Concept explainers

Videos

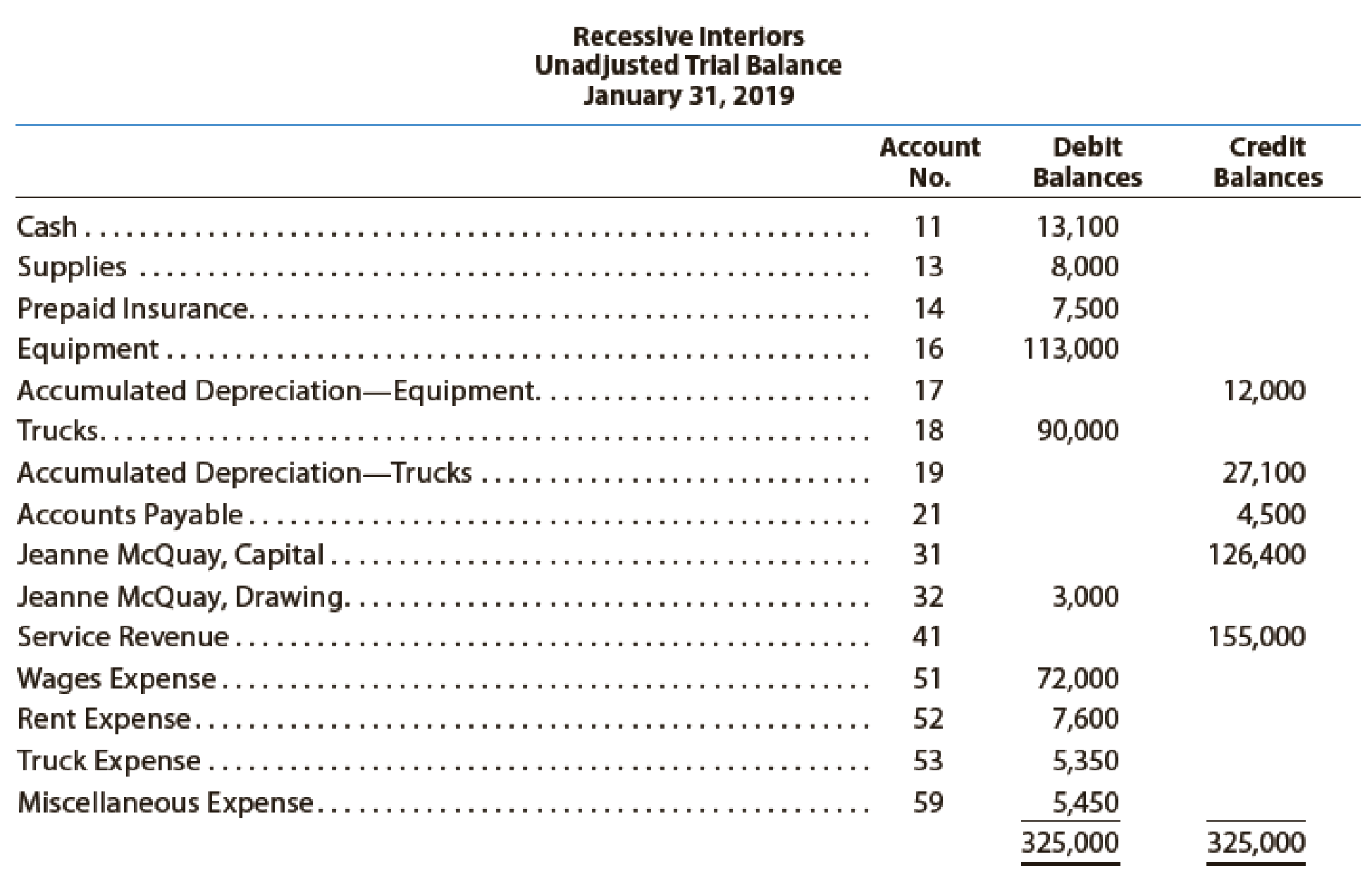

The unadjusted

The data needed to determine year-end adjustments are as follows:

- a. Supplies on hand at January 31 are $2,850.

- b. Insurance premiums expired during the year are $3,150.

- c.

Depreciation of equipment during the year is $5,250. - d. Depreciation of trucks during the year is $4,000.

- e. Wages accrued but not paid at January 31 are $900.

Instructions

- 1. For each account listed in the unadjusted trial balance, enter the balance in the appropriate Balance column of a four-column account and place a check mark (✓) in the Posting Reference column.

- 2. (Optional) Enter the unadjusted trial balance on an end-of-period spreadsheet and complete the spreadsheet. Add the accounts listed in part (3) as needed.

- 3. Journalize and post the

adjusting entries , inserting balances in the accounts affected. Record the adjusting entries on Page 26 of the journal. The following additional accounts from Recessive Interiors’ chart of accounts should be used: Wages Payable, 22; Depreciation Expense—Equipment, 54; Supplies Expense, 55; Depreciation Expense—Trucks, 56; Insurance Expense, 57. - 4. Prepare an adjusted trial balance.

- 5. Prepare an income statement, a statement of owner’s equity (no additional investments were made during the year), and a

balance sheet . - 6. Journalize and

post the closing entries. Record the closing entries on Page 27 of the journal. Indicate closed accounts by inserting a line in both Balance columns opposite the closing entry. - 7. Prepare a post-closing trial balance.

1, 3, and 6:

Prepare the T-accounts.

Explanation of Solution

T-Accounts: T-accounts are referred as T-account because its format represents the letter “T”. The T-accounts consists of the following:

- The title of accounts.

- The debit side (Dr) and,

- The credit side (Cr).

Record the transactions directly in their respective T-accounts, and determine their balances.

| Account: Cash Account no. 11 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 1 | Balance | ✓ | 13,100 | |||

| Account: Supplies Account no. 13 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 31 | Balance | ✓ | 8,000 | |||

| 31 | Adjusting | 26 | 5,150 | 2,850 | |||

| Account: Prepaid Insurance Account no. 14 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 31 | Balance | ✓ | 7,500 | |||

| 31 | Adjusting | 26 | 3,150 | 4,350 | |||

| Account: Equipment Account no. 16 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 31 | Balance | ✓ | 113,000 | |||

| Account: Accumulated Depreciation-Office equipment Account no. 17 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 31 | Balance | ✓ | 12,000 | |||

| 31 | Adjusting | 26 | 5,250 | 17,250 | |||

| Account: Trucks Account no. 18 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 31 | Balance | ✓ | 90,000 | |||

| Account: Accumulated Depreciation- Truck Account no. 19 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 31 | Balance | ✓ | 27,100 | |||

| 31 | Adjusting | 26 | 4,000 | 31,100 | |||

| Account: Accounts Payable Account no. 21 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 31 | Balance | ✓ | 4,500 | |||

| Account: Wages Payable Account no. 22 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 31 | Adjusting | 26 | 900 | 900 | ||

| Account: JM, Capital Account no. 31 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 31 | Balance |

| 126,400 | |||

| 31 | Closing | 27 | 46,150 | 172,550 | |||

| 31 | Closing | 27 | 3,000 | 169,550 | |||

| Account: JM, Drawing Account no. 32 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 31 | Balance | ✓ | 3,000 | |||

| 31 | Closing | 27 | 3,000 | ||||

| Account: Service revenue Account no. 41 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 31 | Balance | ✓ | 155,000 | |||

| 31 | Closing | 27 | 155,000 | ||||

| Account: Wages expense Account no. 51 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 1 | Balance | ✓ | 72,000 | |||

| 31 | Adjusting | 26 | 900 | 72,900 | |||

| 31 | Closing | 27 | 72,900 | ||||

| Account: Rent expense Account no. 52 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 31 | Balance | ✓ | 7,600 | |||

| 31 | Closing | 27 | 7,600 | ||||

| Account: Truck Expense Account no. 53 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 31 | Balance | ✓ | 5,350 | |||

| 31 | Closing | 27 | 5,350 | ||||

| Account: Depreciation Expense- Equipment Account no. 54 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 31 | Adjusting | 26 | 5,250 | 5,250 | ||

| 31 | Closing | 27 | 5,250 | ||||

| Account: Supplies Expenses Account no. 55 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 31 | Adjusting | 26 | 5,150 | 5,150 | ||

| 31 | Closing | 27 | 5,150 | ||||

| Account: Depreciation Expense- Trucks Account no. 56 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 31 | Adjusting | 26 | 4,000 | 4,000 | ||

| 31 | Closing | 27 | 4,000 | ||||

| Account: Insurance expense Account no. 57 | ||||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | |||

| Debit ($) | Credit ($) | |||||||

| 2019 | ||||||||

| January | 31 | Adjusting | 26 | 3,150 | 3,150 | |||

| 31 | Closing | 27 | 3,150 | |||||

| Account: Miscellaneous expense Account no. 59 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 1 | Balance | ✓ | 5,450 | |||

| 31 | Closing | 27 | 5,450 | ||||

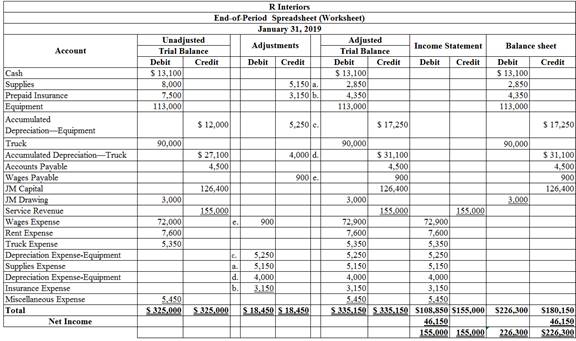

2.

Enter the unadjusted trial balance on an end-of-period spreadsheet, and complete the spreadsheet.

Explanation of Solution

Spreadsheet: A spreadsheet is a worksheet. It is used while preparing a financial statement. It is a type of form having multiple columns and it is used in the adjustment process. The use of a worksheet is optional for any organization. A worksheet can neither be considered as a journal nor a part of the general ledger.

The unadjusted trial balance on an end-of-period spreadsheet is prepared as follows:

Table (1)

Hence, the unadjusted trial balance on an end-of-period spreadsheet is prepared and completed.

3.

Journalize and post the adjusting entries.

Explanation of Solution

Journal: Journal is the book of original entry. Journal consists of the day-to-day financial transactions in a chronological order. The journal has two aspects; they are debit aspect and the credit aspect.

Adjusting entries: An adjusting entry is prepared when the trial balance is not up-to-date, and complete, and they are usually prepared at the end of the accounting period. This adjusting entry is essential for preparing the financial statements of the business.

The adjusting entries are journalized as follows:

| Date | Description |

Post Ref. | Debit ($) | Credit ($) | |

| 2019 | Wages expense | 51 | 900 | ||

| January | 31 | Wages payable | 22 | 900 | |

| (To record the wages accrued) | |||||

Table (2)

- Wages expense is an expense account, and it is increased. Hence, debit the wages expense account by $900.

- Wages payable is a liability account, and it is increased. Hence, credit the wages payable account by $900.

| Date | Description |

Post Ref. | Debit ($) | Credit ($) | |

| 2019 | Depreciation expense-Equipment | 54 | 5,250 | ||

| January | 31 | Accumulated depreciation- Equipment | 17 | 5,250 | |

| (To record the equipment depreciation) | |||||

Table (3)

- Depreciation expense is an expense account, and it is increased. Hence, debit the wages expense account by $5,250.

- Accumulated depreciation is a contra asset account, and it is increased. Hence, credit the accumulated depreciation account by $5,250.

| Date | Description |

Post Ref. | Debit ($) | Credit ($) | |

| 2019 | Depreciation expense-Truck | 56 | 4,000 | ||

| January | 31 | Accumulated depreciation- Truck | 19 | 4,000 | |

| (To record the truck depreciation) | |||||

Table (4)

- Depreciation expense is an expense account, and it is increased. Hence, debit the wages expense account by $4,000.

- Accumulated depreciation is a contra asset account, and it is increased. Hence, credit the accumulated depreciation account by $4,000.

| Date | Description |

Post Ref. | Debit ($) | Credit ($) | |

| 2019 | Supplies expense | 55 | 5,150 | ||

| January | 31 | Supplies | 13 | 5,150 | |

| (To record the supplies expense) | |||||

Table (5)

- Supplies expense is an expense account, and it is increased. Hence, debit the supplies expense account by $5,150.

- Supplies are the asset account, and it is increased. Hence, credit the supplies account by $5,150.

| Date | Description |

Post Ref. | Debit ($) | Credit ($) | |

| 2019 | Insurance expense | 57 | 3,150 | ||

| January | 31 | Prepaid insurance | 14 | 3,150 | |

| (To record the insurance expense) | |||||

Table (6)

- Insurance expense is an expense account, and it is increased. Hence, debit the insurance expense account by $3,150.

- Prepaid insurance is an asset account, and it is decreased. Hence, credit the prepaid insurance account by $3,150.

4.

Prepare an adjusted trial balance for R interiors, as of January 31, 2019.

Explanation of Solution

Adjusted trial balance: The adjusted trial balance is the summary of all the ledger accounts that appears on the ledger accounts after making adjusting journal entries.

Prepare an adjusted trial balance for R interiors, as of January 31, 2019.

| R interiors | |||

| Adjusted Trial Balance | |||

| January 31, 2019 | |||

| Accounts | Account Number | Debit Balances | Credit Balances |

| Cash | 11 | 13,100 | |

| Supplies | 13 | 2,850 | |

| Prepaid Insurance | 14 | 4,350 | |

| Equipment | 16 | 113,000 | |

| Accumulated depreciation- Equipment | 17 | 17,250 | |

| Trucks | 18 | 90,000 | |

| Accumulated depreciation- Trucks | 19 | 31,100 | |

| Accounts payable | 21 | 4,500 | |

| Wages Payable | 22 | 900 | |

| JM, Capital | 31 | 126,400 | |

| JM, Drawing | 32 | 3,000 | |

| Service revenue | 41 | 155,000 | |

| Wages expense | 51 | 72,900 | |

| Rent expense | 52 | 7,600 | |

| Truck Expense | 53 | 5,350 | |

| Depreciation Expense- Equipment | 54 | 5,250 | |

| Supplies expense | 55 | 5,150 | |

| Depreciation Expense- Trucks | 56 | 4,000 | |

| Insurance Expense | 57 | 3,150 | |

| Miscellaneous Expense | 59 | 5,450 | |

| 335,150 | 335,150 | ||

Table (7)

The debit column and credit column of the adjusted trial balance are agreed, both having balance of $335,150.

5.

Prepare income statement, statement of owners’ equity, and a balance sheet for the year ended January 31, 2019.

Explanation of Solution

Income statement: An income statement is one of the financial statements which shows the revenues, and expenses of the company. The income statement is prepared to ascertain the net income/loss of the company, by deducting the expenses from the revenues.

Statement of owners’ equity: This statement reports the beginning owner’s equity and all the changes, which led to ending owners’ equity. Additional capital, net income from income statement is added to and drawing is deducted from beginning owner’s equity to arrive at the end result, ending owner’s equity.

Balance sheet: A balance sheet is a financial statement consists of the assets, liabilities, and the stockholder’s equity of the company. The balance of the assets account must be equal to that of the liabilities and the stockholder’s equity account.

Prepare income statement for the year ended January 31, 2019.

| R interiors | ||

| Income Statement | ||

| For the year ended January 31, 2019 | ||

| Particulars | Amount ($) | Amount ($) |

| Revenue: | ||

| Laundry revenue | $155,000 | |

| Expenses: | ||

| Wages Expense | $72,900 | |

| Rent Expense | 7,600 | |

| Truck Expense | 5,350 | |

| Depreciation Expense-Equipment | 5,250 | |

| Supplies Expense | 5,150 | |

| Depreciation Expense-Trucks | 4,000 | |

| Insurance Expense | 3,150 | |

| Miscellaneous Expense | 5,450 | |

| Total Expenses | 108,850 | |

| Net Income | $46,150 | |

Table (8)

Prepare statement of owners’ equity for the year ended January 31, 2019.

| R interiors | ||

| Statement of Owner’s Equity | ||

| For the Year Ended January 30, 2019 | ||

| Particulars | Amount ($) | Amount ($) |

| JM Capital, February1, 2018 | $126,400 | |

| Add: Net income | $46,150 | |

| Less: Drawings | (3,000) | |

| Increase in owner’s equity | 43,150 | |

| JM Capital, January 31, 2019 | $169,550 | |

Table (9)

Prepare the balance sheet of R interiors at January 31, 2019.

| R interiors | |||

| Balance Sheet | |||

| For the year ended January 31, 2019 | |||

| Assets | |||

| Current Assets: | |||

| Cash | $13,100 | ||

| Supplies | 2,850 | ||

| Prepaid Insurance | 4,350 | ||

| Total Current Assets | $20,300 | ||

| Property, plant and equipment: | |||

| Equipment | $113,000 | ||

| Less: Accumulated Depreciation- Equipment | 17,250 | 95,750 | |

| Trucks | 90,000 | ||

| Less: Accumulated Depreciation- Trucks | 31,100 | 58,900 | |

| Total property, plant, and equipment | 154,650 | ||

| Total Assets | $174,950 | ||

| Liabilities | |||

| Current Liabilities: | |||

| Accounts Payable | $4,500 | ||

| Wages Payable | 900 | ||

| Total Liabilities | $5,400 | ||

| Owner’s Equity | |||

| JM’s capital | 169,550 | ||

| Total Liabilities and Owners’ Equity | $174,950 | ||

Table (10)

Therefore, the total assets and total liabilities plus owners’ equity of R interiors at January 31, 2019 is $174,950.

6.

Journalize the closing entries for R interiors.

Explanation of Solution

Closing entries: Closing entries are recorded in order to close the temporary accounts such as incomes and expenses by transferring them to the permanent accounts. It is passed at the end of the accounting period, to transfer the final balance.

Closing entry for revenue and expense accounts:

| Date | Accounts title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 31, 2019 | Service Revenue | 41 | 155,000 | |

| Wages Expense | 51 | 72,900 | ||

| Rent Expense | 52 | 7,600 | ||

| Truck Expense | 53 | 5,350 | ||

| Depreciation Expense- Equipment | 54 | 5,250 | ||

| Supplies Expense | 55 | 5,150 | ||

| Depreciation Expense- Trucks | 56 | 4,000 | ||

| Insurance Expense | 57 | 3,150 | ||

| Miscellaneous Expense | 59 | 5,450 | ||

| JM, Capital | 31 | 46,150 | ||

| (To close the revenues and expenses account. Then the balance amount are transferred to owners’ capital account) | ||||

| January 31 | JM’s Capital | 31 | 3,000 | |

| JM’ Drawing | 32 | 3,000 | ||

| (To Close the capital and drawings account) | ||||

Table (11)

- Service revenue is revenue account. Since the amount of revenue is closed, and transferred to JM’s capital account. Here, R interiors earned an income of $155,000. Therefore, it is debited.

- Wages Expense, Rent Expense, Insurance Expense, Utilities Expense, Laundry Supplies Expense, Depreciation Expense, JM Capital, and Miscellaneous Expense are expense accounts. Since the amount of expenses are closed to Income Summary account. Therefore, it is credited.

- Owner’s capital is a component of owner’s equity. Thus, owners ‘equity is debited since the capital is decreased on owners’ drawings.

- Owner’s drawings are a component of owner’s equity. It is credited because the balance of owners’ drawing account is transferred to owners ‘capital account

7.

Prepare the post–closing trial balance of R interiors for the year ended January 31, 2019.

Explanation of Solution

Post-Closing Trial Balance: After passing all the journal entries and the closing entries of the permanent accounts and then further posting them to each of the respective accounts, a post-closing trial balance is prepared which consists of a list of all the permanent accounts. A post-closing trial balance serves as an evidence to prove that the balance of the permanent accounts is equal.

Prepare a post–closing trial balance of R interiors for the year ended January 31, 2019.

|

R interiors Post-closing Trial Balance January 31, 2019 | |||

| Particulars |

Account Number | Debit $ | Credit $ |

| Cash | 11 | 13,100 | |

| Supplies | 13 | 2,850 | |

| Prepaid insurance | 14 | 4,350 | |

| Equipment | 16 | 113,000 | |

| Accumulated depreciation- Equipment | 17 | 17,250 | |

| Trucks | 18 | 90,000 | |

| Accumulated depreciation- Trucks | 19 | 31,100 | |

| Accounts payable | 21 | 4,500 | |

| Wages payable | 22 | 900 | |

| JM’s Capital | 31 | 169,550 | |

| Total | 223,300 | 223,300 | |

Table (12)

Want to see more full solutions like this?

Chapter 4 Solutions

Financial Accounting

- The following are independent errors: a. In January 2019, repair costs of 9,000 were debited to the Machinery account. At the beginning of 2019, the book value of the machinery was 100,000. No residual value is expected, the remaining estimated life is 10 years, and straight-line depreciation is used. b. All purchases of materials for construction contracts still in progress have been immediately expensed. It is discovered that the use of these materials was 10,000 during 2018 and 12,000 during 2019. c. Depreciation on manufacturing equipment has been excluded from manufacturing costs and treated as a period expense. During 2019, 40,000 of depreciation was accounted for in that manner. Production was 15,000 units during 2019, of which 3,000 remained in inventory at the end of the year. Assume there was no inventory at the beginning of 2019. Required: Prepare journal entries for the preceding errors discovered during 2020. Ignore income taxes.arrow_forwardAt the end of 2019, Framber Company received 8,000 as a prepayment for renting a building to a tenant during 2020. The company erroneously recorded the transaction by debiting Cash and crediting Rent Revenue in 2019 instead of 2020. Upon discovery of this error in 2020, what correcting journal entry will Framber make? Ignore income taxes.arrow_forwardNewton Labs leased chronometers from Brookline Instruments on January 1, 2021. Brookline Instruments manufactured the chronometers at a cost of $180,000. The chronometers have a fair value of $225,154. Appropriate adjusting entries are made quarterly. (FV of $1. PV of $1. EVA of $1. PVA of $1. EVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.) Related Information: Lease tern Quarterly lease payments Economic life of asset Estimated residual value of chronometers at end of lease tern Interest rate charged by the lessor Required: 1. Prepare appropriate entries for Newton Labs to record the arrangement at its commencement, January 1, 2021, and on March 31, 2021. 2. Prepare appropriate entries for Brookline Instruments to record the arrangement at its commencement, January 1, 2021, and on March 31, 2021. Answer is not complete. Complete this question by entering your answers in the tabs below. Required 1 Required 2 Prepare appropriate entries for Newton Labs…arrow_forward

- While reviewing the company’s records for 2019 and 2020, Ms. Croft discovered that no adjustments were made for the following items.1. Interest income of $14,100 was not accrued at the end of 2019. It was recordedwhen received in February 2020.2. A computer costing $4000 was expensed when purchased on July 1, 2019. It isexpected to have a 4 year life with no residual value. The company typically usesstraight line depreciation for all fixed assets.3. Research costs of $33,000 were incurred early in 2019. They were capitalized andwere to be amortized over a 3-year period. Amortization of $11,000 was recordedfor 2019 and $11,000 for 2020.4. On January 2, 2019, Jolie Inc. leased a building for 5 years at a monthly rental of$8,000. On that date, the company paid the following amounts, which wereexpensed when paid.Security deposit $20,000First month’s rent 8,000Last month’s rent 8,000 $36,0005. The company received $36,000 from a customer at the beginning of 2019 forservices that it is to…arrow_forwardNewton Labs leased chronometers from Brookline Instruments on January 1, 2021. Brookline Instruments manufactured the chronometers at a cost of $230,000. The chronometers have a fair value of $242,340. Appropriate adjusting entries are made quarterly. (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.) Related Information: Lease term 5 years (20 quarterly periods) Quarterly lease payments $ 16,729 at Jan. 1, 2021, and at Mar. 31, June 30, Sept. 30, and Dec. 31 thereafter. Economic life of asset 6 years Estimated residual value of chronometers at end of lease term $ 12,912 Interest rate charged by the lessor 16% Required:1. Prepare appropriate entries for Newton Labs to record the arrangement at its commencement, January 1, 2021, and on March 31, 2021.2. Prepare appropriate entries for Brookline Instruments to record the arrangement at its commencement, January 1, 2021, and on March 31,…arrow_forwardBeaver Construction purchases new equipment for $42,480 cash on April 1, 2021. At the time of purchase, the equipment is expected to be used in operations for six years (72 months) and have no resale or scrap value at the end. Beaver depreciates equipment evenly over the 72 months ($590/month). 1.&2. Record the necessary entries in the Journal Entry Worksheet below. 3. Calculate the year-end adjusted balances of Accumulated Depreciation and Depreciation Expense (assuming the balance of Accumulated Depreciation at the beginning of 2021 is $0). Accumulated Depreciation ending balance: _____________ Depreciation Expense ending balance:__________________arrow_forward

- In completing the adjusting entries for 2021 in early 2022, the internal auditor discovered that a patent, with an estimated eight year life that was registered in January, 2021 had not been amortized. The patent cost $370,000. The income tax rate is 40%. The books are still open in 2021. What is the journal entry to correct the error? Group of answer choices Amortization Expense-Patent 46,250 Retained Earnings46,250 Patent 46,250 Income Taxes Receivable18,500 Retained Earnings 64,750 Amortization Expense-Patent 46,250 Income Taxes Payable18,500 Retained Earnings 27,750 Amortization Expense-Patent 46,250 Patent 46,250 PreviousNextarrow_forwardAccounting Two fixed assets are purchased during 2021: a copier for $10,987.65 on September 30, 2021 and an office desk for 5,432.10 on December 31, 2021. Depreciation entries are recorded at the end of each month. What will be general journal adjusting entry on December 31, 2021 for the depreciation of these fixed assets, if tax basis 150% MACRS is used?arrow_forwardThe Laura Company has the following errors on its books as of December 31, 2020. The books for 2020 have not yet been closed. a. In 2020, fully depreciated equipment (with no residual value) that originally cost $8,000 was sold for $700 as scrap. The company credited the $700 proceeds to Equipment. b. On January 1, 2019, the company recorded the purchase of equipment in exchange for a three-year, noninterest-bearing note payable in the amount of $10,000. Interest rates were then 8%, but no recognition was made of this fact. The present value of $1 at 8% for three periods is 0.7938. (Ignore depreciation.) Required: Prepare journal entries to correct these errors at December 31, 2020. Ignore income taxes.arrow_forward

- The Richards Company paid for a five-year extended warranty on all of their equipment on March 1, 2019 costing $540,000 that went into effect immediately. The fiscal year is the calendar year. what if Richards mistakenly or purposely charged the entire total as an expense in 2019? Assuming that all other accounting during the year had been performed correctly, i.e. in a consistent manner under GAAP (Generally Accepted Accounting Principles), in what ways would this error affect overall totals for 2019 of the six items below. No dollar figures are required in this table. Just place one check mark in each column to identify the impact of this misclassification on that category. Impact On Reported Figures For 2019 if the total payment had been expensed when paid. (Place One Check Mark in Each Column Below) Owners' Assets Liabilities Equity (Retained Earnings) Impact Revenues Expenses Income Overstated Understated No Effectarrow_forwardA company purchases equipment for $40,000 on Aug 1, 2019. It estimates that the equipment will have a salvage value of 4,000 and its useful life will be 9 years. It is the company’s policy to charge a full years depreciation on the year of purchase and no depreciation charge on the year of disposal. Assuming that the company's accounting year ends on December 31 of each year, what will be the Depreciation Expense for the years 2020 assuming straight-line depreciation?arrow_forwardOn Jan 1,2020, Kim Co. supplies amounted to P2,500. During the year, thecompany purchased P1,200 worth of supplies. Because of some defects, theyreturned P300 to the suppliers. At year end, the supplies amounted to P1,800.What is the amount of supplies expense?arrow_forward

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT