Concept explainers

Videos

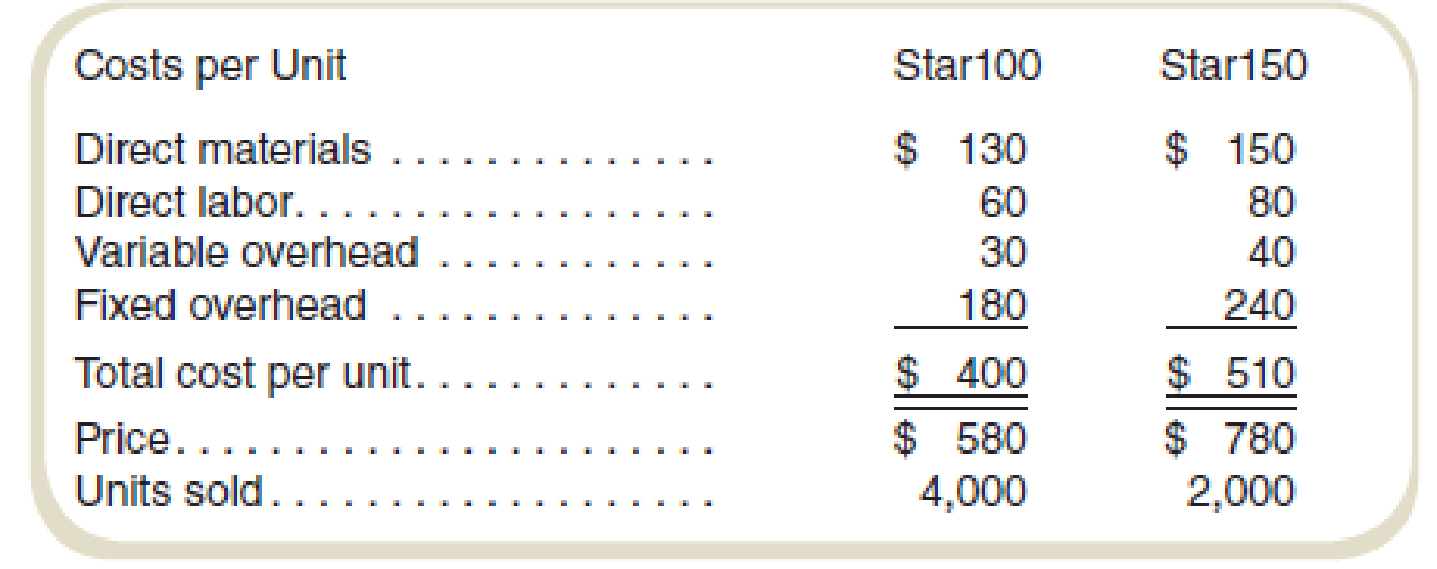

Unter Components

The average wage rate is $40 per hour. Variable

Required

- a. A nationwide car-sharing service has offered to buy 2,500 Star100 systems and 2,500 Star150 systems if the price is lowered to $400 and $500, respectively, per unit. If Unter accepts the offer, how many direct labor-hours will be required to produce the additional systems? How much will the profit increase (or decrease) if Unter accepts this proposal? Prices on regular sales will remain the same.

- b. Suppose that the car-sharing has offered instead to buy 3,500 each of the two models at $400 and $500, respectively. This customer will purchase the 3,500 units of each model only in an all-or-nothing deal. That is, Unter must provide all 3,500 units of each model or none. Unter’s management has decided to fill the entire special order for both models. In view of its capacity constraints, Unter will reduce sales to regular customers as needed to fill the special order. How much will the profits change if the order is accepted? Assume that the company cannot increase its production capacity to meet the extra demand.

- c. Answer the question in requirement (b), assuming instead that the plant can work overtime. Direct labor costs for the overtime production increase to $60 per hour. Variable overhead costs for overtime production are $10 per hour more than for normal production.

a.

Identify, if Company U accepts the offer, how many direct labors will be required to produce the additional systems, and calculate the change in profit in case of company accepts the offer.

Explanation of Solution

Calculate direct labor hours per unit:

| Particulars | Star 100 | Star 150 |

| Labor cost per unit (A) | $60 | $80 |

| Wage rate per labor hour (B) | $40 | $40 |

| Labor hours per unit (A) ÷ (B) | 1.5 hours | 2 hours |

Table (1)

Calculate total direct labor hours required for the additional business.

The current production uses 10,000 direct labor hours and capcity is 20,000 direct labor hours. Thus capacity will not have to expanded to accept the order.

Calculate the change in profit:

| Particulars | Star 100 | Star 150 | Total |

| Units (A) | $2,500 | $2,500 | |

| Sales price (B) | $400 | $500 | |

| Variable costs (C) | $220 | $270 | |

| Differential revenue (A × B) | $1,000,000 | $1,250,000 | $2,250,000 |

| Less: Differential variable cost (A × C) | $550,000 | $675,000 | $1,225,000 |

| Differential Profit | $450,000 | $575,000 | $1,025,000 |

Table (2)

Thus, the differential operating profit is $1,025,000, so Company U should accept the offer.

Working note 1:

Calculate the variable costs:

| Particulars | Star 100 | Star 150 |

| Direct materials | $130 | $150 |

| Add: Direct labor | $60 | $80 |

| Variable overheads | $30 | $40 |

| Total variable costs | $220 | $270 |

Table (3)

b.

Calculate the change in profit in case of acceptance of the offer.

Answer to Problem 53P

The increase in profit is $895,000 if it accepts the offer. So the company should accept the offer.

Explanation of Solution

Calculate total direct labor hours required for the additional business.

The total production time required is 10,000 hours for normal business and 12,250 direct labor hours for the special order, but the direct labor hours capacity is limited to 20,000 hours. In this case, company need to reduce the production of the units sold to the regular customers.

Due to direct labor time is the constraing resource, the companyhaving two alternatives, one is company need to reduce the number of star 100 machines sold to the regular customers, and the second is company need to reduce the number of start 150 machines sold to the regular customers.

Calculate the contribution margin per direct labor hour for each product on the basis of regular customers:

| Particulars | Star 100 | Star 150 |

| Revenue per unit | $580 | $780 |

| Less: Variable cost per unit | $220 | $270 |

| Contribution margin per unit (A) | $360 | $510 |

| Direct labor hours per unit (B) | 1.5 | 2 |

| Contribution margin per hour (A ÷ B) | $240 | $255 |

Table (4)

Star 100 model has the lower contribution margin per hour compared with the star 150 model. The company should reduce the production of this product to sell the special order.

After producing the special order, the company will have 7,750 direct labor hours (20,000 direct labor hours – 12,250 direct labor hours). Company will produce first 2,000 units of srtar 150 model (4,000 direct labor hours = 2,000 units × 2 direct labor hours). The balance direct labor hours ( 3,750 direct labor hours = 7,750 direct labor hours – 4,000 direct labor hours) to produce 2,500 units of the star 100 model.

Calculate the change in operating profit:

Thus, the changes in profit are $895,000, if it accepts the offer. So the company should accept the offer.

Working note 2:

Calculate the contribution margin in case of special order and normal production:

| Particulars | Star 100 | Star 150 | Total |

| Special order: | |||

| Sales price | $400 | $500 | |

| Less: Variable cost | $220 | $270 | |

| Contribution margin per unit (A) | $180 | $230 | |

| Number of units (B) | 3,500 | 3,500 | |

| Total contribution margin ( 1 =A × B) | $630,000 | $805,000 | $1,435,000 |

| Regular production: | |||

| Sales price | $580 | $780 | |

| Less: Variable cost | $220 | $270 | |

| Contribution margin per unit (A) | $360 | $510 | |

| Number of units (B) | 2,500 | 2,000 | |

| Total contribution margin ( 2 =A × B) | $900,000 | $1,020,000 | $1,920,000 |

| Total contribution margin (1 + 2) | $1,530,000 | $1,825,000 | $3,355,000 |

| Less: Fixed Costs | $720,000 | $480,000 | $1,200,000 |

| Net Operating Income (3) | $810,000 | $1,345,000 | $2,155,000 |

Table (5)

Working note 3:

Total contribution margin in case of normal course of business:

| Particulars | Star 100 | Star 150 | Total |

| Regular production: | |||

| Sales price | $580 | $780 | |

| Less: Variable cost | $220 | $270 | |

| Contribution margin per unit (A) | $360 | $510 | |

| Number of units (B) | 4,000 | 2,000 | |

| Total contribution margin ( C =A × B) | $1,440,000 | $1,020,000 | $2,460,000 |

| Less: Fixed costs | $720,000 | $480,000 | $1,200,000 |

| Net operating Income (4) | $720,000 | $540,000 | $1,260,000 |

Table (6)

c.

Calculate the change in profit in case of acceptance of the offer with the given change.

Answer to Problem 53P

The change in profit is $1,367,500 if it accepts the offer. So the company should accept the offer.

Explanation of Solution

Contribution margin:

The excess of sales price over the variable expenses is referred to as the contribution margin. It is computed by deducting the variable expenses from the sales revenue. A contribution margin income statement is prepared in order to record the contribution margin.

Calculate the change in operating profit:

Thus, the change in profit is $1,367,500 if, it accepts the offer. So the company should accept the offer.

Working note 4:

Calculate the contribution margin in case of special order:

| Particulars | Star 100 | Star 150 | Total |

| Special order: | |||

| Sales price | $400 | $500 | |

| Less: Variable cost | $220 | $270 | |

| Contribution margin per unit (A) | $180 | $230 | |

| Number of units (B) | 3,500 | 3,500 | |

| Total contribution margin ( 1 =A × B) | $630,000 | $805,000 | $1,435,000 |

| Regular production: | |||

| Sales price | $580 | $780 | |

| Less: Variable cost | $220 | $270 | |

| Contribution margin per unit (A) | $360 | $510 | |

| Number of units (B) | 4,000 | 2,000 | |

| Total contribution margin ( 2 =A × B) | $1,440,000 | $1,020,000 | $2,460,000 |

| Gross contribution margin (1 + 2) | $2,070,000 | $1,825,000 | $3,895,000 |

| Less: Additional direct labor costs | $45,000 | ||

| Additional variable overhead | $22,500 | ||

| Total contribution margin | $3,827,500 | ||

| Less: Fixed costs | $720,000 | $480,000 | $1,200,000 |

| Net operating Income | $2,627,500 |

Table (7)

Working note 5:

Calculate the additional labor costs:

Calculate the additional variable costs:

Want to see more full solutions like this?

Chapter 4 Solutions

Fundamentals Of Cost Accounting (6th Edition)

- Marvel Parts, Incorporated, manufactures auto accessories. One of the company's products is a set of seat covers that can be adjusted to fit nearly any small car. The company has a standard cost system in use for all of its products. According to the standards that have been set for the seat covers, the factory should work 1,045 hours each month to produce 2,090 sets of covers. The standard costs associated with this level of production are: Direct materials Direct labor Variable manufacturing overhead (based on direct labor-hours) Direct materials (6,500 yards) Direct labor Variable manufacturing overhead Total $ 49,533 $ 10,450 $ 4,598 1. Materials price variance 1. Materials quantity variance 2. Labor rate variance 2. Labor efficiency variance 3. Variable overhead rate variance 3. Variable overhead efficiency variance Per Set of Covers $ During August, the factory worked only 800 direct labor-hours and produced 1,900 sets of covers. The following actual costs were recorded during…arrow_forwardPlata Company produces two products: a mostly handcrafted soft leather briefcase sold under the label Maletin Elegant and a leather briefcase produced largely through automation and sold under the label Maletin Fina. The two products use two overhead activities, with the following costs: Setting up equipment $ 3,000 Machining 19,000 The controller has collected the expected annual prime costs for each briefcase, the machine hours, the setup hours, and the expected production. Elegant Fina Direct labor $9,000 $3,000 Direct materials $3,000 $3,000 Units 3,000 3,000 Machine hours 500 4,500 Setup hours 100 100 Required Calculate the consumption ratios for each activity. Round your answers to one decimal place. Elegant Fina Machining fill in the blank 2 fill in the blank 3 Setups fill in the blank 4 fill in the blank 5 a. Calculate the overhead cost per unit for each briefcase by using a plantwide rate based on direct labor costs. Round to the…arrow_forwardLloyd Gettys, a client of Kevin Lomax, is considering two different processes to make his product—process 1 and process 2. Process 1 requires Lloyd to manufacture subcomponents of the product in-house. As a result, materials are less expensive, but fixed overhead is higher. Process 2 involves purchasing all subcomponents from outside suppliers. The direct materials costs are higher, but fixed factory overhead is considerably lower. Relevant data for a sales level of 30,000 units follow: Process 1 Process 2 Sales $8,010,000 $8,010,000 Variable expenses 2,700,000 4,200,000 Contribution margin $5,310,000 $3,810,000 Less total fixed expenses 3,650,625 1,428,750 Operating income $1,659,375 $2,381,250 Unit selling price $267 $267 Unit variable cost $90 $140 Unit contribution margin $177 $127 a. Compute the degree of operating leverage for each process. b. Suppose that sales are 20 percent higher than budgeted. By what percentage will operating income increase for each process? What will be…arrow_forward

- Marvel Parts, Incorporated, manufactures auto accessories. One of the company's products is a set of seat covers the can be adjusted to fit nearly any small car. The company has a standard cost system in use for all of its products. According to the standards that have been set for the seat covers, the factory should work 1,015 hours each month tc produce 2,030 sets of covers. The standard costs associated with this level of production are: Direct materials Direct labor Variable manufacturing overhead (based on direct labor-hours) Direct materials (8,400 yards) Direct labor Variable manufacturing overhead Total $ 59,276 $8,120 $ 3,857 During August, the factory worked only 700 direct labor-hours and produced 1,500 sets of covers. The following actu costs were recorded during the month: Total $ 42,000 $ 6,300 $ 3,150 Per Set of Covers $ 29.20 4.00 1. Materials price variance 1. Materials quantity variance 2. Labor rate variance 2. Labor efficiency variance 3. Variable overhead rate…arrow_forwardAltex Inc. manufactures two products: car wheels and truck wheels. To determine the amount of overhead to assign to each product line, the controller, Robert Hermann, has developed the following information. Estimated wheels produced Direct labor hours per wheel Activity Cost Pools Setting up machines Assembling Inspection Car Total estimated overhead costs for the two product lines are $835,200. Assembling 39,000 Hermann is not satisfied with the traditional method of allocating overhead because he believes that most of the overhead costs relate to the truck wheels product line because of its complexity. He therefore develops the following three activity cost pools and related cost drivers to better understand these costs. Setting up machines $ Inspection 1 Truck 11,000 S Estimated Use of Cost Drivers 1.000 setups 72.000 labor hours 1.200 inspections 3 Compute the activity-based overhead rates for these three cost pools. Estimated Overhead Overhead Rates Costs $216,000 360,000 259,200arrow_forwardTool Time manufactures carpenter-grade screwdrivers. The company is trying to decide whether to continue to make the case in which the screwdrivers are sold, or to outsource the case to another company. The direct material and direct labor cost to produce the cases total $2.40 per case. The overhead cost is $1.00 per case which consists of $0.40 in variable overhead that would be eliminated if the cases are bought from the outside supplier. The $0.60 of fixed overhead is based on expected production of 400,000 cases per year and consists of the salary of the case production manager of $80,000 per year, along with the remainder consisting of rent, insurance, and depreciation on equipment that will have no resale value. The manager will be laid off if the cases were bought externally. The outside supplier has offered to supply the cases for $3.40 each. How much will Tool Time save or lose if the cases are bought externally? Save $0.40 per case Lose $0.20 per case…arrow_forward

- Ellis Equipment (EE), manufactures three models of lawn tractor: EE-1000, EE-1800, and EE-2800. Because of the different materials used, production processes for each model differ significantly in terms of machine types and time requirements. Once parts are produced, however, assembly time per unit required for each type of tractor is similar. For this reason, EE allocates overhead on the basis of machine-hours. Last quarter, the company shipped 8,000 EE-1000s, 3,200 EE-1800s, and 800 EE-2800s. The revenues and expenses for the last quarter were as follows: ELLIS EQUIPMENT Income Statement For the Quarter Ended June 30 EE-1000 EE-1800 EE-2800 Total Sales revenue $ 12,800,000 $ 8,000,000 $ 3,520,000 $ 24,320,000 Direct costs Direct materials 4,800,000 3,200,000 1,120,000 9,120,000 Direct labor 1,680,000 768,000 230,400 2,678,400 Variable overhead Setting up machines 1,400,000 Quality testing 1,800,000 Painting 780,000…arrow_forwardNowitzki Corporation manufactures swishbombs,a basketball related product. They have a heavily automated manufacturing process. They run production on two different versions of this product . Nowitzki Corp. estimates annual overhead for the period to be $550,000. Due to their manufacturing process, they use machine hours as their basis for overhead allocation. They estimate total machine hours used will be 110,000 machine hoursJob I uses 60,000 machine hours and Job 2 uses 50,000 machine hours Based on the above information calculate predetermined overhead rate (round to nearest cent if needed).arrow_forwardMarvel Parts, Incorporated, manufactures auto accessories. One of the company's products is a set of seat covers that can be adjusted to fit nearly any small car. The company has a standard cost system in use for all of its products. According to the standards that have been set for the seat covers, the factory should work 995 hours each month to produce 1,990 sets of covers. The standard costs associated with this level of production are: Direct materials Direct labor Variable manufacturing overhead (based on direct labor-hours) Direct materials (8,800 yards) Direct labor Variable manufacturing overhead Total $ 47,362 $ 8,955 $ 2,388 During August, the factory worked only 1,000 direct labor-hours and produced 2,300 sets of covers. The following actual costs were recorded during the month: Per Set of Covers $ 23.80 4.50 Total $ 50,600 $ 10,580 $ 4,600 1. Materials price variance 1. Materials quantity variance 2. Labor rate variance 1.20 $29.50 2. Labor efficiency variance 3. Variable…arrow_forward

- Marvel Parts, Incorporated, manufactures auto accessories. One of the company's products is a set of seat covers that can be adjuste to fit nearly any small car. The company has a standard cost system in use for all of its products. According to the standards that have been set for the seat covers, the factory should work 990 hours each month to produce 1,980 sets of covers. The standard costs associated with this level of production are: Direct materials Direct labor Variable manufacturing overhead (based on direct labor-hours) Direct materials (7,400 yards) Direct labor Variable manufacturing overhead Total $ 39,798 $5,940 $ 3,168 During August, the factory worked only 1,000 direct labor-hours and produced 2,200 sets of covers. The following actual costs were recorded during the month: Per Set of Covers $ 20.10 3.00 Total $ 40,700 $ 8,140 $ 3,960 1. Materials price variance 1. Materials quantity variance 2. Labor rate variance 1.60 $24.70 2. Labor efficiency variance 3. Variable…arrow_forwardTerry Industries produces two electronic decoders, P and Q. Decoder P is more sophisticated and requires more programming and testing than does Decoder Q. Because of these product differences, the company wants to use activity-based costing to allocate overhead costs. It has identified four activity pools. Relevant information follows. Activity Pools Repair and maintenance on assembly machine Cost Pool Total Cost Driver Number of units produced 121,800 Number of programming Programming cost 94,240 hours Number of inspections Number of tests Software inspections Product testing 7,560 11,780 $235,380 Total overhead cost Expected activity for each product follows. Number of Number Number Programming of Units of Number Inspections of Tests Hours Decoder 21,000 2,300 182 1,300 P Decoder 1,500 37,000 98 1,800 Q Total 58,000 3,800 280 3,100 Required: a. Compute the overhead rate for each activity pool. (Round your answers to 2 decimal places.) Allocation Rate Activity Pools Decoder P Decoder…arrow_forwardUnter Components manufactures low-cost navigation systems for installation in ride-sharing cars. It sells these systems to various car services that can customize them for their locale and business model. It manufactures two systems, the Star100 and the Star150, which differ in terms of capabilities. The following information is available. Costs per unit Star100 Star150 Direct materials $ 130 $ 150 Direct labor 60 80 Variable overhead 30 40 Fixed overhead 180 240 Total cost per unit $ 400 $ 510 Price $ 580 $ 780 Units sold 4,000 2,000 The average wage rate is $40 per hour. Variable overhead varies with the quantity of direct labor-hours. The plant has a capacity of 20,000 direct labor-hours, but current production uses only 10,000 direct labor-hours. Required: a. A nationwide car-sharing service has offered to buy 2,500 Star100 systems and 2,500 Star150 systems if the price is lowered to $400 and…arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning