Concept explainers

Videos

Rios Financial Co. is a regional insurance company that began operations on January 1, Year 1. The following transactions relate to trading securities acquired by Rios Financial Co., which has a fiscal year ending on December 31:

Instructions

- 1.

Journalize the entries to record these transactions. - 2. Prepare the investment-related current asset

balance sheet presentation for Rios Financial Co. on December 31, Year 2. - 3. How are unrealized gains or losses on trading investments presented in the financial statements of Rios Financial Co.?

(1)

Journalize the stock investment transactions in the books of Company RF.

Explanation of Solution

Trading securities: These are short-term investments in debt and equity securities with an intention of trading and earning profits due to changes in market prices.

Journal entry: Journal entry is a set of economic events which can be measured in monetary terms. These are recorded chronologically and systematically.

Debit and credit rules:

- Debit an increase in asset account, increase in expense account, decrease in liability account, and decrease in stockholders’ equity accounts.

- Credit decrease in asset account, increase in revenue account, increase in liability account, and increase in stockholders’ equity accounts.

Prepare journal entry for the purchase of 7,500 shares of Company C, at $50 per share, and a brokerage commission of $75.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| Year 1 | |||||

| February | 1 | Investments–Company C Stock | 375,075 | ||

| Cash | 375,075 | ||||

| (To record purchase of shares for cash) | |||||

Table (1)

- Investments–Company R Stock is an asset account. Since stock investments are purchased, asset value increased, and an increase in asset is debited.

- Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Working Notes:

Compute amount of cash paid to purchase Company C’s stock.

Prepare journal entry for the purchase of 3,000 shares of Company H, at $42 per share, and a brokerage commission of $90.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| Year 1 | |||||

| May | 1 | Investments–Company H Stock | 126,090 | ||

| Cash | 126,090 | ||||

| (To record purchase of shares for cash) | |||||

Table (2)

- Investments–Company H Stock is an asset account. Since stock investments are purchased, asset value increased, and an increase in asset is debited.

- Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Working Notes:

Compute amount of cash paid to purchase Company H’s stock.

Prepare journal entry for sale of 4,500 shares of Company C, at $46, with a brokerage of $110.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| Year 1 | |||||

| July | 1 | Cash | 206,890 | ||

| Loss on Sale of Investments | 18,155 | ||||

| Investments–Company C Stock | 225,045 | ||||

| (To record sale of shares) | |||||

Table (3)

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Loss on Sale of Investments is a loss or expense account. Since losses decrease equity, equity value is decreased, and a decrease in equity is debited.

- Investments–Company C Stock is an asset account. Since stock investments are sold, asset value decreased, and a decrease in asset is credited.

Working Notes:

Calculate the realized gain (loss) on sale of stock.

Step 1: Compute cash received from sale proceeds.

Step 2: Compute cost of stock investment sold.

Step 3: Compute realized gain (loss) on sale of stock.

Note: Refer to Steps 1 and 2 for value and computation of cash received and cost of stock investment sold.

Prepare journal entry for the dividend received from Company C for 3,000 shares.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| Year 1 | |||||

| July | 31 | Cash | 1,500 | ||

| Dividend Revenue | 1,500 | ||||

| (To record receipt of dividend revenue) | |||||

Table (4)

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Dividend Revenue is a revenue account. Since revenues increase equity, equity value is increased, and an increase in equity is credited.

Working Notes:

Compute amount of dividend received on Company C’s stock.

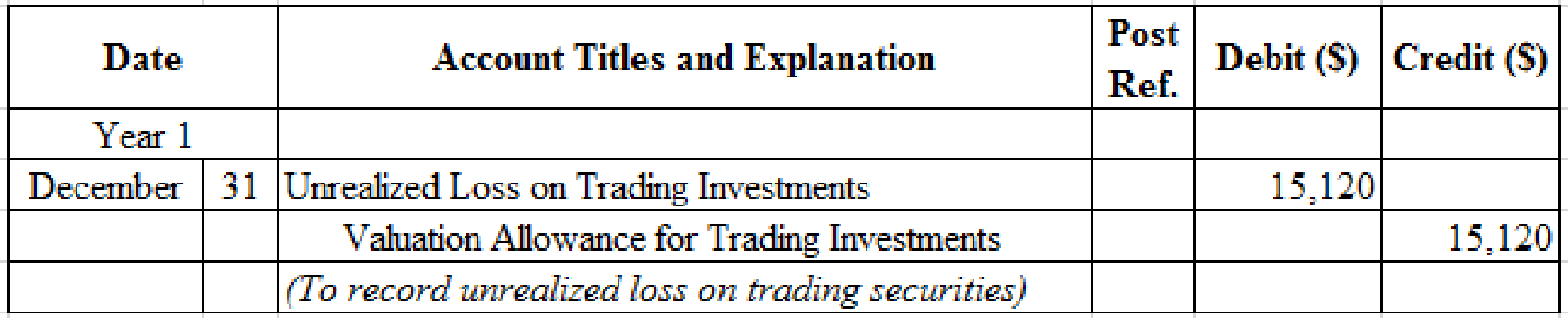

Prepare adjusting entry for valuation of trading securities transaction.

Table (5)

- Unrealized Loss on Trading Investments is an adjustment account used to report gain or loss on adjusting cost of investment at fair market value. Since loss has occurred and losses reduce stockholders’ equity value, and a decrease in stockholders’ equity value is debited.

- Valuation Allowance for Trading Investments is a contra-asset account. The account is credited because the market price was decreased (loss) to $276,120 from the cost of $261,000.

Working Notes:

Compute the unrealized gain (loss) as on December 31.

Step 1: Compute the fair value of the portfolio of the trading investment.

| Security | Number of Shares | Fair Market Value | = | Fair Market Value of Investment | |

| Company C | 3,000 shares | $47 | = | $141,000 | |

| Company H | 3,000 shares | 40 | = | 120,000 | |

| Total | $261,000 | ||||

Table (6)

Step 2: Compute the cost per share of Company C.

Step 3: Compute the cost per share of Company H.

Step 4: Compute the cost of the portfolio of the trading investment, as on December 31.

| Security | Number of Shares | Cost per Share | = | Cost of Investment | |

| Company C | 3,000 shares | $50.01 | = | $150,030 | |

| Company H | 3,000 shares | 42.03 | = | 126,090 | |

| Total | $276,120 | ||||

Table (7)

Note: Refer to Steps 3 and 4 for cost per share of Company C and Company H.

Step 5: Compute the unrealized gain (loss) as on December 31.

| Details | Amount ($) |

| Trading investments at fair value, December 31 (From Table-6) | $261,000 |

| Less: Trading investments at cost, December 31 (From Table-7) | (276,120) |

| Unrealized loss on trading investments | $(15,120) |

Table (8)

Prepare journal entry for the purchase of 5,000 shares of Company F, at $25 per share, and a brokerage commission of $100.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| Year 2 | |||||

| April | 1 | Investments–Company F Stock | 125,100 | ||

| Cash | 125,100 | ||||

| (To record purchase of shares for cash) | |||||

Table (9)

- Investments–Company F Stock is an asset account. Since stock investments are purchased, asset value increased, and an increase in asset is debited.

- Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Working Notes:

Compute amount of cash paid to purchase Company F’s stock.

Prepare journal entry for the dividend received from Company C for 3,000 shares.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| Year 2 | |||||

| July | 31 | Cash | 1,560 | ||

| Dividend Revenue | 1,560 | ||||

| (To record receipt of dividend revenue) | |||||

Table (10)

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Dividend Revenue is a revenue account. Since revenues increase equity, equity value is increased, and an increase in equity is credited.

Working Notes:

Compute amount of dividend received on Company C’s stock.

Prepare journal entry for sale of 1,000 shares of Company F at $28, with a brokerage of $110.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| Year 2 | |||||

| October | 14 | Cash | 27,890 | ||

| Gain on Sale of Investments | 2,870 | ||||

| Investments–Company F Stock | 25,020 | ||||

| (To record sale of shares) | |||||

Table (11)

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Gain on Sale of Investments is a revenue account. Since revenues increase equity, equity value is increased, and an increase in equity is credited.

- Investments–Corporation E Stock is an asset account. Since stock investments are sold, asset value decreased, and a decrease in asset is credited.

Working Notes:

Calculate the realized gain (loss) on sale of stock.

Step 1: Compute cash received from sale proceeds.

Step 2: Compute cost of stock investment sold.

Step 3: Compute realized gain (loss) on sale of stock.

Note: Refer to Steps 1 and 2 for value and computation of cash received and cost of stock investment sold.

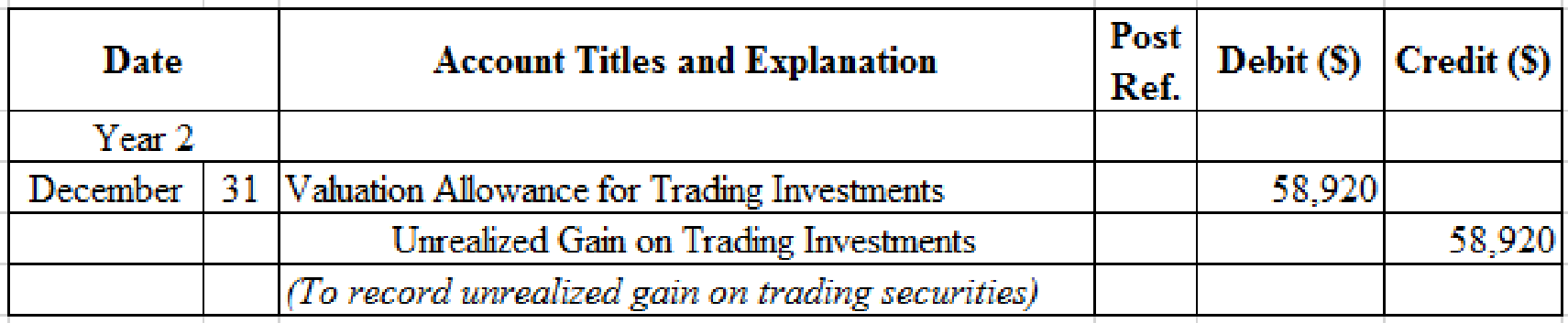

Prepare adjusting entry for valuation of trading securities transaction.

Table (12)

- Valuation Allowance for Trading Investments is a contra-asset account. The account is debited because the market price was increased (gain).

- Unrealized Gain on Trading Investments is an adjustment account used to report gain or loss on adjusting cost of investment at fair market value. Since gain has occurred and gains increase stockholders’ equity value, and an increase in stockholders’ equity value is credited.

Working Notes:

Compute the unrealized gain (loss) as on December 31.

| Details | Amount ($) |

| Unrealized gain as on December 31, Year 2 | $43,800 |

| Less: Unrealized loss as on December 31, Year 1 (From Table-8) | (15,120) |

| Unrealized loss on trading investments | $58,920 |

Table (13)

(2)

Indicate the presentation of trading investments on the current assets section of the balance sheet.

Explanation of Solution

Balance sheet presentation:

| Company R | ||

| Balance Sheet (Partial) | ||

| December 31, Year 2 | ||

| Assets | ||

| Current assets: | ||

| Trading investments (at cost) | $376,200 | |

| Add valuation allowance for trading investments | 43,800 | |

| Trading investments (at fair value) | $420,000 | |

Table (14)

(3)

Discuss the reporting of trading investments on the financial statements.

Explanation of Solution

Unrealized gain or loss is the result of change in trading investments cost and fair values, and reported as Other Revenues (Losses) on the income statement. The unrealized gain will be added to the net income and unrealized loss will be deducted from the net income. In the Year 1, Company R would report $15,120 of unrealized loss as Other Losses on the income statement. In the Year 2, Company R would report $58,920 of unrealized gain as Other Income on the income statement.

Want to see more full solutions like this?

Chapter 15 Solutions

Financial Accounting

- Soto Industries Inc. is an athletic footware company that began operations on January 1, Year 1. The following transactions relate to debt investments acquired by Soto Industries Inc., which has a fiscal year ending on December 31: Instructions 1. Journalize the entries to record these transactions. 2. If the bond portfolio is classified as available for sale, what impact would this have on financial statement disclosure?arrow_forwardRekya Mart Inc. is a general merchandise retail company that began operations on January 1, Year 1. The following transactions relate to debt investments acquired by Rekya Mart Inc., which has a fiscal year ending on December 31: Instructions 1. Journalize the entries to record these transactions. 2. If the bond portfolio is classified as available for sale, what impact would this have on financial statement disclosure?arrow_forwardForte Inc. produces and sells theater set designs and costumes. The company began operations on January 1, Year 1. The following transactions relate to securities acquired by Forte Inc., which has a fiscal year ending on December 31: Instructions 1. Journalize the entries to record these transactions. 2. Prepare the investment-related asset and stockholders equity balance sheet presentation for Forte Inc. on December 31, Year 2, assuming that the Retained Earnings balance on December 31, Year 2, is 389,000.arrow_forward

- The following equity investment transactions were completed by Romero Company during a recent year: Journalize the entries for these transactions.arrow_forwardGlacier Products Inc. is a wholesaler of rock climbing gear. The company began operations on January 1, Year 1. The following transactions relate to securities acquired by Glacier Products Inc., which has a fiscal year ending on December 31: Instructions 1. Journalize the entries to record the preceding transactions. 2. Prepare the investment-related asset and stockholders equity balance sheet presentation for Glacier Products Inc. on December 31, Year 2, assuming that the Retained Earnings balance on December 31, Year 2, is 700,000.arrow_forwardYou were assigned to perform audit procedures on the investments account of Classic Corporation for 2020, yourfirst-time audit of the client. The current asset portion of Classic Corporation’s statement of financial positionshows the following information as of December 31, 2019: Current Assets Note As of December 31, 2019 Cash and cash equivalents 5, 14 P 3,985,000 Receivables, net 6, 14 7,742,000 Inventories 7 15,859,000 Short-term investments 8, 14 3,280,000 Other current assets 10 352,000 Total current assets P 31,218,000 Note 8 on investments described the investments as equity securities held primarily for being traded to takeadvantage of price fluctuations in the market. The following information shows the breakdown of the investmentaccount per client’s subsidiary records: Held for Trading Securities: Securities No. of Shares Market Price Amount SMC Ordinary 5,000…arrow_forward

- At December 31, 2021, Hull-Meyers Corp. had the following investments that were purchased during 2021, its first year of operations: Trading Securities: Security A Security B Totals Securities Available-for-Sale: Security C Security D Totals Securities to Be Held-to-Maturity: Security E Security F Totals Trading Securities Security A Security B Securities Available-for-Sale Security C Security D Securities to be Held-to-Maturity Security E Security F Totals Amortized cost Reported on Balance Sheet as: Current assets $ 905,000 110,000 $1,015,000 Noncurrent assets $ 705,000 905,000 $1,610,000 $ 495,000 620,000 $1,115,000 No investments were sold during 2021. All securities except Security D and Security F are considered short-term investments. None of the fair value changes is considered permanent. Required: Complete the following table. (Amounts to be deducted should be indicated with a minus sign.) Fair Value $915,500 104,900 $1,020,400 $ 784,500 920, 200 $1,704,700 Net Income (I/S) $…arrow_forwardGard Company completes the following transactions related to its short-term debt investments. May 8 Purchased FedEx notes as a short-term investment in available-for-sale securities for $12,975. Sep. 2 Sold part of its investment in FedEx notes for $4,475, which had cost $4,325. Oct. 2 Purchased Ajay bonds for $25,600 as a short-term investment in available-for-sale securities.arrow_forwardInstructions: (Assume all transactions during the year were for cash.) a. Prepare the journal entry to record the sale of the available-for-sale debt securities in 2020. b. Prepare the journal entry to record the Unrealized Holding Gain or Loss for 2020. c. Prepare a statement of comprehensive income for 2020. d. Prepare a balance sheet as of December 31, 2020arrow_forward

- During the current year, Reed Consulting acquired long-term available-for-sale debt securities on July 1 at a $76,000 cost. At its December 31 year-end, these securities had a fair value of $63,400. This is the first and only time the company purchased such securities. 1. Prepare the July 1 entry to record the purchase of these debt securities. 2. Prepare the year-end adjusting entry related to these securities. View transaction list Journal entry worksheet 1 2 Record purchase of available-for-sale securities. Note: Enter debits before credits. Date July 01 Record entry General Journal Clear entry Debit Credit View general journalarrow_forwardParkman Sporting Goods is preparing its annual report for its 2021 fiscal year. The company’s controller has asked for your help in determining how best to disclose information about the following items:1. A related-party transaction.2. Depreciation method.3. Allowance for uncollectible accounts.4. Composition of investments.5. Composition of long-term debt.6. Inventory costing method.7. Number of shares of common stock authorized, issued, and outstanding.8. Employee benefit plans.Required:Indicate whether the above items should be disclosed (A) in the summary of significant accounting policies note, (B) in a separate disclosure note, or (C) on the face of the balance sheet.arrow_forwardKitty Company began operations in the current year and acquired short-term debt investments in trading securities. The year-end cost and fair values for its portfolio of these debt investments follow. Trading Securities Tesla Bonds Nike Bonds Ford Bonds (1) After the fair value adjustment is made, prepare the assets section of Kitty Company's December 31 classified balance sheet. (2) In which income statement section is the unrealized gain (or loss) on the portfolio of trading securities reported? Required 1 Cost $ 12,900 21, 200 5,300 Complete this question by entering your answers in the tabs below. Required 2 Fair Value $ 9,675 22,260 4,240 KITTY COMPANY Assets Section of Balance Sheet December 31 Assets After the fair value adjustment is made, prepare the assets section of Kitty Company's December 31 classified balance sheet. Note: Amounts to be deducted should be indicated with a minus sign.arrow_forward

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning