Concept explainers

Videos

Nature of transactions

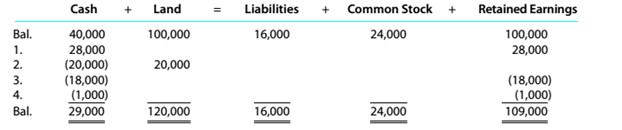

Cheryl Alder operates her own catering service. Summary financial data for March are presented in the following equation form. Each line, designated by a number, indicates the effect of a transaction on the

a. Describe each transaction.

h. What is the net decrease in cash during the month?

c. What is the net increase in retained earnings during the month?

d. What is the net income for the month?

e. How much of the net income for the month was retained in the business?

f. What are the net cash flows from operating activities?

g. ‘1iat arc the net cash flows fn)m investing activities?

h. What are the net cash flows from financing activities?

(a)

Balance sheet:

It is a financial statement that records the assets, liabilities and stockholder's equity of the company at a point in time. The balance sheet also known as statement of financial condition is expressed in the accounting equation as:

The balance sheet is prepared using accounting equation in vertical form. Also, the balance on assets side must be equal to sum of balances of liabilities and stockholder's equity

The effect of each transaction in balance sheet of person A during the given period.

Answer to Problem 2.11E

The effect of each transaction is mentioned below:

- Here, there is an increase in cash by $28000 along with an increase in retained earnings by$28000 which means that this increase is due to payment received from customers or fees earned.

- In this transaction, there is an increase in land under assets by $20000 along with a decrease in cash under assets by $20000 which means that land is purchased for which cash decreased during the given period.

- Here, there is decrease in cash under assets as well as decrease in retained earnings under stockholders' equity by $18000 which means that operating expenses have been paid during the given period.

- In this transaction, there is decrease in cash under assets as well as decrease in retained earnings under stockholders' equity by $1000 which means that dividends have been paid during the given period.

Explanation of Solution

The effect of each transaction is explained below:

- When there is an increase in cash, it means that the person A has received cash of $28000 as fees earned it will increase assets in the form of cash and increase retained earnings under stockholder's equity by $28000. The effect of this transaction on statement of cash flows will be an increase in cash flow from operating activities by $28000.

- When there is decrease in cash along with an increase in land value of same amount it means that the person A has purchased land of $20000, which will be recorded in balance sheet as a deduction from cash under assets and added to land as an asset. In the statement of cash flows it will be recorded as a deduction under cash flow from investing activities.

- When there is decrease in cash and retained earnings of same amount it means that person A has paid operating expenses of $18000 which will reduce balance sheet balance under assets since cash is paid and retained earnings will also reduce. In the statement of cash flows, it will be recorded as a deduction under cash flow from operating expenses and in income statement it will be treated as an expense.

- When there is decrease in cash and retained earnings of same amount it means person A paid dividends of $1000, which will be reduced from assets under cash for dividends paid and from retained earnings under stockholder's equity with $1000. Also, it will be recorded in the statement of cash flows under cash flow from financing activities as a deduction of $1000.

(b)

Statement of cash flows:

It is a financial statement that provides details of changes in cash that is cash generated or used during a period. The analysis of this statement is divided into three sections:

- Operating activities- It is used to assess the cash flows from operating activities of the business.

- Investing activities- It is used to report the cash flows from purchase and sale of long-term investments.

- Financing activities- It is used to show changes in cash from borrowings and contributed equity capital of the company.

The net decrease in cash during the month.

Answer to Problem 2.11E

The statement of cash flows shows that there is a net decrease in cash during the month which is $11000

Explanation of Solution

Computation of Statement of cash flows of company P for the year ended 31, 20Y8:

(c)

Retained Earnings:

It is related to net income and represents accumulated profits after paying out dividends to stockholders of the company. It is calculated as:

To compute:

Net increase in retained earnings during the month.

Answer to Problem 2.11E

The net increase in retained earnings during the month is $9000

Explanation of Solution

Computation of net increase in retained earnings:

Computation of net income with income statement for the month:

(d)

Income statement:

This statement shows the financial performance of the company over a specific time-period. It is used to measure the profitability of the company by recording revenues and expenses during a period.

To prepare:

The income statement of company A for the month.

Answer to Problem 2.11E

The income statement of company A shows net income of $10000 for the month.

Explanation of Solution

Computation of income statement of company A for the month:

(e)

Retained Earnings:

It is related to net income and represents accumulated profits after paying out dividends to stockholders of the company. It is calculated as:

To compute:

Net income retained for the month by person A.

Answer to Problem 2.11E

The net income retained for the month in the business is $9000.

Explanation of Solution

Computation of retained earnings for the month:

Computation of net income with income statement:

(f)

Statement of cash flows:

It is a financial statement that provides details of changes in cash that is cash generated or used during a period. The analysis of this statement is divided into three sections:

- Operating activities- It is used to assess the cash flows from operating activities of the business.

- Investing activities- It is used to report the cash flows from purchase and sale of long-term investments.

- Financing activities- It is used to show changes in cash from borrowings and contributed equity capital of the company.

To compute:

Net cash from operating activities for the month.

Answer to Problem 2.11E

The net cash flows from operating activities of company A for the month is $10000.

Explanation of Solution

Computation of net cash flows from operating activities of company A for the month:

(g)

Statement of cash flows:

It is a financial statement that provides details of changes in cash that is cash generated or used during a period. The analysis of this statement is divided into three sections:

- Operating activities- It is used to assess the cash flows from operating activities of the business.

- Investing activities- It is used to report the cash flows from purchase and sale of long-term investments.

- Financing activities- It is used to show changes in cash from borrowings and contributed equity capital of the company.

To compute:

Cash flow from investing activities for the month.

Answer to Problem 2.11E

The cash flow from investing activities for the month is $20000.

Explanation of Solution

Computation of cash flow from investing activities for the month:

(h)

Statement of cash flows:

It is a financial statement that provides details of changes in cash that is cash generated or used during a period. The analysis of this statement is divided into three sections:

- Operating activities- It is used to assess the cash flows from operating activities of the business.

- Investing activities- It is used to report the cash flows from purchase and sale of long-term investments.

- Financing activities- It is used to show changes in cash from borrowings and contributed equity capital of the company.

To compute:

Cash flow from financing activities for the month.

Answer to Problem 2.11E

The net cash flow from financing activities for the month is $1000.

Explanation of Solution

Computation of cash flows from financing activities for the month:

Want to see more full solutions like this?

Chapter 2 Solutions

Survey of Accounting (Accounting I)

Additional Business Textbook Solutions

Auditing And Assurance Services

INTERMEDIATE ACCOUNTING

Financial Accounting (12th Edition) (What's New in Accounting)

Financial Accounting (11th Edition)

Fundamentals of Financial Accounting

Advanced Financial Accounting

- "Choose from the following list of terms and phrases to best complete the statements below. Fiscal year Timeliness Accrual basis accounting Annual financial statements Cash basis accounting Time period assumption 1. presumes that an organization's activities can be divided into specific time periods. 2.Financial reports covering a one-year period are known as 3.A(n) consists of any 12 consecutive months. 4. records revenues when services are provided and records expenses when incurred. 5. The value of information is often linked to itsarrow_forwardNature of transactionsTeri West operates her own catering service. Summary financial data forJuly are presented in equation form as follows. Each line designated by anumber indicates the effect of a transaction on the equation. Eachincrease and decrease in owner's equity, except transaction (5), affectsnet income. a. Describe each transaction. b. What is the amount of the net increase in cash during the month? c. What is the amount of the net increase in owner's equity during themonth? d. What is the amount of the net income for the month? e. How much of the net income for the month was retained in thebusiness?arrow_forwardSuppose your company sells services for $325 cash this month. Your company also pays $100 insalaries and wages, which includes $15 that was payable at the end of the previous month and $85 forsalaries and wages of this month.Required:1. Show the journal entries to record these transactions.2. Calculate the amount that should be reported as net cash flow from operating activities.3. Calculate the amount that should be reported as net income.4. Show how the indirect method would convert net income (requirement 3) to net cash flowfrom operating activities (requirement 2).5. What general rule about converting net income to operating cash flows is revealed by youranswer to requirement 4?arrow_forward

- Using the accrual basis, in which month should revenue be recorded? OA. In the month that goods are ordered by the customer B. In the month that goods are shipped to the customer C. In the month that the invoice is mailed to the customer D. In the month that cash is collected from the customerarrow_forwardAt Homeland Arts, gross sales for the month included: Sales on account (1/10, r/30) Credit card sales (4 % credit card fee) $200,000 $160,000 Date (a) Requirement 1. Journalize the sales on account, the credit card sales, and the cash payments on account received during the month. (Use the gross method to record the sales transactions Record debits first, then credits Exclude explanations from any joumal entries.) First, record the sales on account Journal Entry Accounts Debit Half of the sales on account were paid within the discount period, the other accounts were paid in full by the end of the month Read the requirements Creditarrow_forwardAssessing Financial Statement Effects of TransactionsDeFond Services, a firm providing art services for advertisers, began business on June 1. The following accounts are needed to record the transactions for June: Cash; Accounts Receivable; Supplies; Office Equipment; Accounts Payable; Common Stock; Dividends; Service Fees Earned; Rent Expense; Utilities Expense; and Wages Expense. Record the following transactions for June using the financial statement effects template. (Record each transaction in the order it appears.) June 1 M. DeFond invested $12,000 cash to begin the business in exchange for common stock. 2 Paid $950 cash for June rent.Hint: Record rent expense on June 2. 3 Purchased $6,400 of office equipment on credit. 6 Purchased $3,800 of art materials and other supplies; the company paid $1,800 cash with the remainder due within 30 days. 11 Billed clients $4,700 for services rendered. 17 Collected $3,250 cash from clients on their accounts billed on…arrow_forward

- Question Topic– Analysing business transactions. The following table contains several business transactions for the current month. Required: Identify the names of which accounts are affected, how they are affected (+/-, increase or decrease), and the element of the financial statement of these accounts (A, L, OE, R, E).arrow_forwardWhich of the following transactions causes an increase in total assets? a. Pay employee salaries for the current month. b. Pay dividends to stockholders. c. Issue common stock in exchange for cash. d. Purchase office equipment for cash.arrow_forwardGumbo Company had the following transactions during the month of December. What was the December 1 cash balance?arrow_forward

- Which of the following breaks down company financial information into specific time spans, and can cover a month, quarter, half-year, or full year? A. accounting period B. yearly period C. monthly period D. fiscal periodarrow_forwardFINANCIAL RATIOS Use the work sheet and financial statements prepared in Problem 15-8B. All sales are credit sales. The Accounts Receivable balance on January 1 was 38,200. REQUIRED Prepare the following financial ratios: (a)Working capital (b)Current ratio (c)Quick ratio (d)Return on owners equity (e)Accounts receivable turnover and the average number of days required to collect receivables (f)Inventory turnover and the average number of days required to sell inventoryarrow_forwardThe transactions completed by AM Express Company during March, the first month of the fiscal year, were as follows: Instructions 1. Enter the following account balances in the general ledger as of March 1: 2. Journalize the transactions for March, using the following journals similar to those illustrated in this chapter: single-column revenue journal (p. 35), cash receipts journal (p. 31), purchases journal (p. 37, with columns for Accounts Payable, Maintenance Supplies, Office Supplies, and Other Accounts), cash payments journal (p. 34), and twocolumn general journal (p. 1). Assume that the daily postings to the individual accounts in the accounts payable subsidiary ledger and the accounts receivable subsidiary ledger have been made. 3. Post the appropriate individual entries to the general ledger. 4. Total each of the columns of the special journals and post the appropriate totals to the general ledger; insert the account balances. 5. Prepare a trial balance.arrow_forward

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning

College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning