Concept explainers

Videos

Problem 2-62B Comprehensive Problem

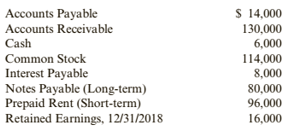

Mulberry Services sells electronic data processing services to firms too Email to own their own computing equipment. Mulberry had the following amounts and amount balances as of January 1, 2019:

During 2019, the following transactions occurred (the events described below are aggregations of many individual events):

- During 2019, Mulberry sold $690,000 of computing services, all on credit.

- Mulberry collected $570,000 from the credit sales in Transaction a and an additional $129,000 from the accounts receivable outstanding at the beginning of the year.

- Mulberry paid the interest payable of $8,000.

- A Wages of $379,000 were paid in cash.

- Repairs and maintenance of $9,000 were incurred and paid.

- The prepaid rent at the beginning of the year was used in 2019. In addition, $28,000 of computer rental costs were incurred and paid. There is no prepaid rent or rent payable at year-end.

- Mulberry purchased computer paper for $13,000 cash in late December. None of the paper was used by year-end.

- Advertising expense of $26,000 was incurred and paid.

- Income tax of $10,300 was incurred and paid in 2019.

- Interest of $5,000 was paid on the long-term loan.

(Continued)

Required:

- Establish a T-account for the accounts listed above and enter the beginning balances. Use a chart of accounts to order the T-accounts.

- Analyze each transaction; Journalize as appropriate. (Note: Ignore the date because these events are aggregations of individual events.)

Post your journal entries to the T-accounts. Add additional T-accounts when needed.- Use the ending balances in the T-accounts to prepare a

trial balance .

T-Accounts:

T-accounts as its name derived from shape of the account, is representation of business transaction in their respective account. It helps in organizing and analyzing the transaction according to their similar nature of account.

Requirement 1

Prepare:

Prepare ledger accounts and enter the beginning balances.

Answer to Problem 62APSA

Cash

| Bal. $16,300 | |

Accounts Receivable

| Bal. $384,000 | |

Accounts Payable

| Bal. $11,900 | |

Interest Payable

| Bal. $11,200 | |

Rent Payable

| Bal. $10,000 | |

Insurance Payable

| Bal. $1,000 | |

Notes Payable

| Bal. $100,000 | |

Common Stock

| Bal. $165,000 | |

Retained Earnings

| Bal. $101,200 | |

Explanation of Solution

| Nature | Accounts Name | Normal Balance | Debit | Credit |

| Asset | Cash | Debit | Increase | Decrease |

| Accounts Receivable | Debit | Increase | Decrease | |

| Liabilities | Accounts Payable | Credit | Decrease | Increase |

| Interest Payable | Credit | Decrease | Increase | |

| Rent Payable | Credit | Decrease | Increase | |

| Insurance Payable | Credit | Decrease | Increase | |

| Notes Payable | Credit | Decrease | Increase | |

| Equity | Common Stock | Credit | Decrease | Increase |

| Retained Earnings | Credit | Decrease | Increase |

Journal Entries:

Journal entries are medium of recording business transactions. A business enterprise must record all the business transaction to evaluate net income or loss and analyze the financial performance of a company during a specified accounting period.

Requirement 2

To Prepare:

Prepare journal entries for the transaction during 2019.

Answer to Problem 62APSA

| Events | Accounts and Explanation | Debit | Credit |

| a. | Accounts Receivable | $994,000 | |

| Service Revenue | $994,000 | ||

| b. | Cash | 384,000 | |

| Accounts Receivable | 384,000 | ||

| c. | Cash | 983,000 | |

| Accounts Receivable | 983,000 | ||

| d. | Rent Payable | 10,000 | |

| Rent Expense | 48,000 | ||

| Cash | 58,000 | ||

| e. | Insurance Payable | 1,000 | |

| Insurance Expense | 4,000 | ||

| Cash | 5,000 | ||

| f. | Utilities Expense | 56,000 | |

| Cash | 56,000 | ||

| g. | Salaries Expense | 702,000 | |

| Cash | 702,000 | ||

| h. | Interest Payable | 11,200 | |

| Interest Expense | 11,000 | ||

| Cash | 22,200 | ||

| i. | Income Tax Expense | 19,700 | |

| Cash | 19,700 |

Explanation of Solution

| Accounting Equation | |||||

| Asset = Liabilities +Stockholders’ Equity | |||||

| a. | Increase (Accounts Receivable) | Increase (Service revenue) | |||

| b. | Increase (Cash) | ||||

| Decrease (Accounts Receivable) | |||||

| c. | Increase (Cash) | ||||

| Decrease (Accounts Receivable) | |||||

| d. | Decrease (Cash) | Decrease (Rent Payable) | Decrease (Rent Expense) | ||

| e. | Decrease (Cash) | Decrease (Insurance Payable) | Decrease (Insurance Expense) | ||

| f. | Decrease (Cash) | Decrease (Utilities Expense) | |||

| g. | Decrease (Cash) | Decrease (Salaries Expense) | |||

| h. | Decrease (Cash) | Decrease (Interest Payable) | Decrease (Interest Expense) | ||

| i. | Decrease (Cash) | Decrease (Income Tax Expense) | |||

Introduction:

T-accounts as its name derived from shape of the account, is representation of business transaction in their respective account. It helps in organizing and analyzing the transaction according to their similar nature of account.

Requirement 3

Prepare:

Posting the journal entries to T-accounts.

Answer to Problem 62APSA

| Accounts | Balance |

| Cash | $520,400 |

| Accounts Receivable | 11,000 |

| Accounts Payable | 11,900 |

| Interest Payable | 0 |

| Rent Payable | 0 |

| Insurance Payable | 0 |

| Notes Payable | 100,000 |

| Common Stock | 165,000 |

| Retained Earnings | 101,200 |

| Service Revenue | 994,000 |

| Rent Expense | 48,000 |

| Insurance Expense | 4,000 |

| Utilities Expense | 56,000 |

| Salaries Expense | 702,000 |

| Interest Expense | 11,000 |

| Income Tax Expense | 19,700 |

Explanation of Solution

Cash

| Bal. $16,300 (b) 384,000 (c) 983,000 | (d) $58,000 (e) 5,000 (f) 56,000 (g) 702,000 (h) 22,200 (i) 19,700 |

| Bal. 520,400 |

Accounts Receivable

| Bal. $384,000 (a) 994,000 | (b) $384,000 (c) 983,000 |

| Bal. 11,000 |

Accounts Payable

| Bal. $11,900 | |

| Bal. 11,900 |

Interest Payable

| (h) 11,200 | Bal. $11,200 |

| Bal. 0 |

Rent Payable

| (d) 10,000 | Bal. $10,000 |

| Bal. 0 |

Insurance Payable

| (e)1,000 | Bal. $1,000 |

| Bal. 0 |

Notes Payable

| Bal. $100,000 | |

| Bal. 100,000 |

Common Stock

| Bal. $165,000 | |

| Bal. 165,000 |

Retained Earnings

| Bal. $101,200 | |

| Bal. 101,200 |

Service Revenue

| Bal. $0 (a) 994,000 | |

| Bal. 994,000 |

Rent Expense

| Bal. $0 (d) 48,000 | |

| Bal. 48,000 |

Insurance Expense

| Bal. $0 (e)4,000 | |

| Bal. 4,000 |

Utilities Expense

| Bal. $0 (f) 56,000 | |

| Bal. 56,000 |

Salaries Expense

| Bal. $0 (g) 702,000 | |

| Bal. 702,000 |

Interest Expense

| Bal. $0 (h)11,000 | |

| Bal. 11,000 |

Income Taxes Expense

| Bal. $0 (i) 19,700 | |

| Bal. 19,700 |

Trial Balance:

A financial statement which integrates all the balance of ledger accounts is termed as a trial balance. The total balance of debit and credit in trial balance should be equal at end of an accounting period.

Requirement 4

Prepare:

Prepare the trial balance as of December 31, 2019.

Answer to Problem 62APSA

The total balance of the trial balance for the year ending December 31, 2019 is $1,372,100.

Explanation of Solution

| Western Sound StudiosTrial Balance December 31, 2019 | |||

| Accounts | Debit | Credit | |

| Cash | $520,400 | ||

| Accounts Receivable | 11,000 | ||

| Accounts Payable | $11,900 | ||

| Notes Payable | 100,000 | ||

| Common Stock | 165,000 | ||

| Retained Earnings | 101,200 | ||

| Service Revenue | 994,000 | ||

| Rent Expense | 48,000 | ||

| Insurance Expense | 4,000 | ||

| Utilities Expense | 56,000 | ||

| Salaries Expense | 702,000 | ||

| Interest Expense | 11,000 | ||

| Income Tax Expense | 19,700 | ||

| Total | $1,372,100 | $1,372,100 | |

Want to see more full solutions like this?

Chapter 2 Solutions

Cornerstones of Financial Accounting

- Problem 2-24 (IFRS) Alyanna Company operates a customer loyalty program. The entity grants program members loyalty points when they spend a specified amount on purchases. Program members can redeem the points for further purchases. The points have no expiry date. During 2022, the customer earned 60,000 points. Management expects that 100% of these points will be redeemed. The stand-alone selling price of each loyalty point is estimated at P20. The sales during 2022 amounted to P6,800,000 based on stand-alone selling price. On December 31, 2022, 28,800 points have been redeemed in exchange for purchases. In 2023, the management revised expectations and now expects 90% of the points to be redeemed. In 2023, the entity redeemed 9,000 points. 1. What amount of the transaction price should be allocated to the points? a. 1,800,000 b. 1,200,000 c. 1,020,000 d. 0 2. What amount should be reported as revenue earned from loyalty points for 2022? a. 576,000 b. 489,600 c. 510,000 d. 0 3. What…arrow_forwardProblem 2-5 (IFRS) Erika Company operates a customer loyalty program. The entity grants loyalty points for goods purchased. The loyalty points can be used by the customers in exchange for the goods of the entity. The points have no expiry date. During 2020, the entity issued 50,000 award credits and expects that 80% of these award credits shall be redeemed. The stand-alone selling price of the award credits granted is reliably measured at P1,000,000. In 2020, the entity sold goods to customers for a total consideration of P7,000,000 based on stand-alone selling price. The award credits redeemed and the total award credits expected to be redeemed each year are as follows: Redeemed Expected to be redeemed 2020 15,000 80% 2021 7,950 85%…arrow_forwardMalachi Department Store starts its business on May 1, 2022 and completes the following transactions relating to its credit card sales during May: Total sales charged by customers are as follows: BPI P 600,000 RCBC 1,200,000 Eastwest 1,500,000 Deposits made by banks to charge the account of Malachi for credit card sales, net of 3% service charge. BPI P 407,400 RCBC 814,800 Eastwest 1,018,500. How much is the accounts receivable as of May 31, 2022?arrow_forward

- Notes Receivable Link Communications programs voicemail systems for businesses. For a recent project, they charged $135 000. The customer secured this amount by signing a note bearing 9% interest on February 1, 2019. Required: 1. Prepare the journal entry to record the sale on February 1, 2019. 2. Determine how much interest Link will receive if the note is repaid on December 1, 2019. 3. Prepare Links journal entry to record the cash received to pay off the note and interest on December 1, 2019.arrow_forwardMcKinney Co. estimates its uncollectible accounts as a percentage of credit sales. McKinney made credit sales of 1,500,000 in 2019. McKinney estimates 2.5% of its sales will be uncollectible. Prepare the journal entry to record bad debt expense for McKinney at the end of 2019.arrow_forwardWrite-Off of Uncollectible Accounts King Enterprises had 27 customers utilizing its financial planning services in 2019. Each customer paid King $25,000 for receiving Kings assistance. King estimates that 2% of its $675,000 credit sales in 2019 will be uncollectible. During 2020, King wrote off $2,700 related to services performed in 2019. Required: 1. Prepare the journal entry to record the defaulted balance. 2. Prepare the adjusting entry to record the bad debt expense for 2019.arrow_forward

- PROBLEM 1 (MODIFIED) Spring Corporation has the following account balances on December 31, 2020: Accounts receivable Php 400,000 Allowance for uncollectible accounts 8,400 Spring completed the following transactions in 2019: Net credit sales, Php 4,000,000. Collections on accounts, Php 3,870,000. Write-off of uncollectible accounts, Php 10,000. Recovery of accounts previously written-off, Php 2,000. Uncollectible accounts expense, 2/3 of 1% of net credit sales. REQUIRED: Journalize the foregoing transactions. Compute the balance of accounts receivable and allowance for uncollectible accounts at December 31, 2020. What amount of Accounts receivable, net would Spring report on its December 31, 2020 balance sheet? Assume that Spring uses the aging of accounts instead of the percent of sales method in estimating uncollectible accounts. Analysis indicates that Php 30,800 of outstanding accounts on December 31, 2020 may prove to…arrow_forwardPlease help to solve the whole question please this is 1 question with 3sub parts. InvisiGuard Ltd sells security doors. Majority of its sales are on credit except small amount of cash sales each year. The accounting records at 30 June 2019 reveal the following. Ignore GST. Credit sales (for the year of 2019) $2,100,000 Cash sales (for the year of 2019) 20,000 Credit sales returns and allowances (for the year of 2019) 80,000 Accounts receivable (balance at 30 June 2019) 593,000 Allowance for doubtful debts (credit balance at 30 June 2019) 2,800 The company’s yearly bad debts expense had been estimated at 2.5% of net credit sales revenue in the past. The management of InvisiGuard Ltd has decided to compare the current method with an ageing of accounts receivable method. The following analysis was obtained with respect to the accounts receivable. Balance % of estimated uncollectable Accounts not yet due $351,200 1 Accounts…arrow_forwardAging Method Spotted Singer Ltd. sells karaoke machines to businesses and consumers via the Internet. On December 31, 2021, Spotted Singer has an accounts receivable balance of $997,000 and a credit balance in its allowance for doubtful accounts of $24,000. During 2022, Spotted Singer had $2,500,000 of credit sales, collected $1,725,000 of accounts receivable, and had customer defaults of $45,000. At year-end, an aging analysis indicates that $28,000 of Spotted Singer's receivables will be uncollectible. Required: 1. Calculate Spotted Singer's balance in accounts receivable on December 31, 2022, prior to the adjustment. 2. Calculate Spotted Singer's balance in allowance for doubtful accounts on December 31, 2022, prior to the adjustment. 3. Prepare the necessary adjusting entry for 2022.arrow_forward

- Topic: Premium Liability Problem 2-20 William Company operates a customer loyalty program. The entity grants loyalty points for goods purchased. The loyalty points can be used by the customers in exchange for goods of the entity. The points have no expiry date. During 2020, the entity issued 100,000 award credits and expects that 80% of these award credits shall be redeemed. The total stand-alone selling price of the award credits granted is reliably measured at P2,000,000. In 2020, the entity sold goods to customers for a total consideration of P8,000,000 based on stand-alone selling price. The award credits redeemed and the total award credits expected to be redeemed each year are as follows Redeemed Expected to be redeemed 2020 30,000 80% 2021 15,000 90% Solve for the following: The revenue from points for 2020 The revenue from points for 2021arrow_forwardThe Yankee Corporation has recently begun to accept credit cards. On July 7, Year 1, Yankee made a credit card sale of $600. Assume that the credit card fee is recorded on the date of sale and that the credit card company charges a fee of 3% for handling a credit card transaction. Which of the following correctly shows the effects of the sale on July 7? Assets 600 A. B. 582 C. 582 D. 600 Multiple Choice O Balance Sheet Liabilities + 18 ΝΑ ΝΑ ΝΑ Option B Option D Option C Option A Stockholders' Equity 582 582 582 600 Revenue 582 600 600 600 Income Statement Expense = Net Income Statement of Cash Flows ΝΑ ΝΑ 18 582 0A 18 ΝΑ 582 582 582 600 ΝΑ ΝΑarrow_forwardProblem 20 On December 31, 2020, the accounts receivable control account of Eddie Company had a balance of PS,200,000. An analysis of the accounts receivable account showed the following: Subscription receivable due in 30 days Advance payments to creditors on purchase orders Advances to affiliated companies Interest receivable on bonds Trade accounts receivable - unassigned Customers' accounts reporting credit balances arising from sales returns Trade accounts receivable - assigned (Finance Company's equity in assigned accounts is P500,000) OMNA Trade installments receivable due 1-18 months, including unearned finance charge of P50,000 Trade accounts receivable from officers, due currently Trade accounts on which post-dated checks are held (no entries were made on receipt of checks) Accounts known to be worthless Total 2,200,000 400,000 1,000,000 400,000 2,000,000 ( 600,000) 1,500,000 850,000 150,000 200,000 100,000 8,200,000 The correct balance of trade accounts receivable on December…arrow_forward

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning