Horngren's Financial & Managerial Accounting, The Financial Chapters (Book & Access Card)

5th Edition

ISBN: 9780134078939

Author: Tracie L. Miller-Nobles, Brenda L. Mattison, Ella Mae Matsumura

Publisher: PEARSON

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 6, Problem 6.31AP

Correcting inventory errors over a three-year period and computing inventory turnover and days’ sales in inventory

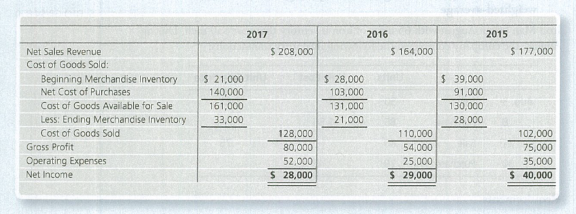

Lake Air Carpets’s books how the following data. In early 2018, auditors found that the ending merchandise inventory for 2015 was understated by $6,000 and that the ending merchandise inventory for 2017 was overstated by $7,000. The ending merchandise inventory at December 31, 2016, was correct.

Requirements

- 1. Prepare corrected income statements for the three years.

- 2. State whether each year’s net income—before your corrections—is understated or overstated, and indicate the amount of the understatement or overstatement.

- 3. Compute the inventory turnover and days’ sales in inventory using the corrected income statements for the three years. (Round all numbers to two decimals.)

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

Topic: SINGLE-ENTRY BOOKKEEPING

SANAOL Company suspects that there is missing inventory in its warehouse at December 31, 2021. All sales and purchases were made on account. Also, the gross profit rate based on net sales is consistent every year. To aid in your investigation, you obtained the following:

How much is the missing inventory during the year?

I What is the amount of gross profit for the eleven months

2 What is the amount of sales for the month of June?

a What is the cost of goods sold for the month of June ?

at an interim date, May 31, 2020, instead of at year end.

ended June 30, 2020, the CPA observed the physical inventory

The following information was obtained from the general

„Problem 13-14 (AICPA Adapted)

ended May 31, 2020?

year

In conducting an audit of Ultimate Company for the

a 1,680,000

b. 1,725,000

C. 1,735,000

d. 1,670,000

ledger.

Inventory, July 1, 2019

Physical inventory, May 31, 2020

Sales for 11 months ended May 31, 2020

Sales for year ended June 30, 2020

Purchases for 11 months ended May 31, 2020

before audit adjustments

Purchases for year ended June 30, 2020

before audit adjustments

875,000

950,000

8,400,000

9,600,000

в. 1,100,000

b. 1,200,000

c. 1,300,000

d. 1,400,000

er 14

6,750,000

8,000,000

1. Shipments received in May and included in the

physical inventory but recorded as June purchases

a. 960,000

b.…

For all exercises, assume the perpetual inventory system is used unless stated otherwise.

Correcting an inventory error—two years

Nature Foods Grocery.1 reported the following comparative income statements for the year ended June 30, 2019 and 2018:

During 2019, Nature Foods Grocery discovered that ending 2018 merchandise inventory was overstated by $5,500.

Requirements

Prepare corrected income statements for the two years.

State whether each year’s net income—before your corrections—is understated or overstated, and indicate the amount of the understatement or overstatement.

Chapter 6 Solutions

Horngren's Financial & Managerial Accounting, The Financial Chapters (Book & Access Card)

Ch. 6 - Which principle or concept states that businesses...Ch. 6 - Which inventory costing method assigns to ending...Ch. 6 - Assume Nile.com began April with 14 units of...Ch. 6 - Suppose Nile.com used the weighted-average...Ch. 6 - Which inventory costing method results in the...Ch. 6 - Prob. 6QCCh. 6 - At December 31, 2016, Stevenson Company overstated...Ch. 6 - Suppose Maestros had cost of goods sold during the...Ch. 6 - Suppose Nile.com used the LIFO inventory costing...Ch. 6 - Prob. 1RQ

Ch. 6 - Prob. 2RQCh. 6 - Prob. 3RQCh. 6 - What is the goal of conservatism?Ch. 6 - Prob. 5RQCh. 6 - Under a perpetual inventory system, what are the...Ch. 6 - Prob. 7RQCh. 6 - Prob. 8RQCh. 6 - What does the lower-of-cost-or-market (LCM) rule...Ch. 6 - What account is debited when recording the...Ch. 6 - What is the effect on cost of goods sold, gross...Ch. 6 - When does an inventory error cancel out, and why?Ch. 6 - Prob. 13RQCh. 6 - Prob. 14RQCh. 6 - Prob. 15ARQCh. 6 - Prob. 16ARQCh. 6 - Determining inventory accounting principles Ward...Ch. 6 - Determining inventory costing methods Ward Hard...Ch. 6 - Use the following information to answer Short...Ch. 6 - Use the following information to answer Short...Ch. 6 - Use the following information to answer Short...Ch. 6 - Use the following information to answer Short...Ch. 6 - Comparing Cost of Goods Sold under FIFO, UFO, and...Ch. 6 - Applying the lower-of-cost-or-market rule Assume...Ch. 6 - Determining the effect of an inventory error...Ch. 6 - Computing the rate of inventory turnover and days...Ch. 6 - Use the following information to answer Short...Ch. 6 - Prob. 6.12SECh. 6 - Prob. 6.13SECh. 6 - Using accounting vocabulary Match the accounting...Ch. 6 - Comparing inventory methods Zippy, a regional...Ch. 6 - Prob. 6.16ECh. 6 - Use the following information to answer Exercises...Ch. 6 - Use the following information to answer Exercises...Ch. 6 - Comparing amounts for cost of goods sold, ending...Ch. 6 - Comparing cost of goods sold and gross...Ch. 6 - Prob. 6.21ECh. 6 - Prob. 6.22ECh. 6 - Prob. 6.23ECh. 6 - Prob. 6.24ECh. 6 - Prob. 6.25ECh. 6 - Prob. 6.26ECh. 6 - Prob. 6.27ECh. 6 - Accounting for inventory using the perpetual...Ch. 6 - Accounting for inventory using the perpetual...Ch. 6 - Prob. 6.30APCh. 6 - Correcting inventory errors over a three-year...Ch. 6 - Accounting for inventory using the periodic...Ch. 6 - Accounting for inventory using the perpetual...Ch. 6 - Prob. 6.34BPCh. 6 - Prob. 6.35BPCh. 6 - Prob. 6.36BPCh. 6 - Prob. 6.37BPCh. 6 - Prob. 6.38CPCh. 6 - Accounting for inventory using the perpetual...Ch. 6 - Suppose you manage Campbell Appliance. The stores...Ch. 6 - Ever since he was a kid, Carl Montague wanted to...Ch. 6 - The notes are an important part of a companys...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Effects of an Inventory Error The income statements for Graul Corporation for the 3 years ending in 2019 appear below. During 2019, Graul discovered that the 2017 ending inventory had been misstated due to the following two transactions being recorded incorrectly. a. A purchase return of inventory costing $42,000 was recorded twice. b. A credit purchase of inventory' made on December 20 for $28,500 was not recorded. The goods were shipped F.O.B. shipping point and were shipped on December 22, 2017. Required: 1. Was ending inventory for 2017 overstated or understated? By how much? 2. Prepare correct income statements for all 3 years. 3. CONCEPTUAL CONNECTION Did the error in 2017 affect cumulative net income for the 3-year period? Explain your response. 4. CONCEPTUAL CONNECTION Why was the 2019 net income unaffected?arrow_forwardErrors As controller of Lerner Company, which uses a periodic inventory system, you discover the following errors in the current year: 1. Merchandise with a cost of 17,500 was properly included in the final inventory, but the purchase was not recorded until the following year. 2. Merchandise purchases are in transit under terms of FOB shipping point. They have been excluded from the inventory, but the purchase was recorded in the current year on the receipt of the invoice of 4,300. 3. Goods out on consignment have been excluded from inventory. 4. Merchandise purchases under terms FOB shipping point have been omitted from the purchases account and the ending inventory. The purchases were recorded in the following year. 5. Goods held on consignment from Talbert Supply Co. were included in the inventory. Required: For each error, indicate the effect on the ending inventory and the net income for the current year and on the net income for the following year.arrow_forwardFinancial statement data for years ending December 31 for Holland Company follow: a. Determine the inventory turnover for 20Y4 and 20Y3. b. Determine the days sales in inventory for 20Y4 and 20Y3. Use 365 days and round to one decimal place. c. Does the change in inventory turnover and the days sales in inventory from 20Y3 to 20Y4 indicate a favorable or an unfavorable trend?arrow_forward

- If a group of inventory items costing $3,200 had been double counted during the year-end inventory count, what impact would the error have on the following inventory calculations? Indicate the effect (and amount) as either (a) none, (b) understated $______, or (c) overstated $______. Table 10.2arrow_forwardInventory Analysis The following account balances are taken from the records of Lewis Inc., a wholesaler of fresh fruits and vegetables: Required Compute Lewiss inventory turnover ratio for 2016 and 2015. Compute the number of days sales in inventory for 2016 and 2015. Assume 360 days in a year. Comment on your answers in parts (1) and (2) relative to the companys management of inventory over the two years. What problems do you see in its inventory management?arrow_forwardInventory Valuation You are engaged in an audit of Roche Mfg. Company for the year ended December 31, 2019. To reduce the workload at year-end, Roche took its annual physical inventory under your observation on November 30, 2019. Roches inventory account, which includes raw materials and work in process, is on a perpetual basis, and it uses the first-in, first-out method of pricing. It has no finished goods inventory. The companys physical inventory revealed that the book inventory of 60,570 was understated by 3,000. To avoid distorting the interim financial statements, Roche decided not to adjust the book inventory until year-end except for obsolete inventory items. Your audit revealed this information about the November 30 inventory: Pricing tests showed that the physical inventory was overpriced by 2,200. Footing and extension errors resulted in a 150 understatement of the physical inventory. Direct labor included in the physical inventory amounted to 10,000. Overhead was included at the rate of 200% of direct labor. You determined that the amount of direct labor was correct and the overhead rate was proper. The physical inventory included obsolete materials recorded at 250. During December, these materials were removed from the inventory account by a charge to cost of sales. Your audit also disclosed the following information about the December 31, 2019, inventory. Total debits to certain accounts during December are: The cost of sales of 68,600 included direct labor of 13,800. Normal scrap loss on established product lines is negligible. However, a special order started and completed during December had excessive scrap loss of 800 which was charged to Manufacturing Overhead Expense. Required: 1. Compute the correct amount of the physical inventory at November 30, 2019. 2. Without prejudice to your solution to Requirement 1, assume that the correct amount of the inventory at November 30, 2019, was 57,700. Compute the amount of the inventory at December 31,2019.arrow_forward

- Under the periodic inventory system, what account is debited when an estimate is made for sales made this year, but expected to be returned next year? (a) Sales Returns and Allowances (b) Merchandise Inventory (c) Customer Refunds Payable (d) Salesarrow_forwardAnalyzing Inventory The recent financial statements of McLelland Clothing Inc. include the following data: Required: 1. Calculate McLellands gross profit ratio (rounded to two decimal places), inventory turnover ratio (rounded to three decimal places), and the average days to sell inventory (assume a 365-day year and round to two decimal places) using the FIFO inventory costing method. Be sure to explain what each ratio means. 2. Calculate McLellands gross profit ratio (rounded to two decimal places), inventory turnover ratio (rounded to three decimal places), and the average days to sell inventory (assume a 365-day year and round to two decimal places) using the LIFO inventory costing method. Be sure to explain what each ratio means. 3. CONCEPTUAL CONNECTION Which ratios-the ones computed using FIFO or LIFO inventory values-provide the better indicator of how successful McLelland was at managing and controlling its inventory?arrow_forwardUnder the periodic inventory system, what account is credited when an estimate is made for sales made this year, but expected to be returned next year? (a) Merchandise Inventory (b) Customer Refunds Payable (c) Sales (d) Sales Returns and Allowancesarrow_forward

- Scenario 1:Rocky Inc hired a new intern from CSU to help with year-end inventory. The intern computed the inventory counts at the end of 2020 and 2021. However, the intern's manager, a UNC grad, noticed that the ending inventory did not include inventory on consignment to a retail customer of $3,000 at the end of year 2020 and $6,000 at the end of year 2021. What was the effect of the error (if any] on 2021's statements (amount and whether it was under- ( too low) or over-stated (too high)? If there is no effect, put OKarrow_forwardTopic: SINGLE-ENTRY BOOKKEEPING HALSEY Company suspects that there is missing inventory in its warehouse at December 31, 2021. All sales and purchases were made on account. Also, the gross profit rate based on net sales is consistent every year. To aid in your investigation, you obtained the following: How much is the net sales revenue for the year?arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

Financial Accounting: The Impact on Decision Make...

Accounting

ISBN:9781305654174

Author:Gary A. Porter, Curtis L. Norton

Publisher:Cengage Learning

Cornerstones of Financial Accounting

Accounting

ISBN:9781337690881

Author:Jay Rich, Jeff Jones

Publisher:Cengage Learning

Financial Accounting

Accounting

ISBN:9781305088436

Author:Carl Warren, Jim Reeve, Jonathan Duchac

Publisher:Cengage Learning

Financial Accounting

Accounting

ISBN:9781337272124

Author:Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:Cengage Learning

College Accounting, Chapters 1-27

Accounting

ISBN:9781337794756

Author:HEINTZ, James A.

Publisher:Cengage Learning,

Accounting Changes and Error Analysis: Intermediate Accounting Chapter 22; Author: Finally Learn;https://www.youtube.com/watch?v=c2uQdN53MV4;License: Standard Youtube License