Concept explainers

Videos

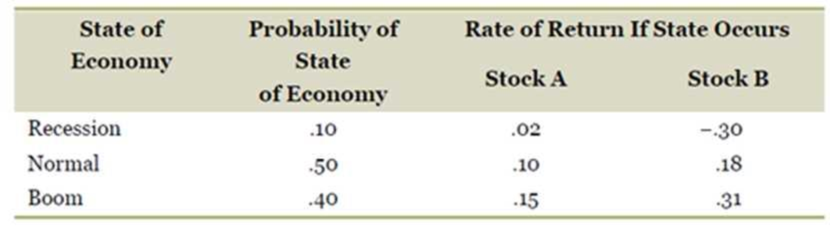

Calculating Returns and Standard Deviations. Based on the following information, calculate the expected return and standard deviation for the two stocks.

To determine: The expected return of Stock A and Stock B.

Introduction:

Expected return refers to the return that the investors expect on a risky investment in the future.

Answer to Problem 7QP

The expected return of Stock A is 11.20 percent.

The expected return of Stock B is 18.40 percent.

Explanation of Solution

Given information:

Stock A’s rate of return is 2 percent when the economy is in a recession, 10 percent when the economy is normal, and 15 percent when the economy is in a boom.

Stock B’s rate of return is −30 percent when the economy is in a recession, 18 percent when the economy is normal, and 31 percent when the economy is in a boom.

The probability of having a recession is 10 percent, the probability of having a normal economy is 50 percent, and the probability of having a booming economy is 40 percent.

The formula to calculate the expected return on the stock:

Where,

R1 refers to the rate of returns during the recession economy,

Rn refers to the rate of returns for “n” number of items,

P1 refers to the probability of having a recession economy,

Pn refers to the probability of having “n” number of economy.

Compute the expected return on Stock A:

Hence, the expected return on Stock A is 0.1120 or 11.20 percent.

Compute the expected return on Stock B:

Hence, the expected return on Stock B is 0.1840 or 18.40 percent.

To determine: The standard deviation of Stock A and Stock B.

Introduction:

Standard deviation refers to the variation in the actual returns from the expected returns.

Answer to Problem 7QP

The standard deviation of Stock A is 3.87 percent.

The standard deviation of Stock B is 17.26 percent.

Explanation of Solution

Given information:

Stock A’s rate of return is 2 percent when the economy is in a recession, 10 percent when the economy is normal, and 15 percent when the economy is in a boom.

Stock B’s rate of return is −30 percent when the economy is in a recession, 18 percent when the economy is normal, and 31 percent when the economy is in a boom.

The probability of having a recession is 10 percent, the probability of having a normal economy is 50 percent, and the probability of having a booming economy is 40 percent.

The formula to calculate the standard deviation of the stock:

Compute the standard deviation of Stock A:

Hence, the standard deviation of Stock A is 0.0387 or 3.87 percent.

Compute the standard deviation of Stock B:

Hence, the standard deviation of Stock B is 0.1726 or 17.26 percent.

Want to see more full solutions like this?

Chapter 11 Solutions

Essentials of Corporate Finance (Mcgraw-hill/Irwin Series in Finance, Insurance, and Real Estate)

- (a) A stock’s returns have the following distribution: Calculate the stock’s expected return, standard deviation, and the coefficient of variation.arrow_forwardWhen finding the covariance, should 2 stocks be used or can it be calculated using 1 stock and the market returns?arrow_forwardWhat is the correlation between returns of stock S and T, given that covariance between stocks is 2.419 and standard deviation are 1.23 and 2.21, respectively.arrow_forward

- KINDLY ANSWER PART 5,6.and 7 Using the stock price data for any two companies provided below carry out the following tasks: 1.Compute, for each asset: i.Total Returns ii.Expected returns iii.standard deviation iv.Correlation Coefficient 2.Construct the variance-covariance matrix 3.Construct equally weighted portfolio and calculate Expected Return, Standard Deviation and Sharpe ratio. 4.Reconstruct equally weighted portfolio and calculate Expected Return, Standard Deviation and Sharpe ratio. 5.Use Solver to determine optimal risky portfolio. 6.Create hypothetical portfolios (commencing from Weight A=0 and weight B=100) 7.Calculate Expected return and Standard Deviation for all the above combinations 8.Graph the efficient frontier 9.Graph the optimal portfolio 10.Assuming that the investors prefers lower level of risk than what a portfolio of risky assets offer, introduce a risk free asset in the portfolio with a return of 3% 11.Using hypothetical weights (A= Portfolio of Risky…arrow_forwarda. Calculate the expected return for Stock media Prima and Stock Astro 2. Calculate the standard deviation for Stock media Prima and Stock Astro 3. Calculate the covariance and correlation of coefficient for the above stock.arrow_forwardA price-weighted index such as the DJIA is a geometric mean of current stock prices. a. True b. Falsearrow_forward

- Using the stock price data for any two companies provided below carry out the following tasks: 1.Compute, for each asset: i.Total Returns ii.Expected returns iii.standard deviation iv.Correlation Coefficient 2.Construct the variance-covariance matrix 3.Construct equally weighted portfolio and calculate Expected Return, Standard Deviation and Sharpe ratio. 4.Reconstruct equally weighted portfolio and calculate Expected Return, Standard Deviation and Sharpe ratio. 5.Use Solver to determine optimal risky portfolio. 6.Create hypothetical portfolios (commencing from Weight A=0 and weight B=100) 7.Calculate Expected return and Standard Deviation for all the above combinations 8.Graph the efficient frontier 9.Graph the optimal portfolio 10.Assuming that the investors prefers lower level of risk than what a portfolio of risky assets offer, introduce a risk free asset in the portfolio with a return of 3% 11.Using hypothetical weights (A= Portfolio of Risky Assets, B= 1 Risk Free…arrow_forwarda. what is return on each of the three shortlisted stock? and what is the standard deviation of the rate of return on the three shortlisted stocks?arrow_forwardAhmed observed the following data of two stocks as shown in the below table. Which stock do you advise Ahmed to select according to the required rate of return? And explain why? (picture)arrow_forward

- Calculate the variance and standard deviation of each stockarrow_forwardThe Black-Scholes OPM is dependent on which five parameters? Select one: a. Stock price, exercise price, risk free rate, beta, and time to maturity b. Stock price, risk free rate, beta, time to maturity, and variance c. Stock price, exercise price, risk free rate, standard deviation and time to maturity d. Stock price, risk free rate, probability, standard deviation and exercise pricearrow_forwardThe table below contains the covariance matrix of stock returns and the market. Assume that the assumptions of CAPM hold. 1. Find the market risk. 2. Find the systematic risk of BlueChip.arrow_forward

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning