Concept explainers

Videos

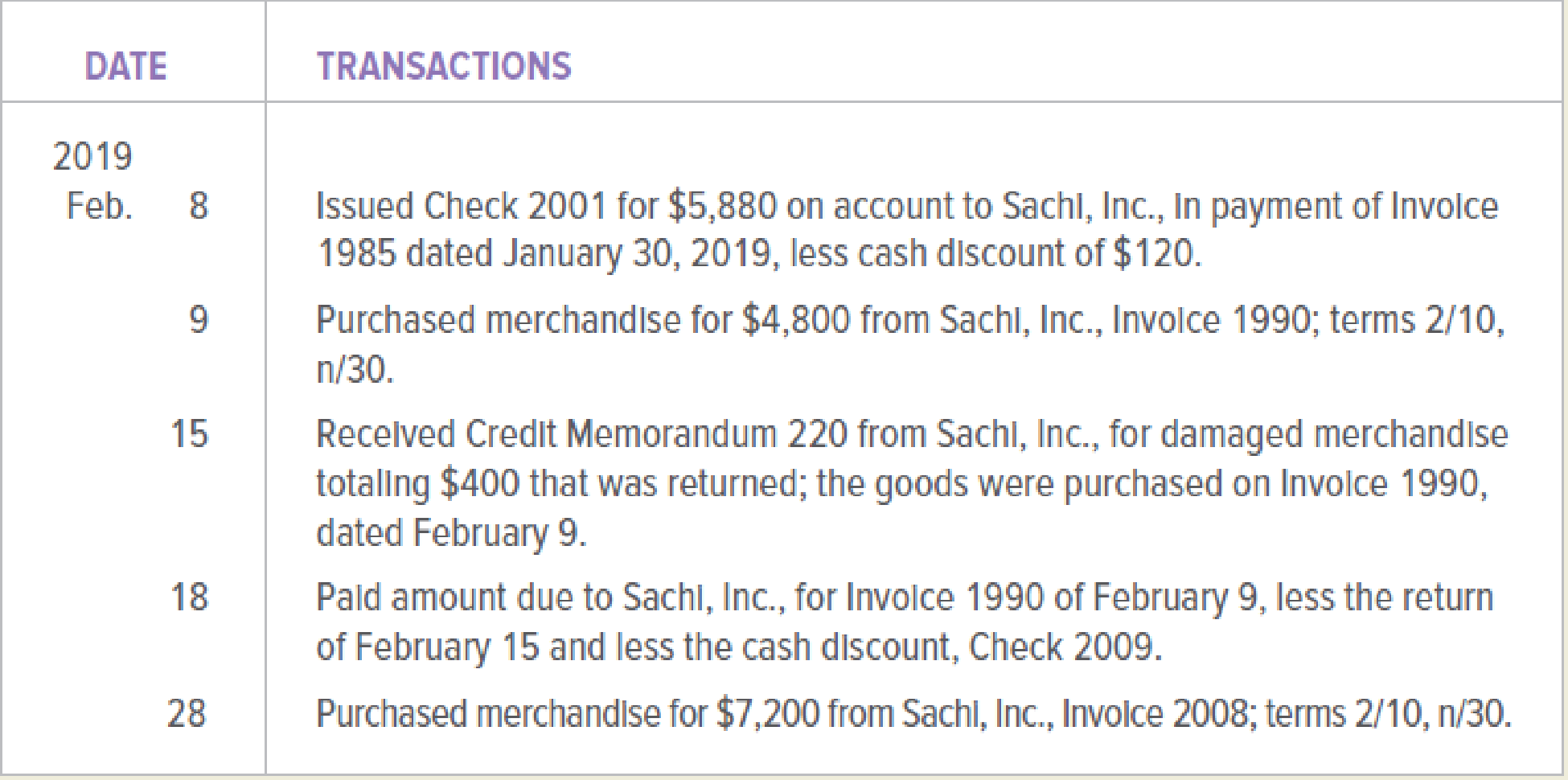

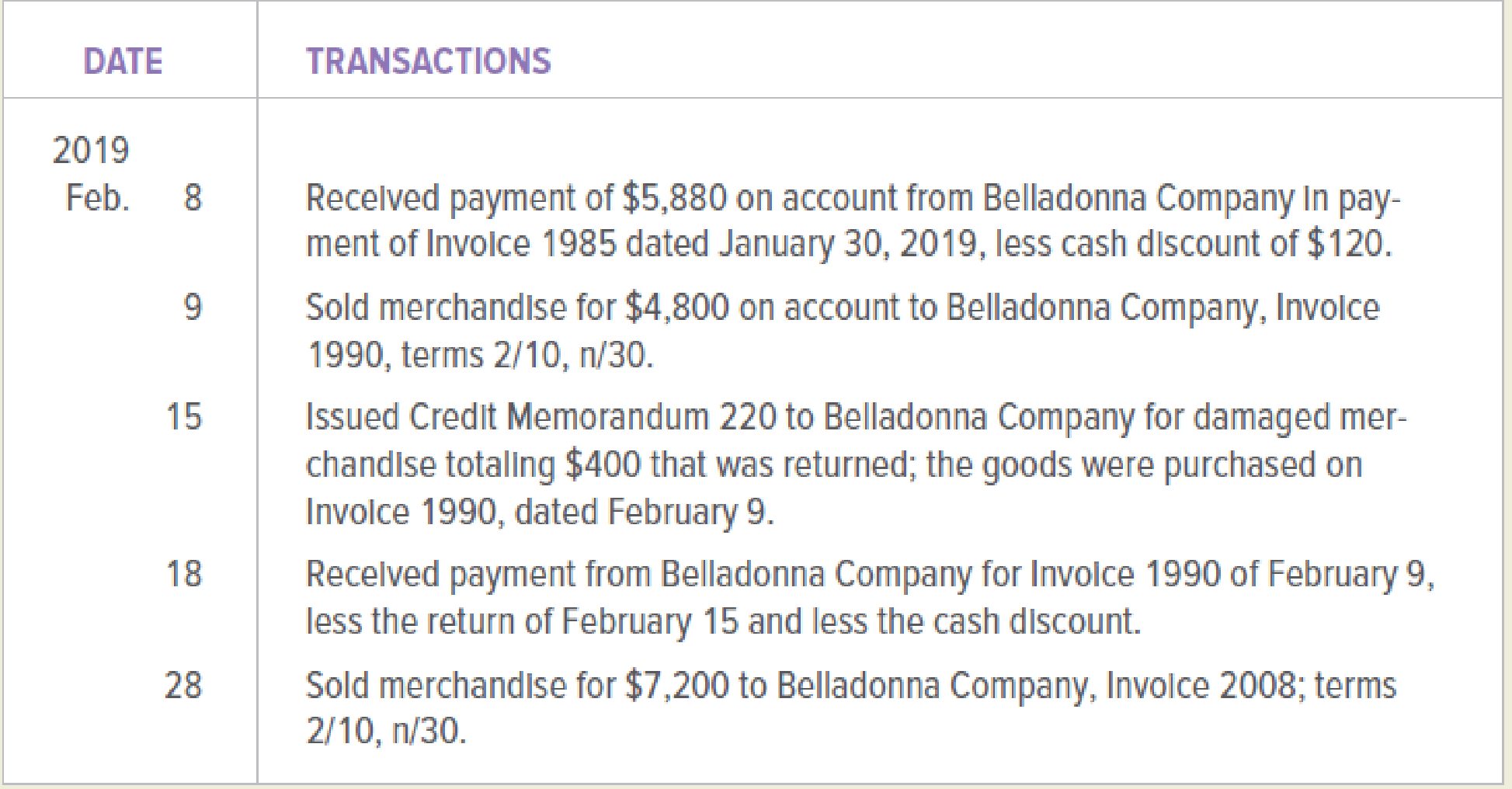

Belladonna Company (buyer) and Sachi, Inc. (seller), engaged in the following transactions during February 2019:

Belladonna Company

Sachi, Inc.

INSTRUCTIONS

- 1. Open the accounts payable ledger account and accounts receivable ledger account indicated below for both Belladonna Company and Sachi, Inc. Enter the balances as of February 1, 2019.

- 2. Journalize the transactions above in a general journal for both Belladonna Company and Sachi, Inc. Begin the journals for both companies with page 12.

- 3.

Post the transactions to the appropriate accounts in the general ledger and the accounts payable subsidiary ledger for Belladonna Company. - 4. Post the transactions to the appropriate accounts in the general ledger and the accounts receivable subsidiary ledger for Sachi, Inc.

GENERAL LEDGER ACCOUNTS—BELLADONNA COMPANY

201 Accounts Payable, $6,000 Cr.

ACCOUNTS PAYABLE LEDGER ACCOUNT—BELLADONNA COMPANY

Sachi, Inc., $6,000

GENERAL LEDGER ACCOUNTS—SACHI, INC.

111 Accounts Receivable, $6,000 Dr.

ACCOUNTS RECEIVABLE LEDGER ACCOUNT—SACHI, INC.

Belladonna Company, $6,000

Analyze: What is the balance of the accounts payable for Sachi, Inc., in the Belladonna Company accounts payable subsidiary ledger? What is the balance of the accounts receivable for Belladonna Company in the Sachi, Inc., accounts receivable subsidiary ledger?

1.

Create the accounts payable ledger account and accounts receivable ledger account of company B and company SI indicating the balances on given date.

Explanation of Solution

Ledgers:

Ledgers are T accounts to which journal entries are posted. Ledgers are used to ascertain transactions of a particular account and its closing balance for the period. The day-to-day transactions of the business are recorded in their respective ledgers.

The accounts payable ledger account of company B is as follows:

| Accounts Payable | ||||

| Date | Particular |

Debit ($) |

Credit ($) |

Balance ($) |

| February 1,2019 | Balance | 6,000 | ||

Table (1)

The accounts receivable ledger account of company SI is as follows:

| Accounts Receivable | ||||

| Date | Particular |

Debit ($) |

Credit ($) |

Balance ($) |

| February 1,2019 | Balance | 6,000 | ||

Table (2)

2.

Record the entries into the general journal of the company B and the company SI.

Explanation of Solution

The recording of entries in the general journal for company B is as follows:

Recording the payment made:

| GENERAL JOURNAL | Page 12 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| February 8, 2019 | Accounts payable/Company SI | 6,000 | ||

| Purchases discounts | 120 | |||

| Cash | 5,880 | |||

| (to record the payment made and receiving purchases discount) | ||||

Table (3)

- • The accounts payable account is liability and the account balance is decreasing. Therefore, accounts payable account is debited.

- • The purchases discount account is a contra expense account. The account has the normal credit balance and it is increasing. Therefore, it is credited.

- • The cash account is an asset account and the account balance is decreasing. Therefore, it is credited.

Recording the purchases on credit:

| GENERAL JOURNAL | Page 12 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| February 9, 2019 | Purchases | 4,800 | ||

| Accounts payable/Company SI | 4,800 | |||

| (to record the inventory purchased on account with terms2/10, n/30) | ||||

Table (4)

- • The purchases account is an expense account. The purchases account has normal debit balance and the balance is increasing. Therefore, it is debited.

- • Accounts payable is liability and the balance of accounts payable is increasing. Therefore, it is credited.

Recording the purchases returned and credit memorandum received:

| GENERAL JOURNAL | Page 12 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| February 15, 2019 | Accounts payable/Company SI | 400 | ||

| Purchases returns and allowances | 400 | |||

| (to record the inventory returned and credit memorandum received) | ||||

Table (5)

- • The accounts payable account is a liability account. The accounts payable account has the normal credit balance and it is decreasing. Therefore, it is debited.

- • The purchase returns and allowances account is contra expenses account. The account has the normal credit balance and it is increasing. Therefore, it is credited.

Recording the payment made:

| GENERAL JOURNAL | Page 12 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| February 18, 2019 | Accounts payable/Company SI | 4,400 | ||

| Purchases discounts | 88 | |||

| Cash | 4,312 | |||

| (to record the payment made and receiving purchases discount) | ||||

Table (6)

- • The accounts payable is liability and the account balance is decreasing. Therefore, accounts payable account is debited.

- • The purchases discount account is a contra expense account. The account has the normal credit balance and it is increasing. Therefore, it is credited.

- • The cash account is an asset account and the account balance is decreasing. Therefore, it is credited.

Recording the purchases on credit:

| GENERAL JOURNAL | Page 12 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| February 28, 2019 | Purchases | 7,200 | ||

| Accounts payable/Company SI | 7,200 | |||

| (to record the inventory purchased on account with terms2/10, n/30) | ||||

Table (7)

- • The purchases account is an expense account. The purchases account has normal debit balance and the balance is increasing. Therefore, it is debited.

- • Since, the accounts payable is liability and the account balance is increasing. Therefore, it is credited.

The recording of entries in the general journal for company SI is as follows:

Recording the payment received from the buyer:

| GENERAL JOURNAL | Page 12 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| February 8, 2019 | Sales Discount | 120 | ||

| Cash | 5,880 | |||

| Accounts Receivable/Company B | 6,000 | |||

| (to record the payment received and discount provided) | ||||

Table (8)

- • The sales discount account is identified as contra revenue account and it has normal debit balance which is increasing. Therefore, it is debited.

- • The cash account is debited. This is because the cash account is asset account and the account balance is increasing. The amount in cash account would be calculated by subtracting the merchandise returned by the buyer and the sales discount provided.

- • The accounts receivable account is an asset account and the account balance is decreasing. Therefore, it is credited.

Recording of the merchandise sold:

| GENERAL JOURNAL | Page 12 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| February 9, 2019 | Accounts Receivable/ Company B | 4,800 | ||

| Sales | 4,800 | |||

| (to record the merchandise sold on credit on terms of 2/10, n/30) | ||||

Table (9)

- • The accounts receivable is debited. This is because the accounts receivables account is an asset account and the account balance is increasing.

- • The sales account is credited. This because the sales account is identified as the revenue account and the revenue is generated.

Recording the returned merchandise sold and the credit memorandum:

| GENERAL JOURNAL | Page 12 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| February 15, 2019 | Sales returns and allowances | 400 | ||

| Accounts Receivable/ Company B | 400 | |||

| (to record the merchandise returned and issued credit memorandum) | ||||

Table (10)

- • The sales returns and allowances account is identified as contra revenue account with normal debit balance and it is increasing. Therefore, it is debited.

- • The account receivable account is an asset account and the account balance is decreasing. Therefore, the accounts receivable account is credited.

Recording the payment received from the buyer:

| GENERAL JOURNAL | Page 12 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| February 18, 2019 | Sales Discount | 88 | ||

| Cash | 4,312 | |||

| Accounts Receivable/Company B | 4,400 | |||

| (to record the timely payment received from the account receivable) | ||||

Table (11)

- • The sales discount account is identified as contra revenue account and it has normal debit balance which is increasing. Therefore, it is debited.

- • The cash account is debited. This is because the cash account is asset account and the account balance is increasing. The amount in cash account would be calculated by subtracting the merchandise returned by the buyer and the sales discount provided.

- • The accounts receivable account is asset account and the account balance is decreasing. Therefore, it is credited.

Recording of the merchandise sold and sales tax payable:

| GENERAL JOURNAL | Page 12 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| February 28, 2019 | Accounts Receivable/ Company B | 7,200 | ||

| Sales | 7,200 | |||

| (to record the merchandise sold on credit on terms of 2/10, n/30) | ||||

Table (12)

- • The accounts receivables account is debited. This is because the accounts receivables account is an asset account and the account balance is increasing.

- • The sales account is credited. This because the sales account is identified as the revenue account and the revenue is generated.

Working Note:

Calculation of purchases discount:

The purchases discounts are received by the buyer for fulfilling the terms of timely payment to seller for purchases. The terms related to paying on timely basis with the company SI was agreed as 2/10, n/30. The terms 2/10, n/30 means the buyer is entitled to receive two percent of purchase discount on the purchases amount. The buyer will be entitled to the discount only if the payment is paid within ten days after provided invoice.

The amount calculated as purchase discount would be $88.

Calculation for sales discount:

The sales discount is provided to the customer by the seller fulfilling the terms of making the timely payments as per 2/10, n/30 terms. The customer is entitled to receive the one percent of sales discount on the merchandise sold if the payment is made with ten days of invoice provided.

The amount calculated as per given information would be $88.

3.

Record the transactions to the appropriate accounts in the general ledger and the accounts payable subsidiary ledger for company B.

Explanation of Solution

The posting of general journal in the appropriate accounts in the general ledger and the accounts payable subsidiary ledger is as follows:

| Cash | ||||

| Date | Particular |

Debit ($) |

Credit ($) |

Balance ($) |

| Feburary 1,2019 | Balance | - | ||

| February 8, 2019 | 5,880 | (5,880) | ||

| February 18, 2019 | 4,312 | (10,192) | ||

Table (13)

| Accounts Payable/Company SI | ||||

| Date | Particular |

Debit ($) |

Credit ($) |

Balance ($) |

| Feburary 1,2019 | Balance | 6,000 | ||

| February 8, 2019 | 6,000 | - | ||

| February 9, 2019 | 4,800 | 4,800 | ||

| February 15, 2019 | 400 | 4,400 | ||

| February 18, 2019 | 4,400 | - | ||

| February 28, 2019 | 7,200 | 7,200 | ||

Table (14)

| Accounts Payable | ||||

| Date | Particular |

Debit ($) |

Credit ($) |

Balance ($) |

| Feburary 1,2019 | Balance | 6,000 | ||

| February 8, 2019 | 6,000 | - | ||

| February 9, 2019 | 4,800 | 4,800 | ||

| February 15, 2019 | 400 | 4,400 | ||

| February 18, 2019 | 4,400 | - | ||

| February 28, 2019 | 7,200 | 7,200 | ||

Table (15)

| Purchases | ||||

| Date | Particular |

Debit ($) |

Credit ($) |

Balance ($) |

| Feburary 1,2019 | Balance | - | ||

| February 9, 2019 | 4,800 | 4,800 | ||

| February 28, 2019 | 7,200 | 12,000 | ||

Table (16)

| Purchases Returns and Allowances | ||||

| Date | Particular |

Debit ($) |

Credit ($) |

Balance ($) |

| Feburary 1,2019 | Balance | - | ||

| February 15, 2019 | 400 | 400 | ||

Table (17)

| Purchases Discounts | ||||

| Date | Particular |

Debit ($) |

Credit ($) |

Balance ($) |

| Feburary 1,2019 | Balance | - | ||

| February 8, 2019 | 120 | 120 | ||

| February 18, 2019 | 88 | 208 | ||

Table (18)

4.

Record the transactions to the appropriate accounts in the general ledger and the accounts payable subsidiary ledger for company SI.

Explanation of Solution

| Cash | ||||

| Date | Particular |

Debit ($) |

Credit ($) |

Balance ($) |

| Feburary 1,2019 | Balance | - | ||

| February 8, 2019 | 5,880 | 5,880 | ||

| February 18, 2019 | 4,312 | 10,192 | ||

Table (19)

| Accounts Receivable/Company B | ||||

| Date | Particular |

Debit ($) |

Credit ($) |

Balance ($) |

| Feburary 1,2019 | Balance | 6,000 | ||

| February 8, 2019 | 6,000 | - | ||

| February 9, 2019 | 4,800 | 4,800 | ||

| February 15, 2019 | 400 | 4,400 | ||

| February 18, 2019 | 4,400 | - | ||

| February 28, 2019 | 7,200 | 7,200 | ||

Table (20)

| Accounts Receivable | ||||

| Date | Particular |

Debit ($) |

Credit ($) |

Balance ($) |

| Feburary 1,2019 | Balance | 6,000 | ||

| February 8, 2019 | 6,000 | - | ||

| February 9, 2019 | 4,800 | 4,800 | ||

| February 15, 2019 | 400 | 4,400 | ||

| February 18, 2019 | 4,400 | - | ||

| February 28, 2019 | 7,200 | 7,200 | ||

Table (21)

| Sales | ||||

| Date | Particular |

Debit ($) |

Credit ($) |

Balance ($) |

| Feburary 1,2019 | Balance | - | ||

| February 9, 2019 | 4,800 | 4,800 | ||

| February 28, 2019 | 7,200 | 12,000 | ||

Table (22)

| Sales Returns and Allowances | ||||

| Date | Particular |

Debit ($) |

Credit ($) |

Balance ($) |

| Feburary 1,2019 | Balance | - | ||

| February 15, 2019 | 400 | 400 | ||

Table (23)

| Sales Discounts | ||||

| Date | Particular |

Debit ($) |

Credit ($) |

Balance ($) |

| Feburary 1,2019 | Balance | - | ||

| February 8, 2019 | 120 | 120 | ||

| February 18, 2019 | 88 | 208 | ||

Table (24)

The balance of accounts payable account for company SI in company B’s subsidiary ledger is $7,200 credit balance. The balance of accounts receivable account for company B in company SL’s subsidiary ledger is $7,200 debit balance.

Want to see more full solutions like this?

Chapter 8 Solutions

COLLEGE ACCOUNTING (LL)W/ACCESS>CUSTOM<

- Refer to RE6-8. On April 23, 2020, McKinncy Co. receives a check, from Mangold Corporation for 8,500. Prepare the journal entry for McKinncy to record the collection of the account previously written off.arrow_forwardAnalyzing Accounts Receivable Upham Companys June 30, 2019, balance sheet included the following information: Required: 1. Prepare the journal entries necessary for Upham to record the preceding transactions. 2. Prepare an analysis and schedule that shows the amounts of the accounts receivable, allowance for doubtful accounts, notes receivable, and notes receivable dishonored accounts that will be disclosed on Uphams June 30, 2020, balance sheet.arrow_forwardConsider the following note payable transactions of Cargo Video Productions. i (Click the icon to view the transactions.) Requirements 1. Journalize the transactions for the company. 2. Considering the given transactions only, what are Cargo Video Productions' total liabilities on December 31, 2025? Requirement 1. Journalize the transactions for the company. (Record debits first, then credits. Select explanations on the last line of the journal entry.) Sep. 1, 2024: Purchased equipment costing $270,000 by issuing a nine-year, 7% note payable. The note requires annual principal payments of $30,000 plus interest each September 1. Date Accounts and Explanation Debit Credit 2024 Sep. 1 Equipment 270,000 Notes Payable 270,000 Purchased equipment by issuing a 9-year, 7% note. Dec 31, 2024: Accrued interest on the note payable. Date Accounts and Explanation Debit Credit 2024 Dec. 31 Interest Expense 6,300 Interest Payable 6,300 Recognized accrued interest. Sep. 1, 2025: Paid the first…arrow_forward

- Read through the information below for selected transactions during the month of December, 2021 and prepare the required jounal entry to record the transaction. Post each of the entries below to the general ledger T-accounts attached . Sold Merchandise for $5,000 to Lee Corp on account on December 9. Cost of the merchandise was $3,390 and the terms of the sale were 1/15, n/30.arrow_forwardREQUIRED Prepare journal entries for the purchase transaction held on December 1, 2020. Prepare the forward contract transaction entered into on December 1, 2020. Prepare the journal entries to track the accounts payable and the forward contract on December 31, 2020, for Chrysler Exporters Inc. financial statements.arrow_forwardThe following is an alphabetical list of Lloyd’s Hudson Dealership Inc.’s December 31, 2019, balance sheet accounts and amounts: 1. Prepare a properly classified balance sheet for Lloyd’s Hudson Dealership as of December 31, 2019. List the additional parenthetical or note disclosures (if any) that should be made for each item. 2. Next Level Compute the current ratio. what does it indicate about Lloyd’s Hudson Dealership?arrow_forward

- Song, Inc. (seller), engaged in the following transactions during January 2019: Song, Inc. DATE TRANSACTIONS 2019 Jan. 8 Received payment of $2,058 on account from Bowden Company in payment of Invoice 1885 dated December 30, 2018, less cash discount of $42. 10 Sold merchandise for $1,550 on account to Bowden Company, Invoice 1920, terms 2/10, n/30. 15 Issued Credit Memorandum 320 to Bowden Company for damaged merchandise totaling $200 that was returned; the goods were purchased on Invoice 1920, dated January 10. 19 Received payment from Bowden Company for Invoice 1920 of January 10, less the return of January 15 and less the cash discount. 30 Sold merchandise for $3,300 to Bowden Company, Invoice 1950; terms 2/10, n/30. Required: Journalize the transactions above in a general journal for Song, Inc. No Date General Journal Debit Credit 1 Jan 08, 2019 2 Jan 10, 2019…arrow_forwardOn December 5, 2019, Super Circuit Store sold gift certificates totalling $12,000. By December 31, 2019, all but $2,125 worth of these certificates had been redeemed for merchandise. Outstanding certificates were then redeemed by January 15, 2020. Required: 1. Prepare journal entries on Super Circuit’s books to reflect the preceding transactions. 2. How would the gift certificates be reported on Super Circuit’s balance sheet on December 31, 2019?arrow_forwardRosalie Couses the gross method to record sales made on credit. On June 10, 2019, it made sales of £100,000 with terms 2/10, n/30 to Finley Farms, Inc. On June 19, 2019, Rosalie received payment for 1/2 the amount due from Finley Farms. Rosalie’s fiscal year end is on June 30, 2019. What amount will be reported in the statement of financial position for the accounts receivable due from Finley Farms, Inc.?arrow_forward

- Rasheed Company uses net method to record the sales made on credit. On June 30, 2019, it made a sales of OMR 25,000 with term 3/15, n/45. Prepare the required journal entries, if: (a) On July 7 Rasheed company received full payment. (b) On July 22 Rasheed company received full payment.arrow_forwardThe following selected accounts and their current balances appear in the ledger of Kanpur Co. for the fiscal year ended June 30, 2019: 1. Prepare a multiple-step income statement.2. Prepare a statement of owner’s equity.3. Prepare a balance sheet, assuming that the current portion of the note payable is$7,000.4. Briefly explain how multiple-step and single-step income statements differ.arrow_forwardOn June 7,2019, Dilby Mechanical Corp completed $50,00 of servicing work for a client and billed them for that amount plus a GST of $2,500 and PST of $3,50; terms are N20. Required: a. Prepare the journal entry as it would appear in Dilby's accounting records. b. Assume the receivable established on June 7 was collected on June 27. Record the entry.arrow_forward

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning