(a)

When the imported bananas are infected with a deadly virus what happens to the demand and supply curve.

Explanation of Solution

A report says that the bananas that have been imported are infected with a deadly virus, this will lead to the shift of consumers towards other fruits available in the market. Hence, the demand for the bananas will be less which will shift the demand curve towards left.

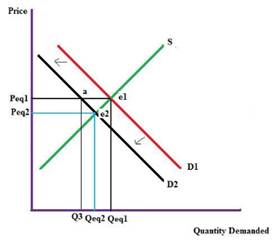

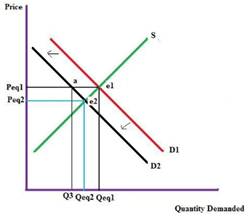

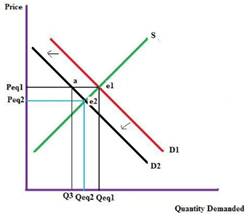

In the given graph, D1 is the initial demand curve, S is the initial supply curve, Peq1 is the initial

Demand and supply are the basic concepts in economics, and they can vary depending on various factors. Demand can be defined as how much quantity of the product or service is demanded or can be availed by a customer.

Whereas Supply how much quantity of products or services is available in the market.

(b)

When the consumers' income drops or decreases what happens to the demand and supply curve.

Explanation of Solution

A fall in consumer income will reduce the demand as his disposable income, so demand curve shifts down, which in turn reduces the price of the product. In the given graph, D1 is the initial demand curve S is the initial supply curve, Peq1 is the initial price and Qeq1 is the initial quantity. Due to change in income demand curve shifts to the left to D2. Price Peq1 is same but demand come down i.e. Q3 which lower than Qeq1 creating a surplus in the market. This in turn shifts the price to a new equilibrium point e2 and price changes to Peq2.and quantity become Qeq2.

Demand and supply are the basic concepts in economics, and they can vary depending on various factors. Demand can be defined as how much quantity of the product or service is demanded or can be availed by a customer.

Whereas Supply how much quantity of products or services is available in the market.

(c)

When the price of banana rises what happens to the demand and supply curve.

Explanation of Solution

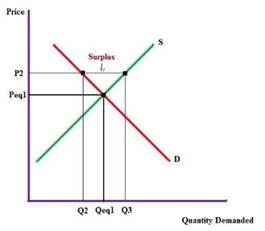

Demand is function of price and the quantity demanded. Hence, demand curve shifts when there is variation in the price and quantity demanded of the product. When price of banana rises quantity demanded will fall, which will create a surplus in the market.

Demand and supply are the basic concepts in economics, and they can vary depending on various factors. Demand can be defined as how much quantity of the product or service is demanded or can be availed by a customer.

Whereas Supply how much quantity of products or services is available in the market.

(d)

When the price of oranges falls what happens to the demand and supply curve.

Explanation of Solution

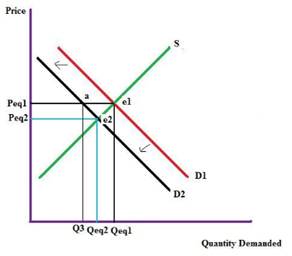

Oranges are a substitute to bananas. As the price of oranges fall, it causes a shift in the consumers preference. They start consuming more oranges than bananas. So, the quantity demanded for bananas fall and the demand curve of bananas shifts toward left reducing the price and consumption. Hence, at the new equilibrium point e2 price is reduced to Peq2 and quantity id reduced to Qeq2.

Demand and supply are the basic concepts in economics, and they can vary depending on various factors. Demand can be defined as how much quantity of the product or service is demanded or can be availed by a customer.

Whereas Supply how much quantity of products or services is available in the market.

(e)

When the consumers assume the price of bananas to fall in future what happens to the demand and supply curve.

Explanation of Solution

When consumers feel the price of bananas would fall in future, they would stop the consumption of bananas at the current price creating a surplus in the market. This would lead to reduction in price of the bananas. At the new point of

Demand and supply are the basic concepts in economics, and they can vary depending on various factors. Demand can be defined as how much quantity of the product or service is demanded or can be availed by a customer.

Whereas Supply how much quantity of products or services is available in the market.

Want to see more full solutions like this?

Chapter 3 Solutions

Microeconomics (MindTap Course List)

- Draw the Graph – Part 1 a. What is the difference between a "change in demand" and a "change in quantity demanded?" Graph your answer. b. For each of the following changes, determine whether there will be a change in quantity demanded or a change in demand. i. a change in the price of a related good ii. a change in tastes iii. a change in the number of buyers iv. a change in price v. a change in consumer expectations vi. a change in incomearrow_forwardSuppose we are analyzing the market for Sweet "Halwa" .What will happen to the equilibrium price and quantity of sweet if the price of sugar rises a little during Ramadan and Eid al-Fitr? Select one: a. Price will stay exactly the same and Quantity will decrease b. Price will increase and the Quantity will decrease c. Quantity will stay exactly the same and the price will increase d. None of the answers are correct e. Price will increase and the Quantity will increase O f. Price will decrease and the Quantity will decreasearrow_forwardExplain how each of the following events changes the demand for or supply of jeans. A. People's incomes increase. B. A new technology becomes available that reduces the time it takes to manufacture a pair of jeans. C. The price of the cloth (denim) used to make jeans falls. D. Jeans come back into fashion. E. The price of a pair of jeans falls. F. The wage rate paid to garment workers rises. G. Many jeans producers go out of business. H. The price of a denim skirt halves. A. Event G decreases supply and event H increases demand. B. Event B decreases supply and event G increases demand. O C. Event C increases demand and event D increases supply. D. Event E increases demand and event F decreases supply. OE. Event A increases demand and event B increases supply.arrow_forward

- Plot the supply curve and the demand curve for bicycles What is the equilibrium price of bicycles? What is the equilibrium quantity of bicycles? If the price of bicycles were €100, is there a surplus or a shortage? How many units of surplus or shortage are there? Will this cause the price to rise or fall ?arrow_forwardGraph the indicated hypothetical movements of demand and supply and state what then happens to both price and quantity. a. Increase in Supply (movement to the right), No change in Demand b. Decrease in Supply (movement to the left), No change in Demand c. Increase in Supply (movement to the right), Decrease in Demand (leftward shift) d. No change in Supply, Decrease in Demand (leftward shift) e. Decrease in Supply (movement to the left), Decrease in Demand (leftward shift)arrow_forward

Essentials of Economics (MindTap Course List)EconomicsISBN:9781337091992Author:N. Gregory MankiwPublisher:Cengage Learning

Essentials of Economics (MindTap Course List)EconomicsISBN:9781337091992Author:N. Gregory MankiwPublisher:Cengage Learning Brief Principles of Macroeconomics (MindTap Cours...EconomicsISBN:9781337091985Author:N. Gregory MankiwPublisher:Cengage Learning

Brief Principles of Macroeconomics (MindTap Cours...EconomicsISBN:9781337091985Author:N. Gregory MankiwPublisher:Cengage Learning Microeconomics: Private and Public Choice (MindTa...EconomicsISBN:9781305506893Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning

Microeconomics: Private and Public Choice (MindTa...EconomicsISBN:9781305506893Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning Macroeconomics: Private and Public Choice (MindTa...EconomicsISBN:9781305506756Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning

Macroeconomics: Private and Public Choice (MindTa...EconomicsISBN:9781305506756Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning Economics: Private and Public Choice (MindTap Cou...EconomicsISBN:9781305506725Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning

Economics: Private and Public Choice (MindTap Cou...EconomicsISBN:9781305506725Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning Economics (MindTap Course List)EconomicsISBN:9781337617383Author:Roger A. ArnoldPublisher:Cengage Learning

Economics (MindTap Course List)EconomicsISBN:9781337617383Author:Roger A. ArnoldPublisher:Cengage Learning