Videos

Randy Harris, controller, has been given the charge to implement an advanced cost management system. As part of this process, he needs to identify activity drivers for the activities of the firm. During the past four months, Randy has spent considerable effort identifying activities, their associated costs, and possible drivers for the activities’ costs.

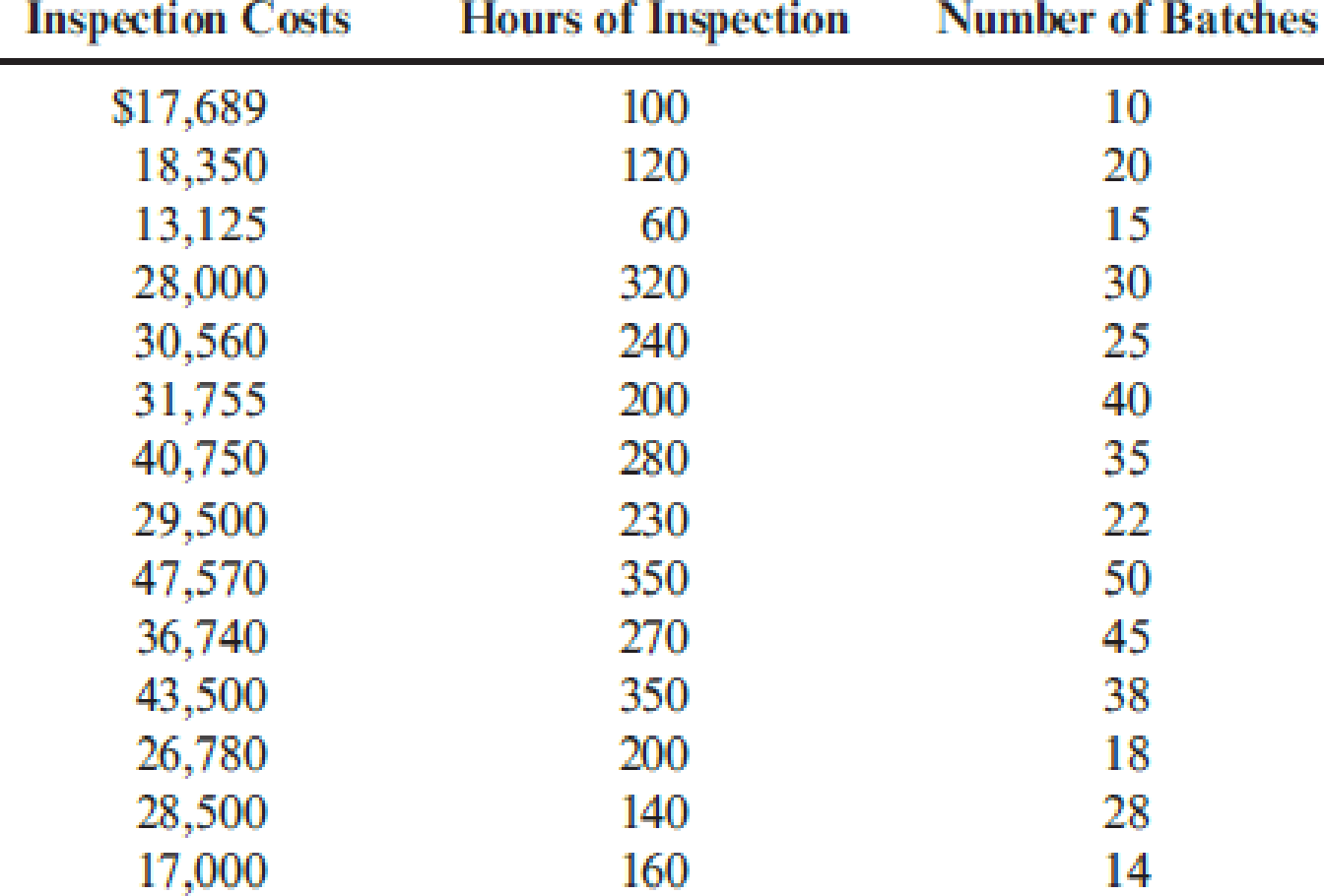

Initially, Randy made his selections based on his own judgment using his experience and input from employees who perform the activities. Later, he used regression analysis to confirm his judgment. Randy prefers to use one driver per activity, provided that an R2 of at least 80 percent can be produced. Otherwise, multiple drivers will be used, based on evidence provided by multiple regression analysis. For example, the activity of inspecting finished goods produced an R2 of less than 80 percent for any single activity driver. Randy believes, however, that a satisfactory cost formula can be developed using two activity drivers: the number of batches and the number of inspection hours. Data collected for a 14-month period are as follows:

Required:

- 1. Calculate the cost formula for inspection costs using the two drivers, inspection hours and number of batches. Are both activity drivers useful? What does the R2 indicate about the formula?

- 2. Using the formula developed in Requirement 1, calculate the inspection cost when 300 inspection hours are used and 30 batches are produced. Prepare a 90 percent confidence interval for this prediction.

Trending nowThis is a popular solution!

Chapter 3 Solutions

Cornerstones of Cost Management (Cornerstones Series)

- The owner of Nia Systems suspects her allocation of indirect costs could be giving misleading results, so she decides to develop an ABC system. She identifies three activities: documentation preparation, information technology support, and training. She figures that documentation costs are driven by the number of pages, information technology support costs are driven by the number of software applications used, and training costs are driven by the number of direct labor hours worked.Estimates of the costs and quantities of the allocation bases follow: Activity Estimated Costs Allocation Base Estimated Quantity of Allocation Base Documentation preparation $47,400 Pages 1,530 pages Information technology support $120,600 Applications 700 applications Training $354,800 Direct labor hours 3,240 hours Total Indirect costs $522,800 1. Compute the predetermined overhead allocation rate for each activity. Round to the nearest dollar. Activity Total estimated overhead…arrow_forwardYou have been hired as a Cost Accountant by Sundial, Inc., which produces sunglasses. Your duties include developing cost standards for materials and labor, designing and implementing cost accounting systems, defining various product and operational costs, analyzing production costs and recommending changes. When the trial period is over, you will have a performance review to demonstrate the completed tasks and gained knowledge. You have read the Cost of Quality Report of Sundial, Inc. and discovered that quality costs constitute 4.2% of sales. The amount is enormous, and your boss asks you to develop a set of measures to reduce it. Sundial, Inc. Cost of Quality Report For the Year Cost of Quality Percent of Sales ($32,000,000) Prevention costs $160,000 0.5% Appraisal costs…arrow_forwardSusan Mills, Company B's chief accountant, has developed an automated costing system that helps track the cost of production activities. This system is capable of accurately measuring and allocating post-manufacturing activities, such as selling, promotional, and distribution activities, in such a way where Company B gets a more detailed view of its product costs. One of the benefits of this system is that it allows Company B to determine which product lines are more profitable. When Susan implemented the new costing system, she realized that the company's current period profits would increase significantly if the new product cost information was used for inventory valuation on the financial statements. Susan has been under intense pressure to improve the company's profits, and this would be a quick and effective way for her to help meet the company's short-term profit goals. As a result, Susan has decided to use the automated costing system to determine the company's profits.…arrow_forward

- Susan Mills, Company B's chief accountant, has developed an automated costing system that helps track the cost of production activities. This system is capable of accurately measuring and allocating post-manufacturing activities, such as selling, promotional, and distribution activities, in such a way that Company B gets a more detailed view of its product costs. One of the benefits of this system is that it allows Company B to determine which product lines are more profitable When Susan implemented the new costing system, she realized that the company's current period profits would increase significantly if the new product cost information was used for inventory valuation on the financial statements. Susan has been under intense pressure to improve the company's profits, and this would be a quick and effective way for her to help meet the company's short-term profit goals. As a result, Susan has decided to use the automated costing system to determine the company's profits. 1. Why…arrow_forwardData Performance, a computer software consulting company, has three major functional areas: computer programming, information systems consulting, and software training. Carol Bingham, a pricing analyst, has been asked to develop total costs for the functional areas. These costs will be used as a guide in pricing a new contract. In computing these costs, Carol is considering three different methods of the departmental allocation approach to allocate overhead costs: the direct method, the step method, and the reciprocal method. She assembled the following data from the two service departments, information systems and facilities: Service Departments Production Departments Information Systems Facilities Computer Programming Information Systems Consulting Software Training Total Budgeted overhead (base) $ 368,000 $ 184,000 $ 736,000 $ 874,000 $ 575,000 $ 2,737,000 Information Systems (computer hours) 600 1,200 300 900 3,000 Facilities (square feet) 240 960 600 600…arrow_forwardJay Corporation has provided data from a two-year period to aid in planning. The Controller has asked you to prepare a contribution format income statement. Use the information included in the Excel Simulation and the Excel functions described below to complete the task.arrow_forward

- Joseph Fox, controller of Thorpe Company, has been in charge of a project to install an activity-based cost management system. This new system is designed to support the companys efforts to become more competitive. For the past six weeks, he and the project committee members have been identifying and defining activities, associating workers with activities, and assessing the time and resources consumed by individual activities. Now, he and the project committee are focusing on three additional implementation issues: (1) identifying activity drivers, (2) assessing value content, and (3) identifying cost drivers (root causes). Joseph has assigned a committee member the responsibilities of assessing the value content of five activities, choosing a suitable activity driver for each activity, and identifying the possible root causes of the activities. Following are the five activities with possible activity drivers: The committee member ran a regression analysis for each potential activity driver, using the method of least squares to estimate the variable and fixed cost components. In all five cases, costs were highly correlated with the potential drivers. Thus, all drivers appeared to be good candidates for assigning costs to products. The company plans to reward production managers for reducing product costs. Required: 1. What is the difference between an activity driver and a cost driver? In answering the question, describe the purpose of each type of driver. 2. For each activity, assess the value content and classify each activity as value-added or non-value-added (justify the classification). Identify some possible root causes of each activity, and describe how this knowledge can be used to improve activity performance. For purposes of discussion, assume that the value-added activities are not performed with perfect efficiency. 3. Describe the behavior that each activity driver will encourage, and evaluate the suitability of that behavior for the companys objective of becoming more competitive.arrow_forwardWalsh & Coggins, a professional accounting firm, collects cost information about the services they provide to their clients. Describe the types of cost data they would collect and explain the importance of analyzing this cost data.arrow_forwardThe controller of Tri Con Global System Inc. has developed a new costing system that traces the cost of activities to products. The new system is able to measure post-manufacturing activities such as selling, promotional, and distribution activities, and allocates these activities to products in a manner that provides a more complete view of the company’s product costs. This system produces better strategic information about the relative profitability of products lines. In the course of implementing the new costing system, the controller realized that the company’s current period GAAP net income would increase significantly if the new product cost information were used for inventory valuation on the financial statements. The controller has been under intense pressure to improve the company’s net income, and this would be an easy and effective way for her to help meet the company’s short-term net income goals. As a result, she has decided to use the new costing system to…arrow_forward

- The controller of Tri Con Global Systems Inc. has developed a new costing system that traces the cost of activities to products. The new system is able to measure post-manufacturing activities, such as selling, promotional, and distribution activities, and allocate these activities to products in a manner that provides a more complete view of the company's product costs. This system produces better strategic information about the relative profitability of product lines. In the course of implementing the new costing system, the controller realized that the company's current period GAAP net income would increase significantly if the new product cost information were used for inventory valuation on the financial statements. The controller has been under intense pressure to improve the company's net income, and this would be an easy and effective way for her to help meet the company's short-term net income goals. As a result, she has decided to use the new costing system to determine GAAP…arrow_forwardThe controller of Tri Con Global Systems Inc. has developed a new costing system that traces the cost of activities to products. The new system is able to measure post-manufacturing activities, such as selling, promotional, and distribution activities, and allocate these activities to products in a manner that provides a more complete view of the company's product costs. This system produces better strategic information about the relative profitability of product lines. In the course of implementing the new costing system, the controller realized that the company's current period GAAP net income would increase significantly if the new product cost information were used for inventory valuation on the financial statements. The controller has been under intense pressure to improve the company's net income, and this would be an easy and effective way for her to help meet the company's short-term net income goals. As a result, she has decided to use the new costing system to determine GAAP…arrow_forwardA seminar was recently attended by the Managing Director of XYZ Manufacturing Company Limited located at Sheffield. The focus of the seminar was “optimising scarce resources utility in a manufacturing setting with particular reference to linear programming”. On his return to his base, he called for a meeting with the Management to share his experience from the seminar and the impact this will have on the decision by the Board to produce two major products in the years ahead. A group of external research experts had previously been commissioned and the following represents information from the research carried out by them The expected products are “Best” and “Smart” with expected costs statistics as follows: Best £ Smart £ Material costs (5kg@£50/kg) 250 (3kg@£50/kg) 150 Labour costs Machinery time (4 hours @£15/Hr) 60 (2hours @£15/Hr) 30 Other Processing Time (4 hours @£10/hr) 40 (5hours@£10/Hr) 50 The applicable pricing…arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College