

| Particulars | Amount ($) | Amount ($) |

| Raw materials: | ||

| Iron castings | 61,040 | |

| Other raw materials. | 50,200 | $111,240 |

| Direct labor: | ||

| Layout (1) | $450 | |

| Electricians (2) | 2,700 | |

| Machinery (3) | 7,200 | |

| Heat treatment (4) | 750 | |

| Assembly (5) | 2,450 | |

| Testing (6) | 1,280 | |

| Additional testing labor (7) | 800 | 15,630 |

| Factory overhead: | ||

| Layout and electricians (8) | $2,205 | |

| Machining, heat treatment, assembly, testing (9) | ||

| 12,480 | 14,685 | |

| Interest paid | 4,260 | |

| Total amount to be capitalized | 145,815 |

Table (1)

Working notes:

(1)Calculate the amount of direct labor costs for layout:

(2)Calculate the amount of direct labor costs for electricians:

(3)Calculate the amount of direct labor costs for machinery:

(4)Calculate the amount of direct labor costs for Heat treatment:

(5)Calculate the amount of direct labor costs for assembly:

(6)Calculate the amount of direct labor costs for testing:

(7)Calculate the amount of direct labor costs for additional testing labor:

(8)Calculate the factory overhead for layout and electricians:

(9)Calculate the factory overhead for machinery, heat treatment, assembly and testing:

2.

Ascertain the costs included in requirement 1 for which there are acceptable alternative procedures and explain the alternative procedures for each case.

Explanation of Solution

“Alternate procedures are probable for two costs— factory overhead and rework costs (affects direct labor, repairs and maintenance, and factory overhead)”

- Rework costs must be taken as cost for the period in which they are nonstandard. Rework costs rising from errors that must not have incurred should be considered as losses of the period. Seemingly, this was the case in this condition since the impairment resulted from a type of error that is not expected. Accordingly, related repairs, maintenance expenses and rework costs are not capitalized in requirement 1.

- Two alternative ways are there to allocate overhead costs to self-constructed assets. The method followed in “requirement 1” is to allot a portion of all overhead costs to the self-constructed asset. The reason which justifies this particular treatment is that all productive output must absorb its proportionate share of all factory overhead costs. Additionally, this method result in a cost of the constructed asset that approximates the cost of the equivalent asset acquired.

- Capitalizing the incremental overhead, that is traceable fixed and variable overhead is the second method that increases as a result of construction. Additional costs occurred in production of the fixed asset (part of the assets’ cost) are included in this method. Traceable fixed overhead and variable overhead are occurred to build the asset and it will be advantageous in the upcoming periods therefore, these costs must be capitalized.

- If there is no relationship between the self-constructed asset and fixed overhead costs, non-traceable fixed overhead costs will be incurred so, these costs must not be capitalized.

Want to see more full solutions like this?

Chapter 10 Solutions

Intermediate Accounting: Reporting And Analysis

- Zachary manufacturing company makes tents that it sells directly to camping enthusiasts through a mail-order marketing program. The company pays a quality control expert $121600 per year to inspect completed tents before they are shipped to customers. assume that the company completed 1,530 tents in January and 1,240 tents in February. For the entire year, the company expects to produce 19000 tents. required c) If the cost objective is to determine the cost per tent, is the expert's salary a direct or an indirect cost? D) How much of the expert's salary should be allocated to tents produced in January and February? If the cost objective is to determine the cost per tent is the expert's salary a direct or an indirect cost?arrow_forwardThe F Inc.’s materials manager is considering the installation of a just-in-time (JIT) inventory system for L-20, one of the chemicals used in the production process. Currently, the chemical is purchased for $30 each pound. The firm uses 4,800 pounds L-20 per year. The controller estimates that it costs $150 to place and receive a typical order of L-20. The annual cost of storing L-20 is $1 per pound. F Inc.’s manufacturing engineering team identifies the following effects of adopting a JIT inventory system: 1) F Inc. will order 100 pounds L-20 each time. 2) The cost of placing an order for L-20 will be reduced to $20. 3) Suppliers would add $4 to the price per pound for frequent deliveries. 4) Currently there is a defect-assessment cost of $120,000 per year. This cost is expected a reduction of 20% under the JIT system. F Inc. requires a 10% annual rate of return on investment Required: From a financial perspective, determine whether it is in the best interest of F to…arrow_forwardTo automate one of its production processes, Milwaukee Corporation bought three flexible manufacturing cells at a price of $400,000 each. When they were delivered, Milwaukee paid freight charges of $30,000 and handling fees of $15,000. Site preparation for these cells cost $50,000. Six employees, each earning $15 an hour, worked five 40-hour weeks to set up and test the manufacturing cells. Special wiring and other materials applicable to the new manufacturing cells cost $2,000. Determine the cost basis (the amount to be capitalized) for these cells.arrow_forward

- At the beginning of last year (2021), Richter installed a semi-auto machine for its production. The owner of the company, Ron Richter, recently returned from an industry equipment exhibition where he watched a computerized machine. He was impressed with the production efficiency, and less labour intensive. Upon returning from the exhibition, he asked his purchasing agent to collect price and operating cost data on the new model. In addition, he asked the company's accountant to provide him with cost data on the company's old model. This information is presented here. Purchase price Accumulated Depreciation Estimated useful life from now Depreciation method Annual operating costs other than depreciation: Variable Fixed Old $105,500 50,000 5 years Straight-line $35,000 25,000 New $255,000 0 5 years Straight-line $15,000 10,000 If the old elevator is replaced now, at the beginning of 2022, Richter Condos will be able to sell it for $35,000. What Richter should do and provide your…arrow_forwardThe engineering department have appointed you on a task purchasing new forklift to transport sheet metal part. From your research, two types of forklift have been finalized as shown in Table 1 for their material handling plan in 6 years. The company also has another option; using manual material handling with 3 workers and the salary of each worker is RM1,200 per month. Suggest TWO (2) decisions on material handling alternatives to the company with suitable assumptions.arrow_forwardThe management of Shatner Manufacturing Company is trying to decide whether to continue manufacturing a part or to buy it from an outside supplier. The part, called CISCO, is a component of the company’s finished product.The following information was collected from the accounting records and production data for the year ending December 31, 2020.1. 8,000 units of CISCO were produced in the Machining Department.2. Variable manufacturing costs applicable to the production of each CISCO unit were: direct materials $5.23, direct labor $4.71, indirect labor $0.48, utilities $0.39.3. Fixed manufacturing costs applicable to the production of CISCO were: Cost Item Direct Allocated Depreciation $2,100 $960 Property taxes 500 370 Insurance 910 650 $3,510 $1,980 All variable manufacturing and direct fixed costs will be eliminated if CISCO is purchased. Allocated costs will not be eliminated if CISCO is purchased. So if CISCO is purchased,…arrow_forward

- The Rainier Company provides landscaping services to corporations and businesses. 11-2 All its landscaping work requires Rainier to use landscaping equipment. Its land scaping equipment has the capacity to do 10,000 hours of landscaping work. It cur rently anticipates getting orders that would utilize 9,000 hours of equipment time from existing customers. Rainier charges $80 per hour for landscaping work. Cost information for the current expected activity level is as follows:arrow_forwardPERBANAS, Inc. installs heating systems in new homes built in the southern tier counties of New York state. Jobs are priced using the time and materials method. The president of PERBANAS, Fenturini, is pricing a job involving the heating systems for six houses to be built by a local developer. He has made the following estimates. Material cost $ 30,000 Labor hours 200 The following predictions pertain to the company’s operations for the next year. Labor rate, including fringe benefits $ 8.00 per hour Annual labor hours 6,000 hours Annual overhead costs: Material handling and storage $ 12,500 Other overhead costs $ 54,000 Annual cost of materials used $ 125,000 Perbanas adds a markup of $ 2 per hour on its time charges, but there is no markup on material costs. Required: 1. Calculate the company's time charges and the material charges percentage. 2. Compute the price for the job 3. What would be the price of the job if Perbanas also added a markup of 5 % on all material charges…arrow_forwardBonita Inc., a manufacturer of steel school lockers, plans to purchase a new punch press for use in its manufacturing process. After contacting the appropriate vendors, the purchasing department received differing terms and options from each vendor. The Engineering Department has determined that each vendor's punch press is substantially identical and each has a useful life of 20 years. In addition, Engineering has estimated that required year-end maintenance costs will be $1,030 per year for the first 5 years, $2,030 per year for the next 10 years, and $3,030 per year for the last 5 years. Following is each vendor's sales package. Vendor A: $58,000 cash at time of delivery and 10 year-end payments of $16,360 each. Vendor A offers all its customers the right to purchase at the time of sale a separate 20-year maintenance service contract, under which Vendor A will perform all year-end maintenance at a one-time initial cost of $9,640. Vendor B: Forty semiannual payments of $9,120 each,…arrow_forward

- Paradise Bay Shop is a manufacturer of golf carts. Peter Cranston, the plant manager of Paradise Bay, obtains the following information for Job # 22 in August 2020. A total of 23 units were started, and 3 spoiled units were detected and rejected at final inspection, yielding 20 good units. The spoiled units were considered to be normal spoilage. Costs assigned prior to the inspection point are $1,300 per unit. Assume that Job #22 of Paradise Bay Shop generates scrap with a total sales value of $400 (it is assumed that scrap returned to the storeroom is sold quickly). Read the requirements. Prepare the journal entries for the recognition of scrap, assuming the following: (Record debits first, then credits. Exclude explanations from any journal entries.) a. The value of scrap is immaterial and scrap is recognized at the time of sale. Journal Entry Accounts Debit (...) Credit Requirements Prepare journal entries for the recognition of scrap, assuming the following: The value of scrap is…arrow_forwardSouthern Tier Heating, Inc. installs heating systems in new homes built in the southern tier counties of New York state. Jobs are priced using the time and materials method. The president of Southern Tier Heating, EIwing, is pricing a job involving the heating systems for six houses to be built by a local developer. He has made the following estimates. Material cost $ 60,000 Labor hours 400 The following predictions pertain to the company’s operations for the next year. Labor rate, including fringe benefits $ 16.00 per hour Annual labor hours 12,000 hours Annual overhead costs: Material handling and storage $ 25,000 Other overhead costs $ 108,000 Annual cost of materials used $ 250,000 Perbanas adds a markup of $ 4 per hour on its time charges, but there is no markup on material costs. Required: 1. Calculate the company's time charges and the material charges percentage. 2. Compute the price for the job 3. What would be the price of the job if Perbanas also added a markup of 10 % on…arrow_forward. ABP Sakalam Corporation manufactures and assembles electronic motor drives for video cameras. The company assembles the motor drives for several accounts. The process consists of a just-in-time cell for each customer. The following information relates only to one customer's just-in-time cell for the coming year. Projected labor and overhead, Php4,800,000; materials costs, P25 per unit. Planned production included 2,400 hours to produce 19,200 motor drives. Actual production for August was 1,300 units, and motor drives shipped amounted to 1,260 units. 28. From the foregoing information, determine the budgeted cell conversion cost per unit.arrow_forward

- Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning