Videos

Complex

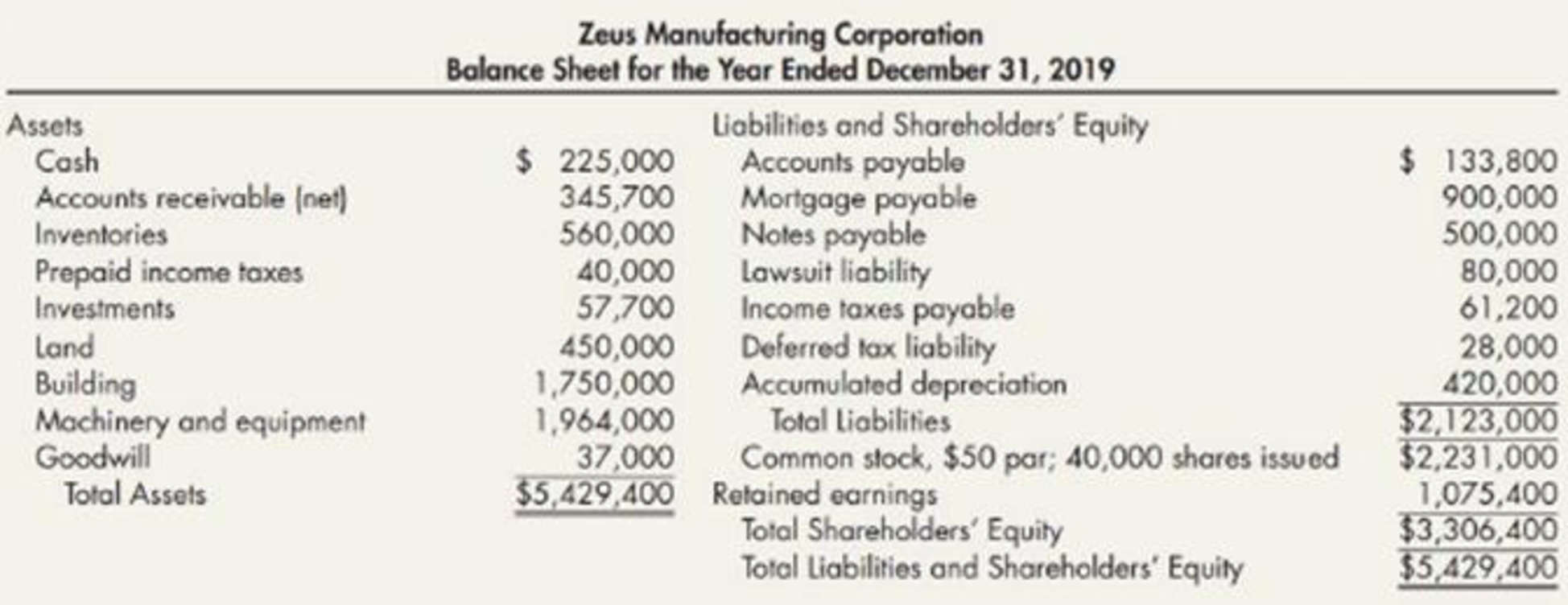

Your company has been engaged to perform an audit, during which you discover the following information:

- 1. Checks totaling $14,000 in payment of accounts payable were mailed on December 31, 2019, but were not recorded until 2020. Late in December 2019, the bank returned a customer’s $2,000 check marked “NSF,” but no entry was made. Cash includes $100,000 restricted for building purposes.

- 2. Included in accounts receivable is a $30,000 note due on December 31, 2022, from Zeus’s president.

- 3. During 2019, Zeus purchased 500 shares of common stock of a major corporation that supplies Zeus with raw materials. Total cost of this stock was $51,300, and fair value on December 31, 2019, was $51,300. Zeus plans to hold these shares indefinitely.

- 4.

Treasury stock was recorded at cost when Zeus purchased 200 of its own shares for $32 per share in May 2019. This amount is included in investments. - 5. On December 31, 2019, Zeus borrowed $500,000 from a bank in exchange for a 10% note payable, manning December 31, 2024. Equal principal payments are due December 31 of each year beginning in 2020. This note is collateralized by a $250,000 tract of land acquired as a potential future building site, which is included in land.

- 6. The mortgage payable requires $50,000 principal payments, plus interest, at the end of each month. Payments were made on January 31 and February 28, 2020. The balance of this mortgage was due June 30, 2020. On March 1, 2020, prior to issuance of the audited financial statements, Zeus consummated a non-cancelable agreement with the lender to refinance this mortgage. The new terms require $100,000 annual principal payments, plus interest, on February 28 of each year, beginning in 2021. The final payment is due February 28, 2028.

- 7. The lawsuit liability will be paid in 2020.

- 8. Of the total

deferred tax liability ; $5,000 is considered a current liability. - 9. The current income tax expense reported in Zeus’s 2019 income statement was $61,200.

- 10. The company was authorized to issue 100,000 shares of $50 par value common stock.

Prepare a corrected classified balance sheet as of December 31, 2019.

Explanation of Solution

Balance sheet: This financial statement reports a company’s resources (assets) and claims of creditors (liabilities) and stockholders (stockholders’ equity) over those resources. The resources of the company are assets which include money contributed by stockholders and creditors. Hence, the main elements of the balance sheet are assets, liabilities, and stockholders’ equity.

Prepare a corrected classified balance sheet of Company Z:

| Company Z | |||

| Balance Sheet | |||

| December 31,2019 | |||

| Current Assets: | Amount ($) | Amount ($) | Amount ($) |

| Cash (1) | 109,000 | ||

| Accounts receivable (net) (2) | 317,700 | ||

| Inventories | 560,000 | ||

| Total current assets | 986,700 | ||

| Long-Term Investment, at fair value (3) | 51,300 | ||

| Property, Plant, and Equipment (at cost): | |||

| Land (4) | 200,000 | ||

| Building | 1,750,000 | ||

| Machinery and equipment | 1,964,000 | ||

| Total | 3,714,000 | ||

| Less: Accumulated depreciation | (420,000) | 3,294,000 | |

| Total property, plant, and equipment | 3,494,000 | ||

| Intangible Asset: | |||

| Goodwill | 37,000 | ||

| Other Assets: | |||

| Cash restricted for building purposes [ Refer working note (1) ] | 100,000 | ||

| Officer’s note receivable [ Refer working note (2) ] | 30,000 | ||

| Land held for future building site [ Refer working note (4) ] | 250,000 | 380,000 | |

| Total Assets | 4,949,000 | ||

| Liabilities | |||

| Current Liabilities: | |||

| Accounts payable (5) | 119,800 | ||

| Current instalments of long-term debt[ Refer working notes (6) & (7) ] | 200,000 | ||

| Lawsuit liability | 80,000 | ||

| Income taxes payable (8) | 21,200 | ||

| Deferred tax liability | 5,000 | ||

| Total current liabilities | 426,000 | ||

| Long-Term Debt: | |||

| Mortgage payable (6) | 800,000 | ||

| Notes payable (7) | 400,000 | ||

| Deferred tax liability | 23,000 | ||

| Total long-term debt | 1,223,000 | ||

| Total Liabilities | 1,649,000 | ||

| Shareholders’ Equity: | |||

| Contributed Capital: | |||

| Common stock, authorized 100,000 shares of $50 par value; issued 40,000 shares; outstanding 39,800 shares (9) | 2,000,000 | ||

| Additional paid-in capital [ Refer working note (9) ] | 231,000 | ||

| Total paid-in capital | 2,231,000 | ||

| Retained earnings | 1,075,400 | ||

| Total | 3,306,400 | ||

| Less: Cost of treasury stock capital [ Refer working note (3) ] | (6,400) | ||

| Total Shareholders’ Equity | 3,300,000 | ||

| Total Liabilities and Shareholders’ Equity | 4,949,000 | ||

Table (1)

Therefore, the total of assets and total liabilities and shareholders’ equity equals to $4,949,000.

Working notes:

(1) Calculate corrected amount of cash balance:

| Cash, per unaudited balance sheet | $225,000 |

| Less: Unrecorded checks in payment of accounts payable | ($14,000) |

| NSF check not recorded | ($2,000) |

| Cash restricted for building purposes (reported in other assets) | ($100,000) |

| Corrected balance | 109,000 |

Table (2)

(2) Calculate the corrected amount of accounts receivable:

| Accounts receivable (net), per unaudited balance sheet | $345,700 |

| Add charge-back for NSF check [refer working note (1)] | $2,000 |

| Less: Officer’s note receivable (reported in other assets) | ($30,000) |

| Corrected balance | $317,700 |

Table (3)

(3) Calculate the corrected amount of investments:

| Investments, per unaudited balance sheet | $57,700 |

| Less: Long-term investment [reported separately as an asset] | ($51,300) |

| Treasury stock [reported in shareholders’ equity] | ($6,400) |

| Corrected balance | $0 |

Table (4)

(4) Calculate the corrected amount of land:

| Land, per unaudited balance sheet | $450,000 |

| Less: Land acquired for future building site (reported in other assets) | ($250,000) |

| Corrected balance | $200,000 |

Table (5)

(5) Calculate the corrected amount of accounts payable:

| Accounts payable, per unaudited balance sheet | $133,800 |

| Less: Unrecorded payments [refer working note (1)] | ($14,000) |

| Corrected balance | $119,800 |

Table (6)

(6) Calculate the corrected amount of mortgage payable:

| Mortgage payable, per unaudited balance sheet | $900,000 |

| Less: Current portion | (100,000) |

| Refinanced as long-term mortgage payable | $800,000 |

Table (7)

(7) Calculate the corrected amount of long-term note payable:

| Notes payable, per unaudited balance sheet | $500,000 |

| Less: Current portion | ($100,000) |

| Long-term note payable | $400,000 |

Table (8)

(8) Calculate the corrected amount of income taxes payable:

| Income taxes payable, per unaudited balance sheet | $61,200 |

| Less: Prepaid income taxes | ($40,000) |

| Corrected balance | $21,200 |

Table (9)

(9) Calculate the corrected amount of common stock:

| Common stock, per unaudited balance sheet | $2,231,000 |

| Less: Additional paid-in capital in excess of par value | ($231,000) |

| Corrected balance | $2,000,000 |

Table (10)

Want to see more full solutions like this?

Chapter 4 Solutions

Intermediate Accounting: Reporting And Analysis

- Firebird Corp. prepares monthly bank reconciliations of its checking account balance. The bank statement for February 2019 indicated the following: The correct amount of check #7853 is $797. It was recorded as a cash disbursement of $779 bymistake. The check was issued to pay for merchandise purchases. The check appeared on thebank statement correctly.Required:1. Prepare a bank reconciliation schedule at February 28, 2019, in proper form.2. What is the amount of cash that should be reported on the February 28, 2019 balance sheet?arrow_forwardOdum Corporation’s cash account showed a balance of $17,000 on March 31, 2019. The bank statement balance for the same date indicated a balance of $17,711.55. The following additional information is available concerning Odum’s cash balance on March 31: • Undeposited cash on hand on March 31 amounted to $724.50. • A customer’s NSF check for $175.80 was returned with the bank statement. • A note for $2,000 plus interest of $25 was collected for Odum by the bank during March. The bank notified Odum of this collection on the bank statement. • The bank service charge for March was $15. • A deposit of $960.75 mailed to the bank on March 31 did not appear on the bank statement. The following checks mailed to creditors had not been processed by the bank on March 31: Check # Amount 429 $57.40 432 147.50 433 210.80 434 191.90 A customer check for $149.50 in payment of his account and listed correctly for that amount on the bank statement had been incorrectly…arrow_forward1. In auditing the Maranao Company, you obtain directly from the bank, with which it does business, the bank statement, canceled checks, and other memoranda which relate to the company's bank account, for December 2021. In reconciling the bank balance at December 31, 2021 with that shown on the company's book, you observe the facts set forth below: Balance per bank statement, 12/31/21 Balance per book, 12/31/2021 Outstanding checks, 12/31/21 Receipts of 12/31/21 deposited 1/02/2022 Service Charge for Nov. 2021 per Bank Memo of 12/15/21 Proceeds of Bank Loan, 12/15/21, discounted for 3 months at 25% per annum, omitted from company's books Deposit of 12/23/21 omitted from Bank Statement Check of Tote's Products Co., charged back on 12/22/21 of absence of 88,219.12 58,983.46 32,108.42 4 5,317.20 3.85 9,875.00 7 2,892.41 counter-signature and redeposited with complete signature on 8 01/5/22,; no entry on the books having been made for the charge back or the redeposit 417.50 Error on Bank…arrow_forward

- The accounts of DMCI Holdings, Inc. revealed the following facts on August 31,2019. Balance of bank statement 1,200,000 Outstanding checks, August 31: Number 555 10,000 761 55,000 762 40,000 763 25,000 764 65,000 765 70,000 Receipts of August 31, deposited September 1 275,000 The bank statement showed the following charges: a. Service charge for August 5,000 b. NSF check received from a customer 85,000 The stub for check number 765 and the invoice relating thereto show that it was for P50,000. It was recorded incorrectly in the cash disbursements journal as P70,000. This check was drawn in payment of an account payable. Payment has been stopped on check number 555 which was drawn in payment of an account payable. The payee cannot be located. The cash balance per ledger on August 31, 2019 is ________.arrow_forwardJansen Company’s general ledger showed a checking account balance of $25,720 at the end of May 2021. The May 31 cash receipts of $2,530, included in the general ledger balance, were placed in the night depository at the bank on May 31 and were processed by the bank on June 1. The bank statement dated May 31, 2021, showed bank service charges of $57. All checks written by the company had been processed by the bank by May 31 and were listed on the bank statement except for checks totaling $2,080. Required: Prepare a bank reconciliation as of May 31, 2021. [Hint: You will need to compute the balance that would appear on the bank statement.]arrow_forwardUsing the following information, prepare a bank reconciliation for Young Co. for August 31, 2019, and prepare the journal entries: (a) The bank statement balance is $4,095 (b) The cash account balance is $4,205. (c) Outstanding checks amounted to $517. (d) Deposits in transit are $655. (e) The bank service charge is $45. (f) A check for $84 for supplies was recorded as $48 in the ledger. (g) NSF check for $649.00 (h) EFT collected $715.00 (i) Bank error processed a check for $53 as $35arrow_forward

- The cash account for Valley Bike Co. on October 1, 2019, indicated a balance of $5,140. During October, the total cash deposited was $39,175, and checks written totaled $40,520. The bank statement indicated a balance of $8,980 on October 31, 2019. Comparing the bank statement, the canceled checks, and the accompanying memos with the records revealed the following reconciling items: Checks outstanding totaled $5,560. A deposit of $1,050 representing receipts of October 31 had been made too late to appear on the bank statement. The bank had collected for Valley Bike Co. $2,120 on a note left for collection. The face of the note was $2,000. A check for $370 returned with the statement had been incorrectly charged by the bank as $730. A check for $310 returned with the statement had been recorded by Valley Bike Co. as $130. The check was for the payment of an obligation to Sports Pro Co. on account. Bank service charges for October amounted to $25. A check for $880 from Overwatch Condos…arrow_forwardThe bank statement for the checking account of Management Systems Inc. (MSI) showed a December 31, 2018, balance of $14,832.62. Information that might be useful in preparing a bank reconciliation is as follows: Outstanding checks were $1,340.55. The December 31, 2018, cash receipts of $585 were not deposited in the bank until January 2, 2019. One check written in payment of rent for $248 was correctly recorded by the bank but was recorded by MSI as a $284 disbursement. In accordance with prior authorization, the bank withdrew $470 directly from the checking account as payment on a mortgage note payable. The interest portion of that payment was $360. MSI has made no entry to record the automatic payment. Bank service charges of $16 were listed on the bank statement. A deposit of $885 was recorded by the bank on December 13, but it did not belong to MSI. The deposit should have been made to the checking account of MIS, Inc. The bank statement included a charge of $85 for an NSF check.…arrow_forwardWinson Company reported the following information related to its 31 August 2019 bank statement: i) The bank statement's balance is $3267. ii) The cash account balance is $3193. iii) The outstanding checks total $612. iv) The deposits in transit amount to $1415. v)The bank service charge is $27. vi) Winson's accountant issued a check for $153 (inpayment on an account payable) that was erroneously recorded in the ledger as $135. vii)Bank debit memorandum for$138 NSF (not sufficient funds)check from one of its customers. viii) The bank collected an account receivable in the amount of $1060 on. behalf if Winson Company. Required; Prepare Winson Company's bank reconciliation on 31 August 2019.arrow_forward

- In auditing Backstraight Boyz Corporation, you obtained the bank statement, cancelled checks, and other memoranda which relate to the company’s bank account for December 2021. In reconciling the bank balance with that shown on the company’s books, you observed the facts set forth below: Balance per bank statement, Dec. 31, 2021 P 47,174 Balance per books, Dec. 31, 2021 19,289 Outstanding checks, Dec. 31, 2021 63,000 Receipts of Dec. 31, 2021, deposited Jan. 2, 2022 6,260 Service charge for November, per bank 1,000memo of Dec. 15, 2021 Proceeds of bank loan, Dec. 15, 2021, discounted for 3 months at 18% per annum, omitted fromcompany books 47,750 Deposit of Dec. 22, 2021, omitted from bank statement…arrow_forwardIn reconciling a bank statement, when a check from the previous month appears on the bank statement (but not the cash balance due to timing), how would you state it on the reconciliation? The note that was given: The difference in the beginning balances in the company’s records and the bank statement relates to checks #469 and #470, which are outstanding as of April 30, 2021 (prior month). Attached is an image of my current progress.arrow_forwardIn connection with your audit of the Cash account of Bruhilda Co., you obtained the followinginformation. You are to prepare the following:1. A four-column reconciliation that would end at adjusted balances.2. Adjusting journal entries as of December 31, 2021.Reconciling items: November 30 December 31Deposits in transit P10,400 ?Outstanding checks 16,014 ?NSF checks 1,052 P1,400Customers’ notes collected by bank 3,000 8,554Bank service charges 100 130Erroneous bank debits 1,200 1,800Erroneous bank credits 2,000 6,000Book balances ? 332,472Bank balances 261,120 ?December transactions: Books BankReceipts P302,460 P299,902Disbursements 222,846 220,196arrow_forward

- Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Auditing: A Risk Based-Approach (MindTap Course L...AccountingISBN:9781337619455Author:Karla M Johnstone, Audrey A. Gramling, Larry E. RittenbergPublisher:Cengage Learning

Auditing: A Risk Based-Approach (MindTap Course L...AccountingISBN:9781337619455Author:Karla M Johnstone, Audrey A. Gramling, Larry E. RittenbergPublisher:Cengage Learning